Risk measures versus risk Models

For advisors, the lesson here is not that they should throw away the standard ways of summarizing risk using measures such as standard deviation and downside deviation.10 Nor should advisors ru

n to embrace Fama's log-stable models.

Instead, we think advisors should understand the limitations of standard risk measures and have a basic understanding of what Mandelbrot's and Fama's work says about describing risk. Rather than solely relying on a few summary statistics to characterize the risks of an investment, advisors would benefit by beginning to think about a more complete risk model. A complete risk model allows investors to consider three questions about a potential decline in value simultaneously:

- How likely might a decline occur?

- How long might it last?

- How bad might it get?

As you can appreciate through our study of historical stock market declines, time horizon is a key dimension of risk not explicitly addressed by standard risk measures. A complete risk model can be used to explicitly take time horizons into account.

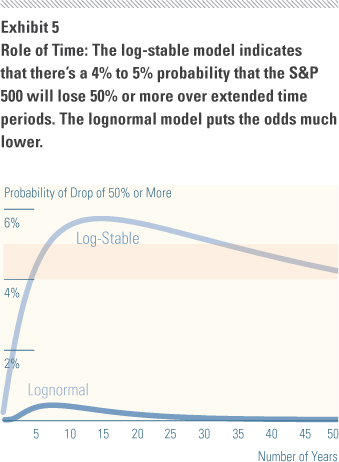

For example, in Exhibit 5, we plot the probability of a cumulative loss of 50% or more over various time horizons using the lognormal distribution for the S&P 500 that we show in Exhibit 2 and the log-stable distribution in Exhibit 3. The lognormal model shows that the risk of such a severe decline over an extended period is negligible. The log-stable model, on the other hand, indicates that such a loss over an extended period has a probability of 4% to 5%--numbers significant enough to gain the attention of risk-averse advisors and investors who might want to be prepared for such a scenario.

Conclusion

In every financial crisis, investors relearn the same message--there isn't a magic risk measure or model that can account for or predict every significant drop in the market. Economists and quantitative analysts have made incredible strides over the decades engineering new ways to explain the distribution of returns. These developments provide investors with valuable information to help them decide how to allocate their portfolios for any number of investing scenarios and mitigate risk. But they are not perfect.

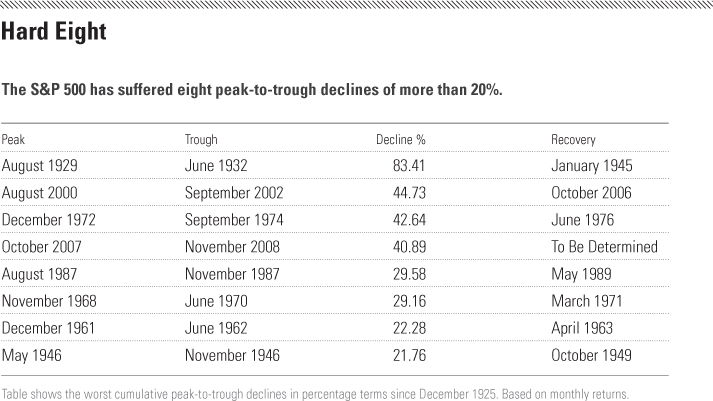

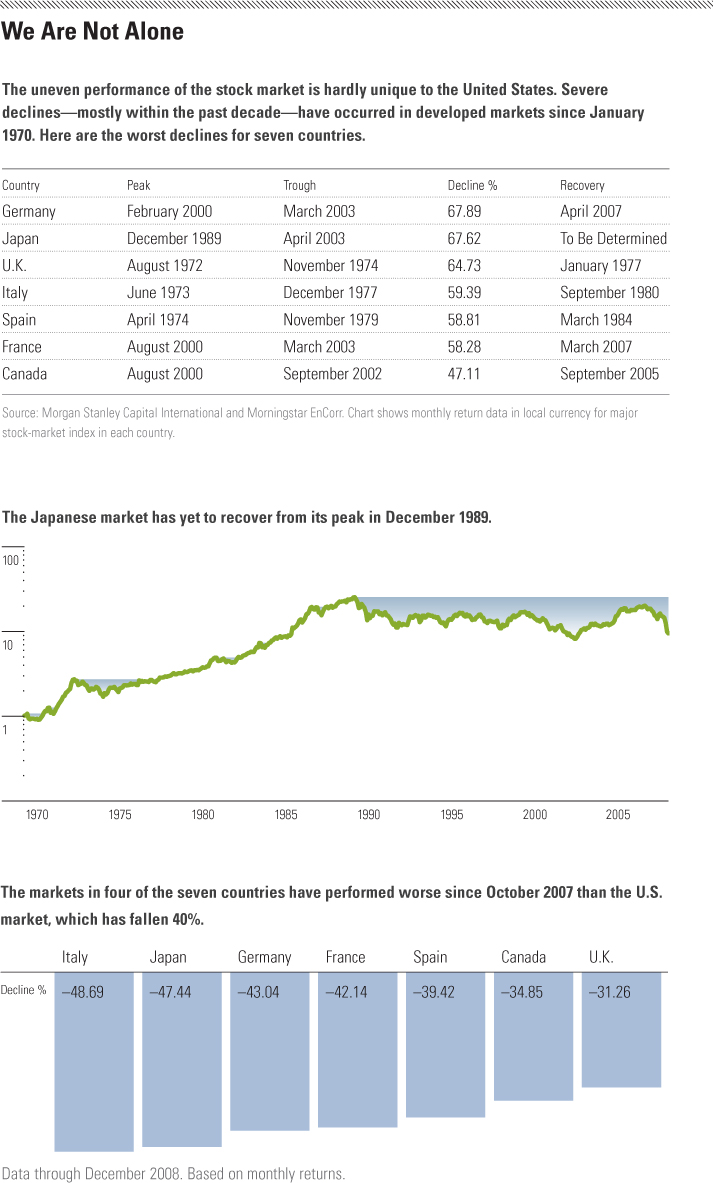

As we've shown, the record contains a much bumpier ride than many risk models would suggest. In addition to preparing clients' portfolios for these occasional severe declines and taking other precautions, advisors would do well to keep reminding their clients of the risks they face as investors. Clients should be fully prepared to take on the 100-year floods they will surely face in the future.

Footnotes:

10. In recognition that return distributions may not be symmetric, measures such as skewness and kurtosis are sometimes presented alongside standard deviation. However, like variance, these measures are not defined for stable Paretian distributions.

This article first appeared in the February/March 2009 issue of Morningstar Advisor Magazine.

{kind=link}

{kind=link}

{kind=link}