.jpg)

The short answer is yes, because the driving force behind the rally in December has not changed. Investors still believe rate cuts are coming in 2024 and are awaiting the positive effect this will have on the economy.

We believe both European and US markets are slightly overvalued, but this shouldn't get in the way of further market gains if momentum is sufficiently strong. There are of course risks, particularly in Europe, should the underlying economy weaken further or if interest rate cuts don't arrive as expected. While we see numerous opportunities across sectors, we believe some of the more defensively orientated ones, such as consumer defensives or healthcare, offer an attractive hedge in this scenario.

Europe's Weak Data

Underlying the market rally in late 2023 was the belief that central banks will cut rates in early 2024. So the first question to ask ourselves is whether this situation has changed-- and it hasn't. If anything, recent data points have added weight behind the argument to cut rates.

In Europe, purchasing managers' index readings are weak, particularly in manufacturing. So is GDP, which actually turned negative toward the end of 2023. The employment market, although tight by historic standards, is still loose enough that central bankers shouldn’t fear the effects of rising rates. Similarly, inflation has fallen close enough to the coveted 2% level for them to be less concerned about pressures returning as a result of interest rate cuts.

In the US, the economy is certainly running warmer, but the labour market has loosened sufficiently, and clamour of pulling off a soft landing may be enough to nudge central bankers towards at least some rate cuts.

Investors Keep the Faith

Despite negative economic readings for much of 2023, markets maintained their historically high levels, with both European and US indexes hitting or at least coming close to all-time highs during the year. The reason for this is hope for a brighter 2024 with lower interest rates, allowing investors to look look past weak economic conditions.

Now that we’ve finally entered 2024 and are closer than ever to those much vaunted rate cuts, it’s very difficult to see investors losing faith.

Can Markets Keep Rallying?

When markets are trading at a discount to our fair value estimates, it's very easy to point to a level and say “that’s where markets could go”. But now, with both US and European markets trading above their fair value estimates, it’s impossible to quantify where they could go. Famous investor Howard Marks explained markets' behaviour well when he described them as a pendulum that swings between being overvalued and undervalued, spending very little time in between.

We ultimately believe that markets eventually revert to their fair value estimates, but we acknowledge that knowing a fair value estimate does not help with market timing. We do not see the current market as an opportunity to simply “back up the truck”, but we also know that momentum is a powerful force that could lift markets well beyond their fair value estimates for some time.

With the overwhelmingly positive catalyst of interest rate cuts awaiting us in 2024, pointing out potential pitfalls is no easy task. In the US, the relatively strong economy and labour markets could work against the central rate cut scenario. The Fed remains concerned about a recurrence of high inflation rates and an overheating economy. Any signs of this in 2024 could spook the Fed into holding or even raising interest rates, which would put pressure on equity markets.

Meanwhile in Europe, the risks are pointing in the opposite direction as its economy teeters on the brink of recession, such that any interest rate cuts may come too late to stop an economic crash. Although investors are for the most part looking past the latest negative economic readings, this could change if the readings deteriorate enough.

Where Are the Undervalued Sectors?

Given that markets are trading slightly above their fair values and risks remain to investors’ optimistic outlooks, how should people invest in 2024?

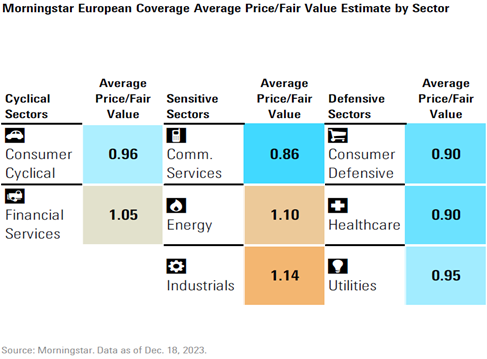

Despite markets as a whole being fairly valued, there is huge disparity across sectors. In Europe, industrials and energy are overvalued by more than 10%. In the US, technology and industrials are the two overvalued sectors, trading at a 5-9% premium based on our bottom-up estimates. This contrasts heavily with valuations for sectors such as consumer defensive and healthcare in Europe, and real estate or basic materials in the US.

Although some attractive areas we mentioned are highly cyclically exposed, others, such as utilities and healthcare, have some solid defensive qualities that investors would do well to remember should the path to a soft landing not be as smooth as hoped.

.jpg)