.jpg)

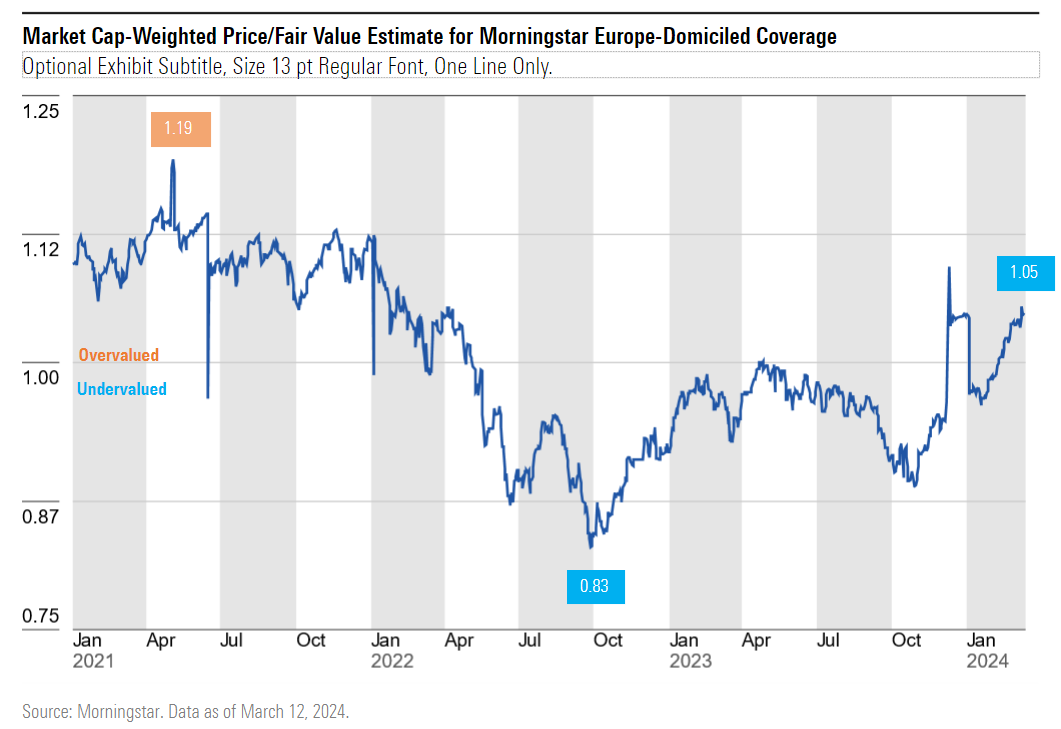

After a strong run in the first quarter of the year, European equities have stopped looking cheap. The market as a whole is now slightly overvalued, trading at 1.05 times our intrinsic fair value estimate. On a relative basis though, Europe still trades at a slight discount to North American stocks. Additionally, valuations are disparate across the sectors, creating opportunities for investors.

There are three specific sectors in which we believe investors are potentially missing out on emerging themes:

• The easing of inflationary pressure on consumer-facing firms

• The growth of order backlogs for key industrial firms

• An undervalued utilities sector offering an increasingly attractive income stream

Who Benefits From Falling Inflation?

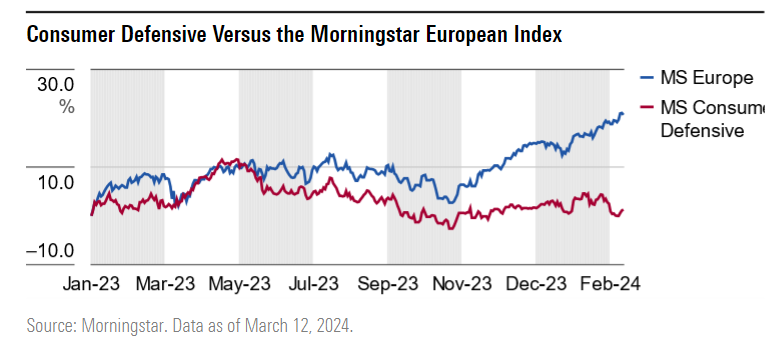

The consumer defensive sector has materially underperformed the broader European market over the last twelve months. Much of this underperformance has stemmed from lethargy on behalf of the consumer.

We’ve been touting the virtues of wide-moat consumer defensive names throughout. Most notably their pricing power – the ability to pass through inflationary increases to the end consumer, thus protecting their operating margins. But, after such a sustained period of high inflation, many consumers are simply stretched to their limits.

This has been evidenced by a lack of volume growth for many consumer defensive firms. For example, consumer giant Nestle (NESN) delivered 7.2% revenue growth in the year 2023, an impressive feat given that global GDP growth was just 3% over the same period. Volume growth over this period was -0.3%, with pricing increases making up the 7.5% shortfall. That's a good illustration of the firm’s ability to pass through price increases, but also an indicator that consumers are pulling back on what they buy in response to increased prices. Recent UK retail sales numbers showed that consumers are buying less goods now that they did before the pandemic.

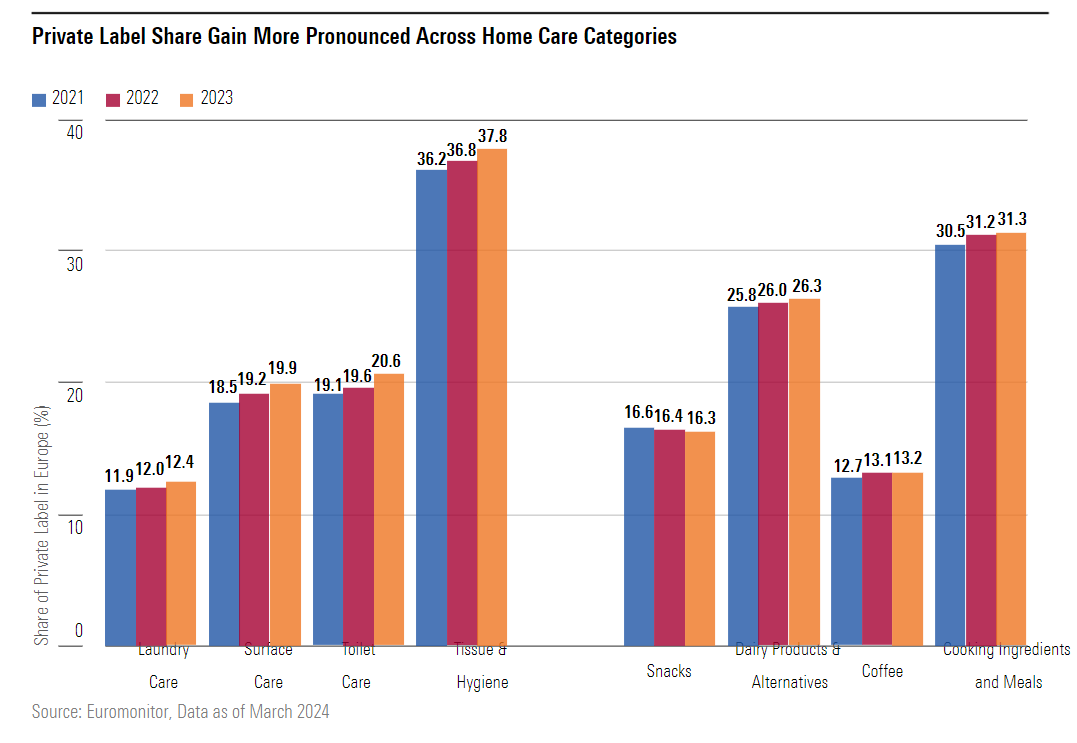

Another symptom of this has been the shift to cheaper alternatives, “downtrading” in industry parlance. Recent Euromonitor data has shown a pick-up in private label goods across numerous categories of consumer goods, particularly those where pricing power is not as strong.

Thankfully, inflation is finally easing. In the Eurozone, consumer price increases have slowed to just 2.4%, from 10.6% at their peak in 2022, while in the US it has fallen to 3.2%, from a 9.1% peak. As these declines slowly filter through supply chains, consumer defensive firms will feel the benefit, with potential for improved volume growth over the coming months.

Some of these gains may have to be reinvested in the brands themselves to ensure that they remain relevant. Still, with the consumer defensive sector trading as much as 15% below our fair value estimate, this could be a catalyst for the gap to narrow.

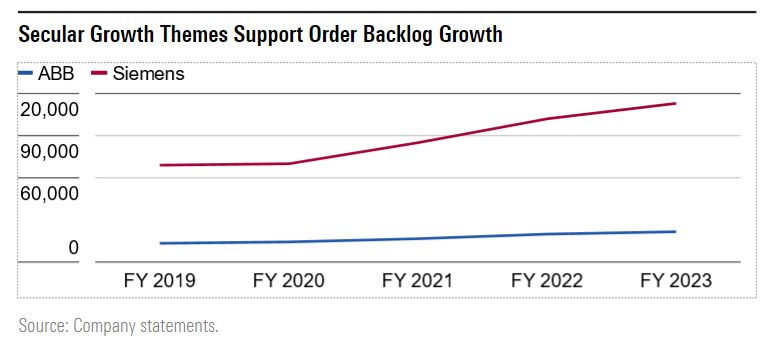

Industrial Order Backlogs are Finally Growing Again

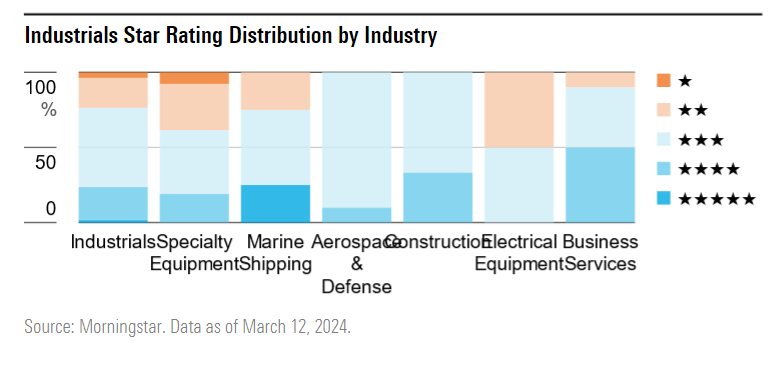

The last couple of years have not been an easy time for European industrial firms, many of whom have literally been at the coalface, dealing with elevated energy prices, low economic growth and weak demand. Looking at valuations, you would not guess this. Industrials are one of the few sectors actually trading at a premium to our intrinsic fair value estimate.

Of course Industrials are far from a homogenous space: They encompasses everything from shipping firms and construction materials providers to pest control businesses. Valuations across these sub-sectors are disparate, with half of the business services space currently undervalued.

One structural theme we have seen emerge has been growing order books for many large industrial names. Stocks like Siemens [SIE], ABB [ABBN] and Schneider Electric [SU] have all reported growing order backlogs. Among firms benefiting from growing order books, the common denominator is exposure to one of the following three themes, and in the case of the three aforementioned companies, a Wide Moat rating.

• Rising investment into energy efficiency in buildings

• Data center investment propelled by AI needs

• The energy transition requiring low- and medium-voltage electrical equipment

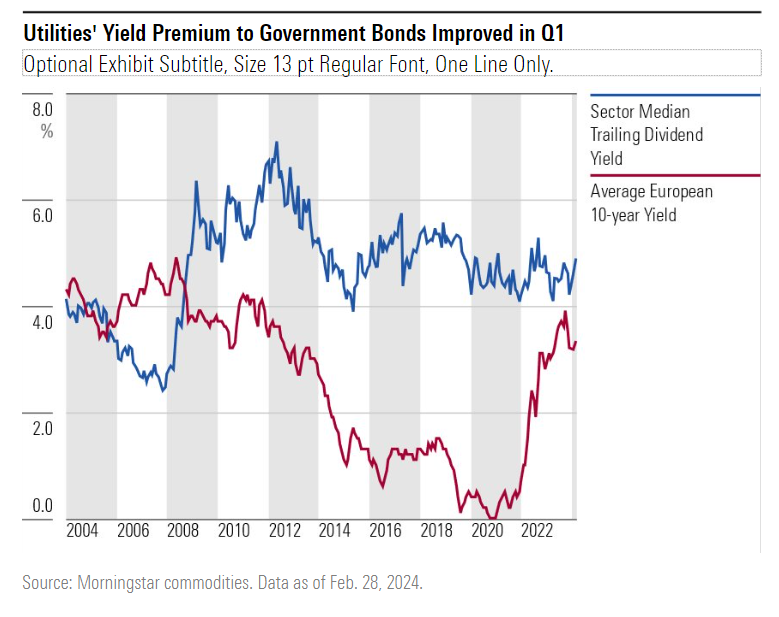

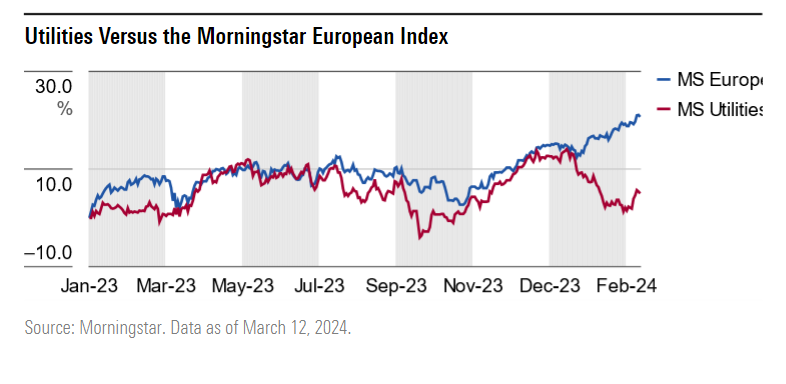

What Do Falling Rates Mean For Income Stocks?

European utilities shares have underperformed the general market for about twelve months, and their underperformance became very acute in the first quarter of 2024. Falling gas prices have hit power producers, while high interest rates have weighed on the whole sector through elevated debt servicing costs. Utility firms, particularly the regulated ones, tend to hold more debt that the average company.

The sector as a whole now trades at an unusually large 20% discount to our fair value estimate. One potential catalyst we see to this valuation gap closing is falling interest rates. For much of the last decade, the utilities sector offered a very attractive dividend yield relative to government bonds. This trend reversed in 2022 as central banks hiked rates, making bonds a real alternative source of income for investors as the yield gap almost closed entirely last year.

Since then however, bond yields have begun to fall. A recent Reuters poll showed that 90% of economists expect the first interest rate cut from the ECB in June of this year, and Morningstar's economists expect the same from the Federal Reserve. Historically, bond yields have fallen as central banks prepare to cut rates. In this dynamic, utility stocks’ attractiveness to income investors should continue to rise, potentially boosting share prices.