One of the most effective ways to help people save for retirement is automatic enrolment. This “nudge” works from the understanding that people may experience obstacles (such as the impetus to open a pension) that stop them from saving. Auto-enrolment was introduced in the UK in 2012 as has proved a huge success at overcoming this.

But is auto-enrolment ethical? Morningstar senior behavioural scientist Stan Treger has looked at people’s perceptions of behavioural interventions – so-called “nudges”.

His research of US savers found that overall people felt auto-enrolment was less ethical, but more effective at helping people to save for retirement than workplace pension schemes which require the individual to actively opt-in to saving. Savers liked employer-matching of pension contributions and having a range of investment options, but preferred the idea of opting in rather than opting-out, which is what you need to do to get out of an auto-enrolment scheme.

The UK is heading for a “retirement crisis”. Longer life expectancies and low savings rates mean many individuals are facing the prospect of not having enough cash to get them through retirement. The phasing out of "defined benefit" or final salary pension schemes, which guaranteed an income for life, have been a major catalyst. Today, defined contribution pensions are the most common – and with this type of pension, the amount you have to retire on depends on the movements on the stock market and how you invested your money. In short, the onus is on the individual – and the individual, it was decided, needed a nudge in the right direction.

Research by Sunstein et al (2019), who coined the term “nudge” has considered public support for nudges generally. Morningstar’s Treger looks at them specifically in relation to retirement saving, surveying 1,390 people across the US, with a median age of 41. (It’s worth pointing out that this study is US focused, and auto-enrolment is not mandated in the US, although it is becoming more widely used).

Three Tasks

Participants were given three tasks:

- Rank 16 features that a workplace pension scheme might have in order from most to least important.

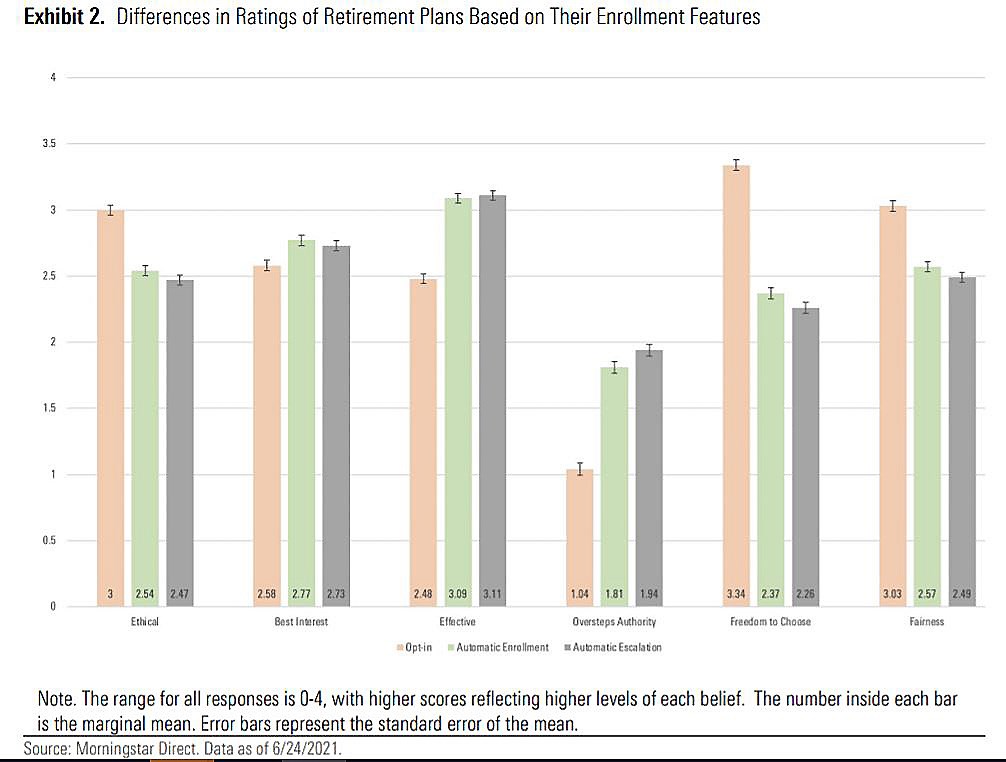

- Reach descriptions of different types of pension schemes (opt-in, automatic enrolment, automatic escalation of contributions) and rate: how ethical it is; how fair it is; whether it gives people freedom to choose how to use their money; how effective it is at helping people prepare for retirement; whether it serves the employee's best interest; and whether it oversteps the authority of the company.

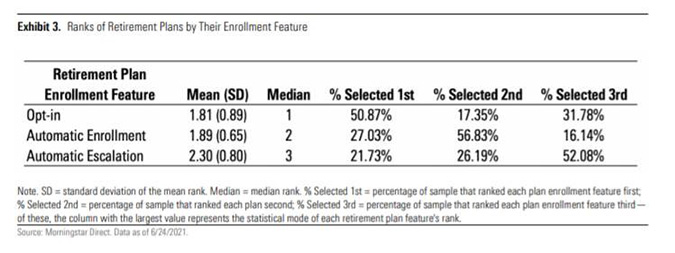

- Rank three types of pension plan from most to least preferred

In the first task, employer matching was the most popular feature, with 41% of participants selecting it. Interestingly, access to investing in cryptocurrency was next most popular, selected by 24% of those surveyed. Other top choices included the number of available investment options, the reputation of the pension provider, and automatic escalation.

The results of the second task are summarised in the below chart. Here we can see that auto-enrolment and auto-escalation schemes were viewed as less ethical and less fair, but as more effective than opt-in schemes.

The final task revealed that opt-in pension schemes were still the first choice of the majority, selected by 50.87% of participants. Auto-enrolment was the most popular second choice, at 56.83%.

What can we learn from this data? Treger summarises: “This experiment showed that people largely believe that automatic-enrolment features are less ethical yet more effective at helping people save for retirement than opt-in features.”

3 Key Takeaways

1. There are some perceived ethical trade-offs

Despite savers acknowledging their effectiveness, there is still hesitancy around these schemes, says Treger. “The biggest effect documented in this research was for the freedom to choose how to use one’s own money: participants believed that both types of automatic-retirement features offer substantially less freedom over using one’s money than opt-in features,” he adds. “In fact, the results suggest that people may weigh the ethical foundation of a pension plan over its effectiveness when making their decisions.”

2. But people don’t view auto-enrolment negatively

The average scores for the ethical evaluations and effectiveness for auto-enrolment and auto-escalation pensions were still above the middle of the scale, says Treger. “So while people may generally prefer opt-in plans they do not seem to be averse to being automatically enrolled in a retirement account.”

3. Other features are far more important

“Free money” in the form of an employer matching pension contributions was by far the biggest priority for those surveyed, says Treger. Other features that participants ranked as more important than both automatic-enrolment and automatic-escalation included the reputation of the company managing the accounts and the number of investment choices.