In the current crisis, people are looking to reduce their outgoings as much as possible, taking mortgage and credit card holidays to ease the pressure on their household finances. Suspending some payments might make sense in the short term, but should you also consider having a pension holiday?

Faced with March’s historic sell-off, many people are nervous about stock market volatility and the risk of loss; those approaching retirement may have had their plans thwarted or delayed by a drop in their pension funds. In lockdown, people are understandably focused on their health rather than long-term financial plans.

But the decision to cut back on retirement saving is one that shouldn’t be taken lightly, experts argue, because of the many factors involved in pension contributions, from tax relief to company matching schemes. There is evidence that even a short pause in contributions could have a damaging long-term effect on the size of your retirement fund.

Research by Royal London suggests that even a modest time out of the market will reduce the size of your pension pot at 65 and that effect is magnified the further you are from retirement age.

For example a 30-year-old paying an average amount of around £200 a month (including employer contributions) into their pension would knock nearly £15,000 off their final pension pot if they stopped contributions a year; and would reduce their pot by around £7,000 with a six-month pension holiday. The margin is reduced as you move up the age scale, but it is still significant: a 12-month break for someone 15 years from retirement shaves £7,000 off the final figure.

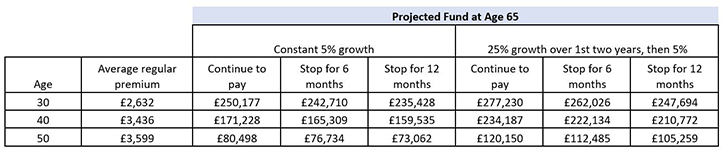

The below table shows what a pension pot would be worth for savers of various ages and contribution levels under different pension holiday scenarios.

While the first batch figures assume that markets rise at a conservative 5% a year over the period. But given the nature of the recent sell-off, history suggests that equity markets could bounce back strongly – so Royal London has modelled a 25% bounce in stock markets in the next two years. The effect of missing this rebound is even more pronounced for a 30-year old missing a year’s payments – they would be around £30,000 worse off at retirement in this scenario, equivalent to a whopping 12% of their pension pot.

Time to Top Up Instead?

Kay Ingram, director of public policy at financial planning group LEBC, says that in some cases, people can afford to top their pensions but are just put off by the recent stock market volatility. Those who are still working but saving on gym and commuting costs, for example, have more disposable income than before the crisis. Even workers who took a pay cut may find themselves in a lower tax bracket and are now eligible for child benefit and an increased savings allowance (although the tax relief is lower).

Older workers at pensionable age, meanwhile, will have just received an inflation-busting 3.9% increase in the State Pension; money could be used to top up a private pension. You can even use increased pension contributions to take yourself out of the higher rate tax bracket.

Under auto-enrolment, companies must match the employee's 5% contribution with a 3% top up - and under the UK Government's Coronavirus Retention Scheme, continuing this payment is a condition of receiving state help to pay wages.

But some companies that currently go over and above this 3% matching figure may now be looking at reducing these this year to cut costs. What should an employee do in this case? Ingram argues that for an employee to cut or suspend their payments in response will compound the problem.

Take Advice

Household finances have been affected in different ways by the Covid-19 crisis so it's important to seek independent financial advice to discuss your options, especially if you have been furloughed or lost your job. The Pensions Regulator says employers must still keep up the minimum contributions required under auto-enrolment even in the crisis and “savers need support to make good decisions in these challenging circumstances”.

For an employee, you could talk to your employer about reducing contributions during this period rather than stopping altogether; it's worth noting that to stop payments you need to leave the pension scheme and re-enrol at a later date of your choosing.

The UK Government’s Money and Pension Service suggests looking at alternatives first: "Suspending your pension contributions may seem like a good idea but it’s worth considering other ways of reducing expenditure if possible."

If you must suspend your contributions, its guidance is to keep the break brief and rejoin as soon as you can: “If you do decide to pause your contributions, this will impact the income that you will have in retirement and you should try to make this pause as short as is possible.”

Still, some company schemes may make you wait a year to rejoin - and that's a year that may have a long-term impact on your retirement prospects.