Asian equities are enjoying an uptick in popularity as we approach the end of the road for the global pandemic. Combine the reopening of both the economy and the borders with a booming tech sector and pent-up consumer demand, and fund managers believe that opportunities abound in the region.

We have spoken to Asia fund managers about the key trends to consider, and what their favourite stocks are:

Key Asia Themes

Tech stocks in countries such as China, Taiwan and South Korea in particular have surged over the past year and while Covid-19 has been a boost, it is not the only driving force for success. The region’s middle class has been growing steadily, meaning more disposable income, which is enabling companies focused on e-commerce, online entertainment, cloud, software and semiconductors to thrive.

And with greater disposable income comes a focus of quality: quality of life through better healthcare, and growing interest in quality products. China, for example, is enjoying rapid growth across its healthcare industry. And according to Charlie Dutton, portfolio manager at the Bronze-rated Ninety One Asia Pacific Franchise, the country has made significant investment in research and development (R&D) - even outspending America, meaning higher-quality products sold at a higher margin.

Moreover, the focus on clean energy is showing no plans to slow down, and China’s plan to achieve carbon neutrality means big growth potential for green companies across solar, wind, and electric vehicles.

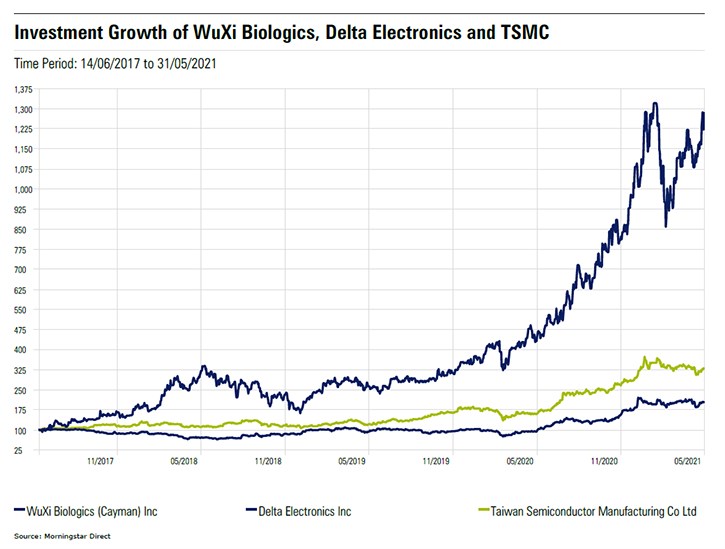

So which stocks are likely to benefit from these market developments? According to the fund managers we spoke to, three stocks stand out: WuXi Biologics (02269), Delta Electronics (2308), and Taiwan Semiconductor Manufacturing Co (2330).

WuXi Biologics

Biologics contract development and manufacturing organisation (CDMO) WuXi Biologics is at an interesting stage, rapidly building its services to help other biologics companies research and develop drugs at a cheaper and faster rate. Currently, it holds a 79% market share in China, but is also the third-largest CDMO company globally with a 5% market share.

Ayaz Ebrahim, manager of the JPMorgan Asia Growth and Income Trust (JAGI) thinks this is an interesting stock due to China’s rapidly expanding healthcare industry. “WuXi Biologics is a leader in the contract manufacturing field and a good example of a company offering integrated technology platforms for biologics drug developments. Over the past year it has experienced a rise in demand for drug manufacturing outsourcing.”

The company is currently trading at a 51% premium, according to Morningstar's fair value estimate - not surprising given that its shares climbed 210% last year. The stock has a Morningstar rating of two stars, but remains an investor favourite.

Delta Electronics

Against the backdrop of an increasingly electrified world, Taiwanese electronics manufacturing company Delta Electronics is well positioned to benefit from several long-term thematic trends such as electric vehicles, automation, 5G and big data, according to Alastair Reynolds, portfolio manager at Martin Currie.

“Delta Electronics is the largest power-supply vendor globally and is making the transition from supplying PC and smartphone makers to meeting the new-economy demand for electric vehicles, datacentres, and industrial robots," he says. "Delta has a strong track record of utilising its core power efficiency skill set in other applications, and often these new applications come with higher margins and high barriers to entry.”

The company has a narrow moat and is trading at a 23% premium with a two-star rating. Shares were up 76% last year but this isn't a short-term success story - shares have delivered annualised returns of 12.31% over 10 years.

TSMC

Taiwan Semiconductor Manufacturing Co (TSMC) has been a popular stock due to the semiconductor shortage during the Covid-19 pandemic, and Morningstar believes it to be undervalued (trading at a 20% discount) because of a successful strategy, a wide moat and continuous technical advancements where its competition has struggled. As the world’s largest dedicated contract chip manufacturer, or foundry, its services are sought-after by companies making mobile phones, cars, computers and automated business solutions. Half its revenue stems from the smartphone market.

According to Laure Négiar, manager of the Comgest Growth World Fund, TSMC was a strong double-digit grower before covid too, but even with growing demand and pressures, the companies did not try to profit excessively or raise prices. “Their aim is to keep the trust of clients for the long term and to keep the ecosystem working well. And as long-term investors we're really happy to see their position.”

JPMorgan’s Ebrahim adds: “We continue to believe industry leaders such as (…) TSMC are well-placed to continue to deliver strong results despite ongoing market uncertainties.” Shares have delivered annualised returns of 23.92% over the past decade.