Global stock markets had a minor sell-off in early May but then maintained their upward direction, despite concerns over inflation as the world economic recovery cranks up. Value stocks still have the upper hand over growth so far this year, which is reflected in the performance of the UK stock market.

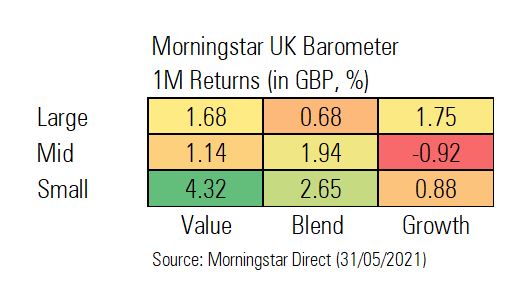

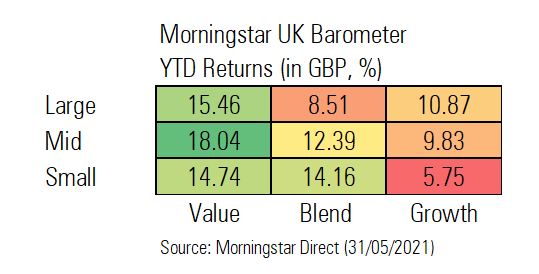

It was another positive month for the large value stocks in the Morningstar UK Index such as Lloyds Banking Group (LLOY), but large growth stocks like retailer Next (NXT) also put in a respectable showing. Both styles were up just under 2% in May. But it was small-cap value stocks that led the charge in May with a 4.32% rise, helped by outsized gains from the likes of infrastructure group John Laing (JLG). While mid-cap value shares had a less impressive month, in the year to date these stocks are ahead of all other styles and sizes with a return of 18%, compared with 15% for large-cap value and 14% for small-cap value.

UK Barometer One Month Returns by Style and Size

Why did small-cap UK value stocks outperform so strongly in May? The nature of the UK recovery, which is currently favouring small-and-medium sized companies, is a key factor. But there are other stock-specific issues at work. John Laing shares were the best performers in the 22-strong list of small caps, gaining 30% in May after the UK Governement announced plans for “Great British Railways”. John Laing, which works on public infrastructure projects like rail, roads and schools, is expected to be a beneficiary of the plans for a state-owned public body taking charge of railways from 2023 onwards. Other outsized gains in the group include Bank of Georgia (BGEO), which gained 28% as it swung back into profit in the first quarter of 2021. But the performance of the small caps wasn’t all positive, with a number of companies like Currys PC World owner Dixons Carphone (DC.) posting negative returns in share price terms in May.

The small-cap blend category, whose shares combine elements of growth and value stocks, was the second best performing in the month with a gain of 2.65%. The 47 companies in this group saw a wide variation in performance, from -18% for Magners cider maker C&C Group (CCR) to a gain of 26% for property development company St Modwen Properties (SMP), which has attracted the interest of private equity giant Blackstone. The US company made an offer for St Modwen in May for £1.2 billion, or 542p per share, drawn by its portfolio of warehouse and distribution properties.

Mid-cap blend was the next best performing category of stocks with a rise of 1.94%. This category has the most amount of stocks within the Morningstar UK index, as it contains 67 companies, with the next biggest being mid-cap growth with 50 names. Mid-cap blend hosts a number of household names such as supermarket Sainsbury’s (SBRY), pasty chain Greggs (GRG) and housebuilder Taylor Wimpey (TW.), which are up 17%, 39% and 5% so far this year. The best performer in this category in May was UDG Healthcare (UDG) with a gain of 23% and miner Ferrexpo (FXPO) is the biggest riser in 2021 so far, soaring 77% as iron ore prices have hit new highs.

UUK Barometer Year to Date Returns by Size and Style

Last year saw extreme volatility in stock markets and outperformance of growth as a style – so it's worth looking again at our Barometer for 2020 showed that small-cap value stocks fell 22% while small-cap growth companies gained nearly 40%, a difference of around 62 percentage points. At this stage of 2021, mid cap value is the best performing style with an increase of 18.04%, while small cap growth is the laggard with a gain of 5.75% this year.

The Morningstar UK Index, which covers more than 300 stocks with a market cap ranging in size from a few hundred million pounds to around £100 billion, gained 2% in May and is up nearly 12% in 2021 so far – compared with a loss of 11% in 2020.