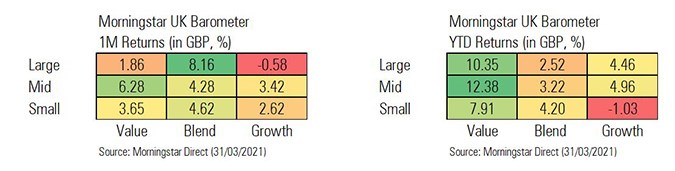

UK value stocks continue to outpace their growth rivals in 2021, according to the latest Morningstar Market Barometer, with large-cap companies gaining 10% so far this year on average. This trend is being played out worldwide as more economically sensitive stocks power ahead at the expense of last year’s winners, the high growth companies that thrived in the middle of the pandemic.

The Morningstar UK Index, which covers more than 300 stocks with a market cap ranging in size from a few hundred million pounds to around £100 billion, gained 2% in March and is up more than 5% in 2021 so far – compared with a loss of 11% in 2020.

But the contrast between the monthly performance of some of the large-cap companies highlights the ongoing divide between value and growth: in the value camp, shares in broadband provider BT (BT.A) rose 25% in March alone, whereas growth stalwart London Stock Exchange (LSEG) lost 27% in the month. Within the 12-company large-growth group, LSE’s loss is by far the greatest, with Ocado’s 7.5% fall the next largest. Despite BT’s price jump last month and a strong finish to 2020, the shares are still undervalued at 155p, according to Morningstar analysts, who assign the company a narrow economic moat and a fair value of 200p.

LSE Under Pressure

Wide-moat LSE started the year at nearly £100 per share but is now trading at £73, below its fair value of £78 per share. Other factors are at work here: the company’s purchase of data group Refinitiv has just gone through, and investors have started to worry about the cost of integrating the new acquisition. And large shareholders in LSE, including Canadian data giant Thomson Reuters (TRI) sold off a chunk of their shares in the London Stock Exhange last month, which has weighed on the price.

While large-cap growth stocks are the winner year to date with a gain of 10%, large-cap blend companies – which combine characteristics of growth and value stocks – were the biggest gainers in March with an average rise of more than 8%. All but one (silver miner Fresnillo (FRES)) of the 11 stocks in this group were in positive territory in March.

A booming UK housing market has helped mid-cap companies to an outstanding month, fuelled by an extension to the stamp duty holiday announced in the Budget in early March. Within the mid-cap value group of stocks, shares in housebuilders Vistry (VTY), Bellway (BWY) and Persimmon (PSN) were up 32%, 21% and 18% respectively in March alone, while DIY company and former stock of the week Kingfisher was up 20%, benefiting from stay-at-home DIY projects and the construction boom.

Mid-Caps Mixed

The 41 mid-growth companies in the Morningstar Index were a mixed bag: FTSE 250 tech firm Softcat (SCT) was the best of the bunch, gaining 23% in the month after a strong set of results, while 2020 IPO success story The Hut Group (THG) was among the month’s losers, falling 11% as investors turned their back on tech stocks. Overall, mid-cap growth stocks fared better than their large-cap counterparts in March.

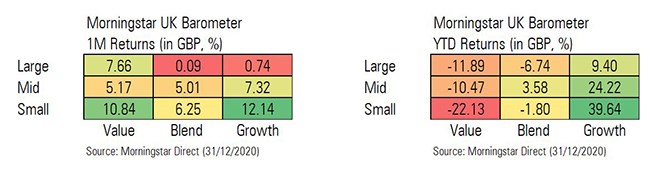

The success of value stocks so far this year is also reflected in the success of funds that invest in them, as shown by the performance of Morningstar’s best-rated funds in March and the top performing investments trust of the first quarter of 2021. But the re-valuation of value stocks should be put into the context of last year’s triumph for the growth style of investing, especially among smaller UK companies – our Barometer for 2020 showed that small-cap value stocks fell 22% while small-cap growth companies gained nearly 40%, a difference of around 62 percentage points. At this stage of the year, the difference between them is around 9 percentage points, in favour of value stocks.