It’s ESG week at Morningstar.co.uk and we’re looking at companies with exceptional commitment to the environment, society or corporate governance. Given a choice of four companies that fit the bill, our Twitter followers have chosen B&Q and Screwfix owner Kingfisher (KGF). This year’s events have been good for DIY companies: they were deemed “essential retailers” by the UK Government and could re-open in April, way ahead of other retail outlets. And with many of us stuck at home for a good chunk of this year, that home improvement project you’ve been putting off for years has been harder to avoid. Construction work has also been able to continue during lockdown, so firms have needed materials to build houses. A boom in house prices, spurred on by a stamp duty holiday, has pushed some homeowners to improve their properties before they go on the market.

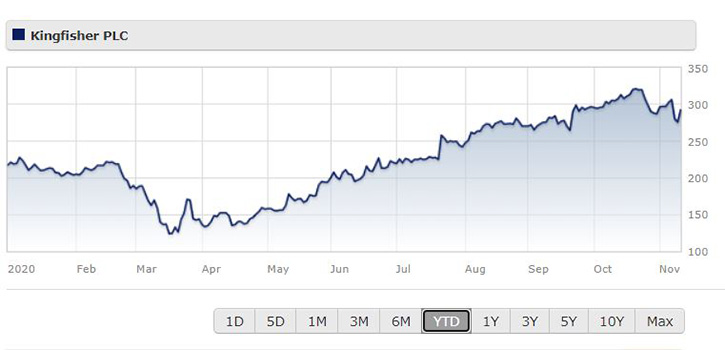

Kingfisher is one of a handful of FTSE 100 companies whose share price is higher than at the start of the year – shares started the year at 200p, got caught up in the March sell-off but have since powered on to break through 300p. This is still below the 10-year high above 400p seen in 2014. Despite this year’s surge, Morningstar analysts think that Kingfisher’s share are fairly valued at 295p. Looking at the most recent half-yearly results, analyst Matthew Donen says the pandemic year has boosted retail profits and accelerated the firm’s move online. The company has saved money because of Government measures to ease the economic impact of Covid-19 such as the furlough scheme and business rates relief. But Donen thinks these cost savings and demand boost is unlikely to be permanent, and kept the company’s fair value at 292p per share.

While people are unlikely to fall out of love with DIY any time soon, Donen notes a number of negative macro factors that are likely to drag on Kingfisher: “The do-it-yourself market in the United Kingdom has been plagued by low consumer confidence since 2016 due to Brexit uncertainty, resulting in low housing transactions and homeownership rates.” And the DIY market is highly competitive, with many online and bricks-and-mortar rivals keeping prices low and profit margins down. For that reason, Kingfisher lacks an economic moat. “Despite a leading market position in U.K. home improvement and a number-two position in France, the company has failed to translate leading market share into meaningful scale advantages or superior profitability,” Donen says.

From an ESG point of view, Kingfisher is one of an elite group of nine UK listed companies that have the lowest ESG risk, according to ratings agency Sustainalytics. (A full list of global companies with a “negligible” ESG risk is here). According to Sustainalytics, Kingfisher has an ESG risk rating of 9.6 out of 100, putting it top in the global Home Improvement Retail category and number three (out of 442) in world retailing. Globally, it ranks 75 out of 12,700 companies for low ESG risk rating.

“The company is at negligible risk of experiencing material financial impacts from ESG factors, due to its low exposure and strong management of material ESG issues. The company is noted for its strong corporate governance performance, which is reducing its overall risk. Furthermore, the company has not experienced significant controversies.”

Still, Sustainalytics says Kingfisher’s ESG disclosure lags behind best practice and is not in line with the “Global Reporting Initiative”, a common world standard for reporting ESG impacts.

Among Morningstar rated funds, Kingfisher makes up over 5% of the Silver-rated Jupiter Income Trust and 5% of Jupiter UK Special Situations, which has a Morningstar Analyst Rating of Gold. Kingfisher is held by a number of UK equity income funds, which have had a rough year in 2019. The company itself will not pay an interim dividend in 2020, and last paid a dividend a year ago (the interim payout for 2019/20)