Bond yields are picking up around the world. In the US, 10-year government bond yields have risen from 1% to 1.7% in less than two months. In Germany, the current yield on public bonds has risen from -0.57% to -0.37% since the end of January. While this may be welcome news to income-seekers, these shifts have caused investors to suffer losses on the bond portion of their portfolios.

But fund and ETF investors should not necessarily ditch these holdings, which can still provide a valuable protective buffer to stock market moves. Government bonds have performed well in past equity market downturns, giving stability to mixed portfolios in a way that corporate, high-yield or emerging market bonds cannot.

Riskier bonds may promise higher yields, but they typically behave like stocks. In financial jargon, this is called high correlation - that is, the prices of two different assets move in the same direction. But government bonds have a lower correlation to stocks than other bonds.

Bonds and Stocks Should not Move in Unison

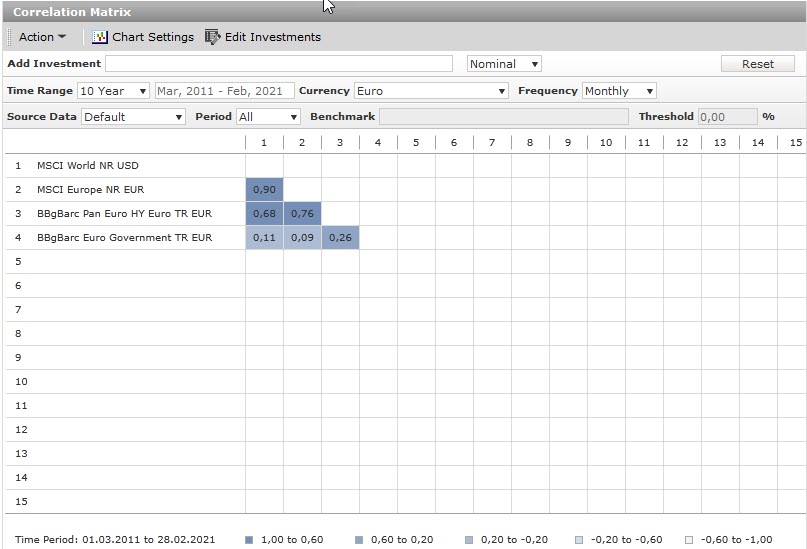

The chart below shows to what extent the prices of the MSCI World and MSCI Europe equity indices have moved in line with the prices of the two bond indices, the BBgBarclays Pan Euro High Yield index and the BBgBarclays Euro Government index, since 2011.

A correlation of between 0.6 and 1.0 is considered high, a correlation of 0.2 to 0.6 moderate, and a value between -0.2 and 0.2 is described as uncorrelated. Values significantly below 0 indicate a contrary direction of the prices of different assets and referred to as a negative correlation.

The correlation of equities and bonds since 2011

As the chart shows, equities have been strongly positively correlated over the past ten years. The MSCI World and the European equity index MSCI Europe largely moved in the same direction between 2011 and 2021, with a correlation of 0.9.

The high-yield index BBgBarclays Pan Euro High Yield behaved strikingly similar to equities during this phase. The correlation with the MSCI Europe was 0.76, while that with the MSCI World was still 0.68.

The movement of the government bond index, BBgBarclays Euro Government, however, was quite different, showing almost zero correlation with the MSCI World (0.11) and MSCI Europe (0.09). There was only a slight correlation with the high-yield index at 0.26. It shows that classic bonds diversify an equity portfolio much better than a high-yield investment.

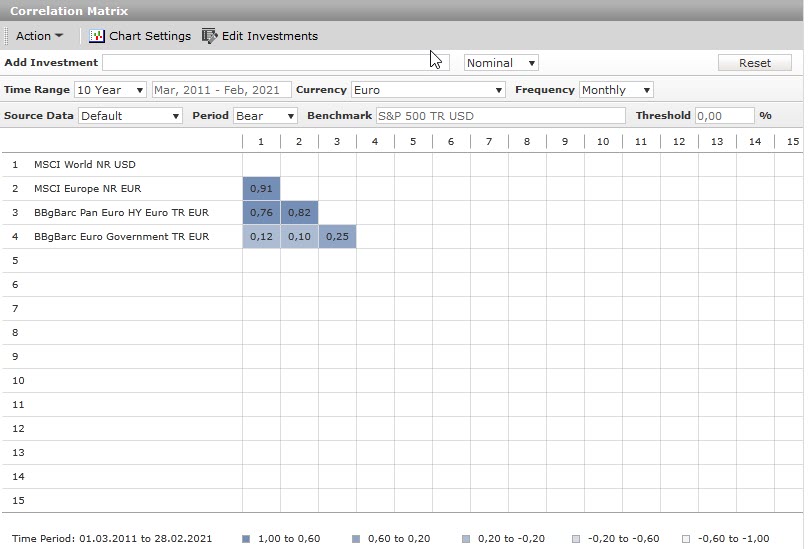

Next, let’s look at the relationship between the four indices in weak equity markets. The chart below shows the correlation of the stock indices with each other remained high (0.91), and the correlation of the high-yield index with the two stock indices increased to 0.76 and 0.82, respectively. The government bond index, meanwhile, maintained a low correlation of 0.12 to the MSCI World and 0.10 to the MSCI Europe.

The correlation of stocks and bonds since 2011 in bear markets

Bonds to Reduce Risk

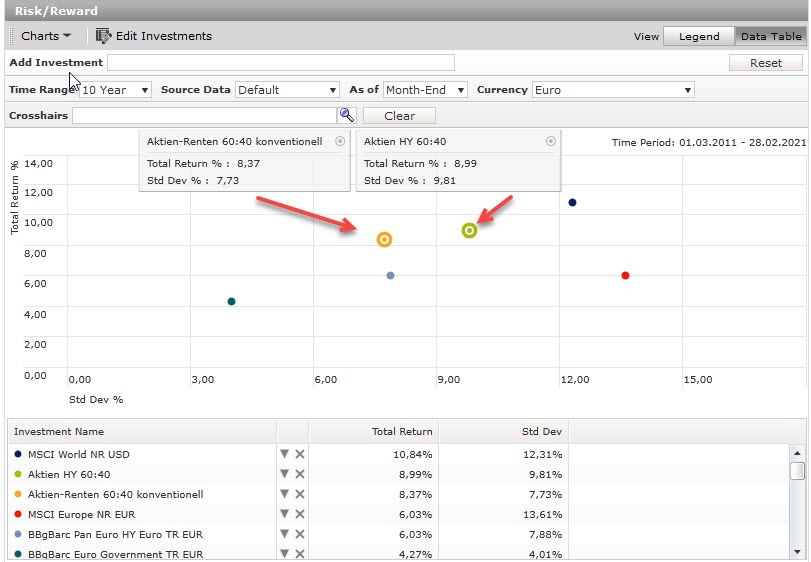

To show the impact of the bond factor on a mixed portfolio, let's now look at the volatility of the four indices over the same 10-year period. To show the effect of bonds in a portfolio, we look at two portfolios: a conventional 60% equity (MSCI World) 40% bond portfolio (BBgBarclays Euro Government Index), and a higher risk version, tracking the BBgBarclays Pan Euro High Yield index. THe performance of each is shown below.

The above graph shows the following: The equity indexes (red and navy blue) move far to the right of the scale, indicating that they are the riskiest of the six investments. The MSCI World is the most profitable index: over 10 years, it has generated annualised returns of almost 11%. European equities fluctuated more and returned less, at 6% a year since 2011, which is why the MSCI World is higher than the MSCI Europe on the chart.

It is now interesting to see how the risky blend portfolio behaves versus the blend portfolio. The volatility (indicated by standard deviation) of the risky portfolio is significantly higher than its conventional counterpart, where annual returns have fluctuated less over the 10 year period measure. Yet, interestingly, the returns of the two portfolios are not markedly different: the risky portfolio deliver annualised gains of 9%, compared to 8.4% for the conventional blend portfolio.

Conclusion

Bonds have been tricky to navigate in recent months but investors must keep in mind that they provide an important degree of protection to a portfolio, as well as the possibility of returns. Bonds can help offset volatility from equities, paticularly when markets are unpredictable. Even if the performance of bonds in the next few years is nowhere near as good as in the past decade, it does not mean they should be ousted from a portfolio, given their ability to provide ballast.

In turbulent market phases, when investors switch to "risk-off" mode, experience shows that not only stock market prices suffer but risky bonds will also move in tandem with equities. Those who abandon government bonds in favour of a higher-yield options may be taking on more risk than they realise.