With children about to return to school in England next month, education, education, education has been the theme of the latest stock of the week. Our Twitter followers have chosen FTSE 100 educational publisher Pearson (PSON) ahead of rivals.

Pearson was founded in the nineteenth century as construction company and is best known for owning the Financial Times newspaper and Penguin Books. 2015 was a watershed year for the company as, after a many years of buying stakes in other media and publishing firms, it announced it was focusing solely on education. Before the internet, publishing was a high-margin business with learners, schools and universities having no choice but to buy expensive textbooks and Pearson’s bumpy journey in recent years has reflected the disruption faced by the industry, and the company’s transition to a digital future. The shift to online learning during the pandemic, which has even further weakened the case for textbook-based education, has proved another obstacle for the company.

Short Squeeze

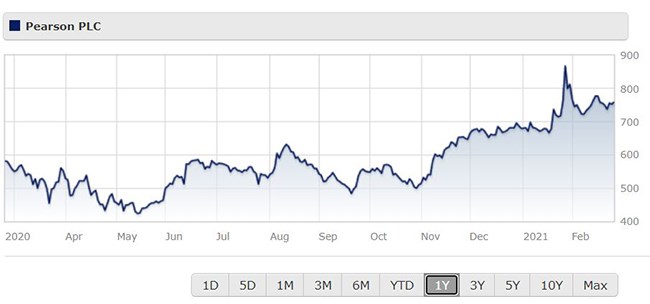

Despite all these challenges, the post-crash bounce in global markets has helped Pearson shares move back towards 2019 levels above 800p. Morningstar analysts say the stock is fairly valued at current levels, despite a 33% increase in the last year – and 16% increase in the last three months alone. Science textbooks seem a long way from the high drama of the GameStop surge, but Pearson may have been an unlikely beneficiary of the recent “short squeeze” in markets.

Pearson’s shares were some of the most shorted in the FTSE at the start of the year, but shares spiked 15% in the first few hours of trading on January 28, with 6 million shares changing hands that day - double the average trading volume. This spike resembles “short covering”, which involves traders going into the market to buy shares to cover positions, in case the prices rises dramatically (remember that they don't actually own the shares they are short of). Pearson shareholders have not been on the white-knuckle ride faced by investors in GameStop, but it’s interesting that in early February 8.5% of Pearson shares were being shorted and that has now fallen to 2.5%. “With short sellers of high-profile stocks now on edge, Pearson, was an obvious candidate for a swift, pre-emptive exit,” says Morningstar’s Michael Field.

Long-Term Potential

What about the company’s long-term prospects? Field says that the company is in strong position to capitalise on the disruption to education, it’s just that previous management has not yet been able to take advantage of this change (a new chief executive took over in October 2020). “We believe that the company's narrow moat, supported by its ability to generate valuable content, puts it in an advantageous position as the shift to digital and online education hits overdrive.” But shareholders are yet to be convinced, making Pearson more of a long-term story: “Scepticism on the part of investors as to the company's ability to effectively manage this change now is both fair and warranted, to some degree.”

One long-term backer of Pearson has been fund manager Nick Train, who admits that the company has not matched the success of outperforming holdings such as London Stock Exchange (LSEG) and Diageo (DGE). “Let me acknowledge that our longstanding and patience-testing holding Pearson is only up 70% since 1988 – not great over 32 years,” he said in the latest update for the Silver-rated Finsbury Growth & Income Trust (FGT). Still, Pearson makes up 1.4% of the trust, but more than 4% of the Lindsell Train Global Equity Fund, which also has a Morningstar Analyst Rating of Silver.

Pearson is also valued as an income stock and features around the top 5 on our monthly list of high yielding FTSE stocks, with a yield of nearly 3%, back up by a hefty dividend cover of 3. As a result, its held by a number of UK equity income funds, including Silver-rated Jupiter Income Trust, where it makes up nearly 5% of the portfolio.

.jpg)