Mini-bonds will no longer be sold to retail investors after the Financial Conduct Authority decided to make its ban on the controversial products permanent.

The FCA banned the sale of what it calls “speculative illiquid securities” in January after a number of scandals in which the companies selling the bonds have gone under, losing investors significant sums. The most high profile of these was the collapse of London Capital & Finance, which went into administration in 2019, putting at risk £230 million invested by more than 11,000 people. Just 1% of these investments are eligible for redress under the Financial Services Compensation Scheme (FSCS) as most investors bought the mini-bonds after switching out of regulated products such as Stocks & Shares Isas.

Mini-bonds offer investors fixed interest payments and then invest the money in a range of illiquid assets like property schemes. Like conventional bonds, they also offer the investor their initial investment back at the end of the term. Investors were lured in by interest rates of 8%, much higher than for cash savings accounts, and in many cases they thought their capital was completely safe.

The products are often enticing to investors because they offer much higher rates of interest than are available elsewhere. One scheme, backed by Grand Designs host Kevin McCloud, offered interest of 9% for investors putting money into its eco-housing developments. It collapsed into administration last year.

Manchester-based Blackmore Bond is the latest firm in the sector to call in administrators after it collapsed in April this year. It raised more than £45 million from investors, who were asked for a minimum of £5,000 and the money was the invested in a range of property development projects. Investors were enticed by returns of up to 10% on these bonds, which were marketed by Surge Group, which has links to London Capital & Finance. Administrators have warned investors in Blackmore Bond they face a “substantial shortfall” as the firm is wound up.

“By making the ban permanent we aim to prevent people investing in complex, high risk products which are often designed to be hard to understand,” says Sheldon Mills, interim executive director of strategy and competition at the FCA. The ban was due to run until the end of December 2020.

FCA Review Delayed

Mills says that since the ban was first introduced in January, some firms have tried to get around it by promoting high-risk bonds not covered in the scope of the original rules. As a result, the FCA is now proposing to widen the scope of the ban even further to capture these new products.

Mini-bonds are just one product covered under the current ban and the FCA defines these as “complex and opaque arrangements where the funds raised are used to lend to a third party, or to buy or acquire investments, or to buy or fund the construction of property”.

The products will still be able to be marketed by authorised firms to sophisticated or high net worth investors as long as they include risk warnings and a full explanation of costs.

Adrian Lowcock, head of personal investing at Willis Owen, welcomed the permanent ban and said it was long overdue: "The difficulty in getting your money back, or even having visibility of how your money is being used by the issuer of the bonds, was a very real problem, and this blanket ban on marketing them to retail investors should ensure fewer individuals end up investing in products that few truly understand."

The conduct of the FCA itself over its role in the LC&F scandal is under scrutiny. The Government has commissioned an independent review into how the regulator handled the collapse of the company. Dame Elizabeth Gloster, who is heading up the investigation, was expected to complete this review by early July this year but this will now be finished in September at the earliest.

Risk Assessments

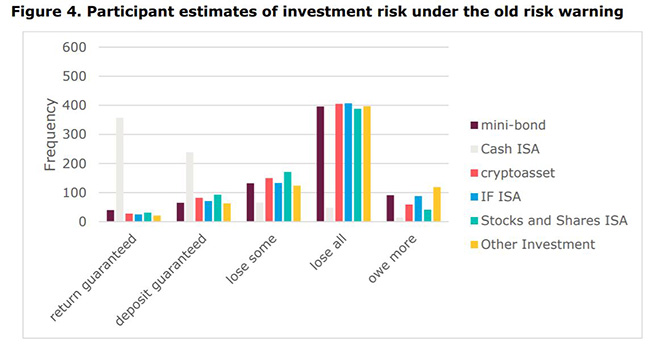

The FCA has just put out a survey of investor attitudes to risk called "Choosing Wisely" and it looks at how people respond to different risk warnings of loss of capital. Without the warnings "You could lose all of your money" and "This is a high-risk investment", investors preferred mini-bonds over Stocks and Shares Isas.

More people thought returns were guaranteed for mini-bonds than for Stocks and Shares Isas, crypto assets and Innovate Finance Isas without the risk warning. This changes when respondents are asked whether they think their deposit is guaranteed: more people thought this was the case for Stocks and Shares Isas, IF Isas and crypto assets than for mini-bonds. When asked if they thought they would lose some of their money, more people thought this was the case for Stocks and Shares Isas than for mini-bonds. Cash Isas score much more highly than rivals for "return guaranteed" and "deposit guaranteed", as you would expect, but worryingly respondents also thought they could lose some or all of their money - and indeed owe more - by putting their money in Cash Isas. (Almost all Cash Isas on the market are covered by the FSCS scheme, which guarantees savings up to £85,000).

For the key question whether the investments are likely to see people lose all of their money, all investments apart from Cash Isas have similar scores, although Innovative Finance Isas are rated just above mini-bonds in terms of risk.

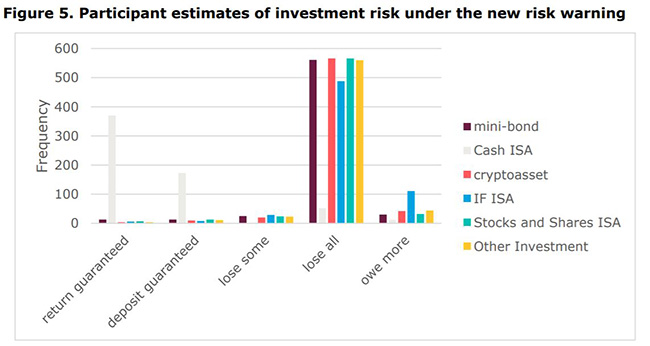

With the risk warning, the perception that deposits and returns are guaranteed drops significantly for mini-bonds and other investments. Still, Stocks and Shares Isas (and crypto assets) are considered marginally more risky than mini-bonds in terms of losing your whole investment. Many mini-bond adverts failed to mention that capital was at risk at all or buried the warning in small print in terms and conditions.