Investment trusts have been caught up in the wave of selling along with company shares, funds and ETFs. But how have Morningstar’s best rated trusts fared during the sell-off? We look at how the sharp falls in share prices have affected these trusts’ premiums and discount.

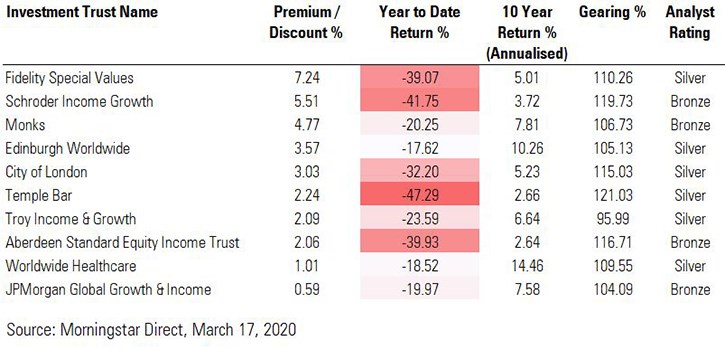

Looking at Morningstar Direct data, Silver-rated Fidelity Special Values (FSV) is sitting at the biggest premium, at 7.24%, among trusts rated by our analysts as Neutral and above. The trust, which is managed by Alex Wright and focuses on turnaround and recovery opportunities, has fallen nearly 40% in the year to date – its benchmark, the FTSE All-Share is down 34% since the start of January.

An investment trust trades either above, below or at its Net Asset Value, which is the underlying value of the trust’s assets; that it is known as trading at a premium (above the NAV) or discount (below the NAV). In-demand trusts in “hot” sectors like technology often trade at a premium to reflect high investor buying interest; those out of favour, such as the Woodford Patient Capital Trust in 2019, often trade at a discount. When out-of-favour trusts turn things around, the discount turns to a premium and investors can benefit from this change of fortune – as well as making money on the uplift in the share price.

Is it Worth Paying a Premium?

Silver-rated names in the list include Monks (MNKS), Edinburgh Worldwide (EWI), Temple Bar (TMPL) and Troy Income & Growth (TIGT). It suggests a "flight to safety" as investors shun Asia-focused investment trusts and look to trusts they believe can be relied upon for an income even during turbulent times.

Indeed, it's noticeable that half of the names on the top 10 premium list are equity income trusts and a number are so-called “dividend heroes”, which they have raised their dividends for at least 20 years in a row. The City of London trust (CTY), which was this week upgraded to a Gold Morningstar Analyst Rating, has grown its dividend for more than 50 years in a row. The trust is run by veteran fund manager Job Curtis and is sitting at a premium of 3%. Temple Bar, which has a Morningstar Analyst Rating of Silver, is another dividend hero along with Schroder Income Growth (SCF).

While some investors may assume it's worth paying a premium for a fund that could protect them, year to date performance suggests that may not be the case. Four of the trusts at trading at the highest premiums have fallen an eye-watering 39% or more so far this year.

While some investors may assume it's worth paying a premium for a fund that could protect them, year to date performance suggests that may not be the case. Four of the trusts at trading at the highest premiums have fallen an eye-watering 39% or more so far this year.

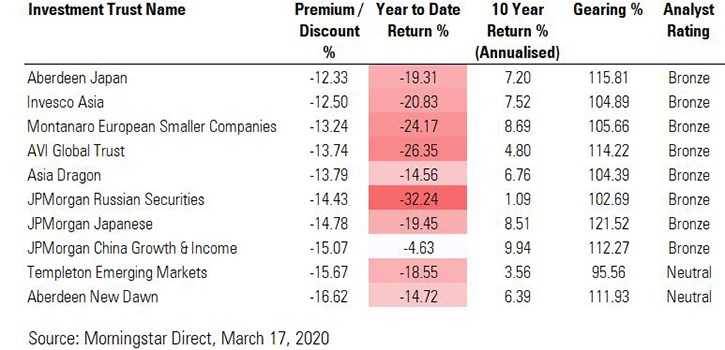

In contrast, the greatest faller among trusts at the widest discounts is down 32%. The biggest discount on the list is Aberdeen New Dawn (ABD), which is trading 16% below its Net Asset Value (NAV), but it has only fallen 14% in the year to date, despite the bloodbath in emerging market stocks. The rest of the most-discounted trusts are mainly (and predictably) Asia-focused, given the fallout from the coronavirus has been felt most immediately there.

There are three Gold-rated trusts trading at a discount: Personal Assets (PNL), Schroder Asia Total Return (ATR) and Pacific Assets (PAC), another trust which has recently been upgraded to Gold by Morningstar analysts.

Has Gearing Made Things Worse?

One additional factor to consider in the current market sell-off is the level of gearing used by trusts. This is the borrowing that investment trust companies can take on to enhance returns during boom times. This isn’t an option for open-ended funds, which can limit returns in bull markets, but can become a liability in a market meltdown.

Here the pattern is less clearcut in that nine out of 10 of the trusts with the biggest premiums use gearing – and so do those with the biggest discounts. The most geared trust in the list of top 10 premiums, Temple Bar, has fallen 47% this year – but JP Morgan Japan (JFJ) also had gearing above 120% and its share price has fallen 19% so far this year. Ie. Higher gearing hasn’t necessarily led to worse performance in the current sell-off.

What investors need to weigh up is that the risk/reward of buying a trust at a discount or a premium – in terms of risk a trust at a premium can swing to discount, making a positive return more of an uphill climb, whereas a trust at a significant discount can see that widen even further. In terms of reward, a heavily discount trust moving to a premium can provide significant uplift to returns. In current market conditions, it's very difficult to get this right.