The US has outperformed Europe economically for some time now, but Europe’s weakness might be its strength. There now lies little in the way for the European Central Bank to cut rates, which may come sooner and harder than in the US. On our valuation, European equity markets are fairly valued, but positive sentiment is a powerful force and could potentially drive equity markets higher in 2024.

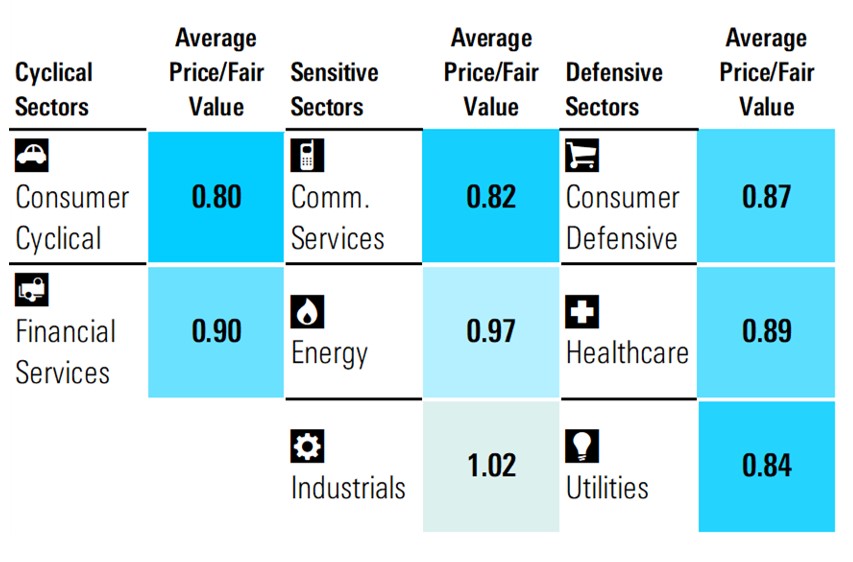

The valuation picture across the sectors is very mixed, and cuts to interest rates could be the catalyst for further disruption here. Financials, which had benefited from higher rates could experience some negative effects, while the utilities and consumer sectors could be large beneficiaries.

I can’t recall a period in time when the words of central bankers, and individual economic data releases, no matter how mundane, have held so much significance in the eyes of investors. On our valuations, both the US and European markets are fairly valued. That is despite relatively weak economic growth, high levels of government debt, and a cost-of-living crisis in both regions.

So why are market valuations elevated despite all of these obvious negatives? Essentially investors are seeing through the current malaise and eagerly anticipating interest rate cuts from the near-record highs we are experiencing now. How soon these interest rate cuts come however, is heavily dependent on a number of factors.

So how is the economy faring up, and are central bankers in a realistic position to cut rates soon? In the US, inflation is hovering at just over 3%. A large climbdown from the more than 9% levels witnessed not two years ago, but still more than 50% above the Federal Reserve’s targeted level. In Europe, inflation has fallen harder and faster, with the most recent reading showing inflation at just 2.6%. Still some way off that key 2% level, but the momentum and trajectory of the fall appears to be slowly chipping away at the European Central Bank’s concerns around a resurgence in inflation.

Europe Won't See Much Growth in 2024

Another concern of central banks was that cutting interest rates at this point might exacerbate an overheating economy. In the US, GDP currently sits north of 3%, a more robust performance than many economists had predicted last year. This contrasts sharply with the eurozone, where GDP growth is currently flat, having actually turned negative in the third quarter of 2023. For the most part, neither situation should deter central bankers from cutting rates. In the US, our forecasts point to an encouraging, but modest, 2% growth in 2024. While for Europe, the economy is unlikely to grow at all in 2024.

Central banks rely heavily on labour market indicators to understand the potential of the economy to overheat. When these markets are tight, wage growth can be a strong driver of inflation. Once again, the situations in Europe and the US diverge from each other. Both have seen a strong uptick in employment numbers over the last three years, but for the US the change has been more pronounced. Unemployment has ticked up from its early 2023 lows, but remains below 4% in the US. In Europe, where unemployment is structurally higher than the US, the number sits at historical lows of 6.4%. While neither number raises any material flags for central banks, there is certainly less of a danger of resurgent wage inflation in Europe.

Rate Cut Forecasts Can Change Again

Our current stance is that the Federal Reserve will cut rates in June, with the most recent Reuters poll of economists also predicting the ECB will cut at the same time. But if we’ve learned anything over the last 12 months it’s that rate cut expectations often get pushed out, and rarely pulled in.

Ultimately the risks to cutting are much lower for the ECB than the Fed, with Europe’s economy more likely to deteriorate further than overheat any time soon. So, if the ECB does in fact cut rates ahead of the Fed, how will this affect European equity markets?

Certainly any large stimulus, in the form of rate cuts, is good news for the economy, which should ultimately filter through to improved corporate profitability. So, while we believe that equity markets in Europe are fairly valued currently, further inflows to markets from enthused investors could push markets higher.

Which Stock Sectors to Look Out For?

• Financials, which saw a material boost over the period of high interest rates, could come under pressure in some areas, namely banks and insurance companies.

• Both consumer sectors have been beaten up of late, as sales growth has come under pressure after a sustained period of high inflation, with many consumers struggling to afford higher costs. Rate cuts will filter down to lower mortgage rates and should slowly alleviate the pressure on consumers and consumer-facing firms.

• Utilities, a sector many investors shied away from as bonds offered equally attractive yields, could swiftly come back into fashion. The European utility sector pays a dividend north of 4.5% and trades at a 20% discount to fair value too.

Michael Field is Morningstar's European market strategist

.jpg)