Paradigms are powerful, but they also tend to die embarrassing deaths. At the end of 2021 the rough consensus of central banks and analysts was inflation would be "transitory".

They were wrong.

Today, the phrase du jour is "higher for longer", a middle-ground scenario that pushes runaway price rises out the window but also fails to immediately return inflation to central bank targets. Like Covid-19, it is another thing we are going to have to learn to live with.

Having called the situation incorrectly so many times, the voice of Bank of England (BoE) governor Andrew Bailey may not be one that markets really want to listen to, but as Jeremy Hunt was delivering the UK’s Autumn Statement speech last month, Bailey was quietly frank with the Treasury Select Committee, whose inquiries into UK finance and regulation remain one of the few political finance theatres still worth listening to.

Markets are, Bailey said, underestimating the threat inflation poses. So as another year ends and talk turns to the risks and opportunities investors face in 2024, it's prudent to ask whether the issue is widespread. Moreover, investors deserve to have some semblance of how they can take advantage of it – if they can at all.

What Are the Professionals Saying?

Views on interest rate cuts differ. Markets expect a hold on interest rates tomorrow when the Bank of England and European Central Bank (ECB) make their next monetary policy moves, but it’s worth a note of caution here. For its part, the UK's Monetary Policy Committee (MPC) has wrong-footed investors once already this year. That could happen again.

Regardless, either outcome will still foster of talk of when rate cuts are coming. But not even that is simple. As RWC Bluebay has already suggested, central banks – and the BoE in particular – could commence another hiking cycle in 2024 if the data looks unfavourable. One step forward. Two steps back.

"Should inflation remain problematic, as RBC BlueBay expects, there remains the risk Bailey and colleagues may re-start a policy tightening cycle later next year, after holding policy on pause for the time being," it says.

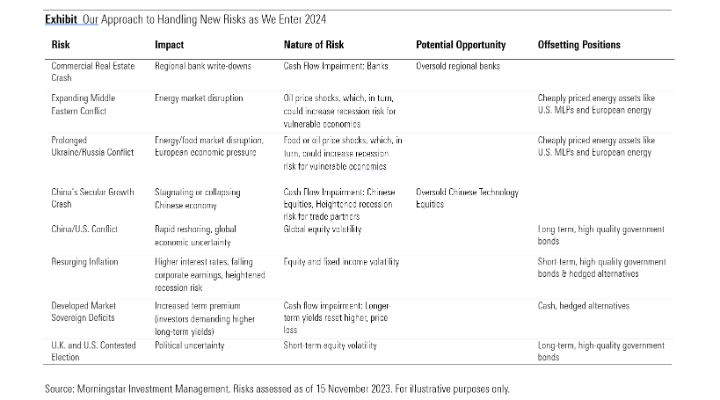

By way of comparison, Morningstar Investment Management (MIM) expects cuts by the second half of next year. That does not necessarily discount the possibility of hikes beforehand, but it certainly highlights the case for a much slower return to target.

"We expect further economic change in 2024. Europe and the UK remain fragile economically. Against this backdrop, it is plausible for central banks to cut rates from mid-2024 and into 2025," it says in its 2024 outlook.

The tension between immediacy and effect here are obvious. Market reactions to events tend to be almost instantaneous, so it's easy to see how falling inflation last month tempted some to think the battle was nearly over. It takes time for rate rises to feed through, however, rendering the fight slower and more frustrating.

As MIM implies, we could still be talking about this issue in a year’s time. For its part, the Office for Budget Responsibility now doesn't think inflation will fall to the BoE’s 2% target until 2025. For now, interest rates sit at 5.25%. The Eurozone has them at 4.5%.

How do I Turn Interest Rates to my Advantage?

There are plenty of ways to invest smartly now interest rates are higher.

First thoughts turn to fixed income, and in particular short-dated bonds, which are yielding above fair value for the first time since the financial crisis of 2008. That renders them, in the words of MIM, "a compelling investment choice". But it applies to corporate debt too, as more companies borrow for shorter periods. Longer-dated bonds, meanwhile, should offer an effective hedge in most macroeconomic circumstances.

"The shape of the yield curve is an important consideration here," MIM adds.

"Despite the 'higher for longer' narrative, we still see an inverted yield curve, where we can capture higher yields for bonds that mature in the short term, while those that mature in 10+ years’ time continue to be less attractive."

But there are risks too. Supply affects demand.

"The first is that we must weigh the increase in bond supply – especially a US Treasury maturity wall – which can significantly affect the market by amplifying the volume of bonds," MIM says.

"The US Treasury Department has confirmed the need to borrow more than $800 billion (£637 billion) in the first quarter of 2024, which could test the appetite of investors. All else being equal, this could result in higher yields."

To balance this out, equity investing – and specifically dividend investing – can really help the core part of your portfolio, but here MIM urges caution, and not just because of dividend uncertainty.

In a volatile environment, company fundamentals are subject to meaningful change. Revenue and earnings growth are now in decline, while interest coverage has also edged lower. This means companies may struggle to repay their debts.

This may also affect investors keen to beat inflation through dividend investing. If you're thinking of being a dividend chaser next year, a sprinkling of caution may help you.

"For investors who utilise rule-based vehicles such as active exchange-traded funds to access high dividend names, many dividend indexes can experience big shifts in the sector composition. Investors [also] need to be mindful of sector exposure they are getting," MIM argues.

"Moreover, while dividends remain a key area to explore and we express this in our portfolios, we do note dividend instability could potentially pose a risk to income investors. Sectors such as energy and financials are more prone to dividend cuts during downturns."

60/40: Even Less Dead Than Before

If it's risk you're talking about, however, there's also the question of risk appetite, and therefore of portfolio construction and rebalancing.

Just two years ago, commentators were predicting the death of the 60/40 "balanced" portfolio, while the acronym "TINA" – meaning "there is no alternative (to stocks)" – was giving equity investors a warm feeling in their bellies. Not so now. Reports of the concept's death have been greatly exaggerated.

Today, volatility and higher interest rates make balanced portfolios look much more attractive. Even if the world outside looks turbulent, there is no need to make your own portfolio mirror the weather. That goes for cash allocations too, which are a useful hedge until they aren't anymore. Bonds look better, both for risk and yield.

"The case for the 60/40 portfolio is stronger than in recent memory," a note from Vanguard reads.

"Long-term investors in balanced portfolios have seen a dramatic rise in the probability of achieving a 10-year annualised return of at least 7%, from a 9% likelihood in 2021 to 39% today."

MIM agrees, saying the merits of playing around with with your portfolio ratios are "overstated".

"The reset in base rates has brought into question the changing merits of a balanced portfolio (for example, 60% in stocks, 40% in bonds, or equivalent mixes), which we believe are likely overstated.

"In our view, the merit of a balanced portfolio has improved following the increase in yields."

Nobody is saying that this central paradigm of investing will never change or be deconstructed, then, but for now it is a very healthy starting point in a very uncertain world.