As we enter the fourth quarter, European equity markets are desperately clinging on to relatively elevated valuations, despite a negative macroeconomic backdrop. What should investors expect in Q4 and where are the opportunities?

Growth is barely hovering above zero across the Eurozone, manufacturing is declining, and inflation is falling but remains high. Despite this negative economic backdrop, equity markets aren’t cheap, and are trading just 5% shy of our fair value estimates.

So why are valuations still high when the macroeconomic backdrop looks so terrible? In a word, hope. Investors are hopeful that while things look bad now, that they will improve over the next nine-to-12 months. Further declines in inflation will mean that central banks can take their foot off the brake and lower interest rates once again, allowing the economy to run uninhibited. Labour markets across the developed world remain tight. While businesses face pain in the meantime, mass layoffs are unlikely to happen, meaning we are less likely to enter a full-blown recession.

Sticky Inflation

The one hitch with this plan lies in the assumption that inflation will continue to fall rapidly. After the significant fall in inflation we have already seen, we are now left with core inflation, which is notoriously sticky. Getting down to central banks’ targeted inflation rate of 2% may take significant time, and potentially further interest rate increases. With the European economy barely growing, this could be enough to properly send us into a recession.

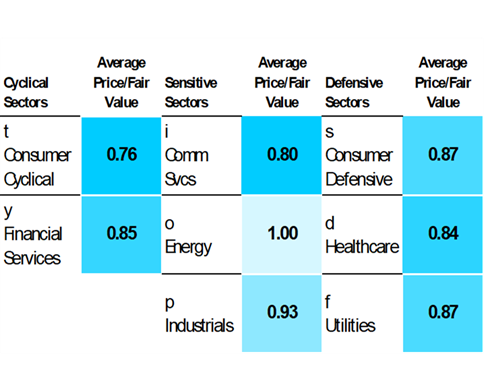

Despite markets close to being fairly valued, there is a huge disparity in valuations across the various sectors. While energy is now fairly valued, consumer cyclicals offer more than 30% upside. Gaps are opening up too in other sectors. Utilities, which were close to being fairly valued earlier this year, now offer about 15% upside potential. Likewise, some of the more defensive sectors such as healthcare and consumer defensive are offering investors a better deal, with valuations having fallen over the quarter.

Utilities is one of the highest dividend-paying sectors in Europe, with traditionally stable and relatively known revenues. When interest rates were low, a dividend of 5% attractive to investors, but now as the return on 10-year government bonds (essentially guaranteed money) approaches 4%, utility dividends look relatively less attractive, leading to outflows from investors. With valuations having fallen, however, we now see a host of opportunities in the sector.

Energy Security in Winter 2023/2024

Staying with the theme of energy, we recently published a deep dive into energy security in Europe, a hot topic last year as we entered winter, not knowing if Europe could keep the lights on without Russian power. This time around we think the EU is in great shape, with storage levels close to full as of the end of September. This scould quickly change however, particularly if this winter is harsher than the last. So we remain vigilant.

Thinking past this winter, what about RePowerEU, the region’s plan to wean itself off Russian gas? While the EU has made huge steps in reducing the exposure to Russian gas, we’ve been cheating somewhat by increasing our consumption of Russian LNG imports. This is something that needs to be addressed by the EU soon, if it genuinely wants to reduce reliance on Russia.

Inflation has come down significantly since this time last year. The good news is that this effect is finally flowing through to businesses, many of whom are already feeling the benefit of falling costs. This is particularly true of businesses with economic moats, like some capital goods firms in the industrial segments. Many of these firms have exposure to secular growth themes such as electrification and automation, and most importantly, they have some degree of pricing power. Although costs are falling, they should for the most part be able to keep prices steady, meaning fatter operating margins in the coming months, an investor’s dream scenario.

.jpg)

.jpg)