I have not previously written about thematic investing. My mistake. I should have cautioned against such funds three years ago because warnings should be issued during upswings. But the truth is, at that time I paid them little attention.

I ignored thematic investing because I did not expect the marketplace to bite. Thematic funds are repackaged sector funds. True, supporters of thematic investing claim their funds are different and better.

For example, Schwab states, "in contrast to sector investing, [thematic investing] includes investments that span many sectors, such as the Workplace Diversity Leaders theme ... bringing together a variety of companies from tech, retail, gaming, hospitality, and more".

Perhaps in that case, but most theme funds are more narrowly constructed, as Schwab’s next sentence confesses.

"Thematic investing lets you align your investments with personal interests and values, including themes like space economy, genomics, cybersecurity, and many others".

The truth comes out. Theoretically, theme funds might "span" several sectors, but in practice, most occupy the relatively small portion that is devoted to futuristic technologies.

That is very old wine, sold in new bottles. As Morningstar’s Ben Johnson reminds us, futurist funds are septuagenarians. The Television Fund (!) made its debut in 1948. The next decade brought Atomic Development Fund; Science and Nuclear Fund; Nucleonics, Chemistry & Electronics Shares; and the Missiles-Rockets-Jets & Automation Fund. They were followed by the infamous Steadman Oceanographic & Growth Fund. (Inspired by Jacques Cousteau, apparently.)

Rejecting Bogle

That you have not heard of such funds, save perhaps for Steadman, suggests all one needs to know about high-concept sector funds: they fizzle. Those from our grandparents' generation did, as did those from our parents’ time. So will the current incarnation.

Over time, the sectors (sorry, "themes") change but the story does not. Buying the current headlines was, is, and always will be a mug’s game. As somebody once said: "if the bozos know about it, it won’t work anymore".

I thought investors would have learned that lesson by now. In the past, fund buyers were doomed to repeat history because of a lack of information. They lacked the data to disprove tempting narratives. That no longer holds.

Also, thematic investing contradicts the currently dominant practice of indexing. Theme funds charge a premium to hold risky portfolios with the promise that today’s extra cost will become tomorrow’s extra profits. Jack Bogle directly preached against such hopes.

A Sales Boom

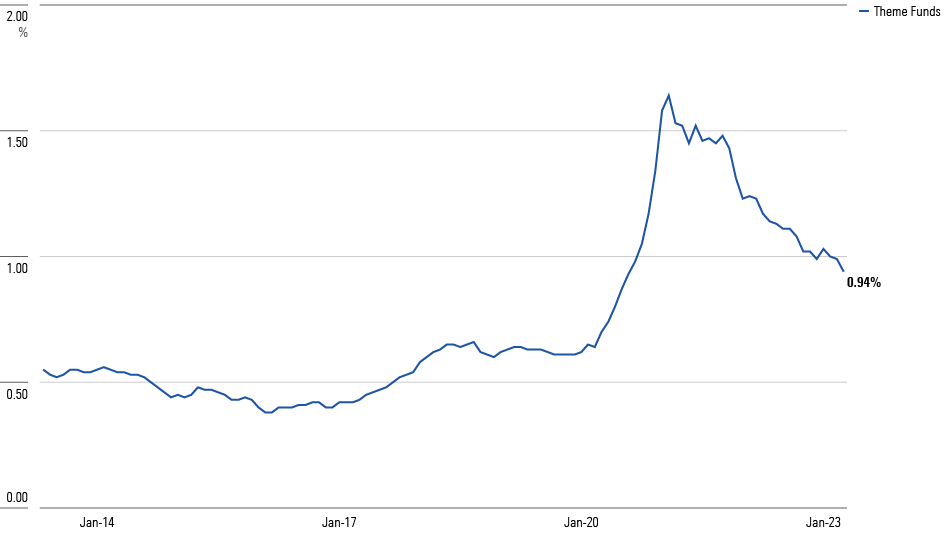

My analysis underestimated the public’s appetite for gambling. Although muted during bear markets, this inclination continues to emerge during bull markets, the triumph of Jack Bogle’s gospel notwithstanding. And when optimism (and the prices of US stocks) surged in summer 2020, so did the coffers of theme funds. By early 2021, the market share of thematic investing, as measured by its percentage of US equity fund assets (both open-end and exchange-traded funds) had nearly tripled.

To be sure, at a peak share of 1.64%, thematic investing was a minor segment of the fund industry. It never mounted a serious challenge to the trillions of dollars parked in conventional equity funds. However, thematic investing did record significant sales. For the six months ending February 2021, theme funds received a net $64 billion. That’s good money even by Vanguard’s standards.

ARK’s Influence

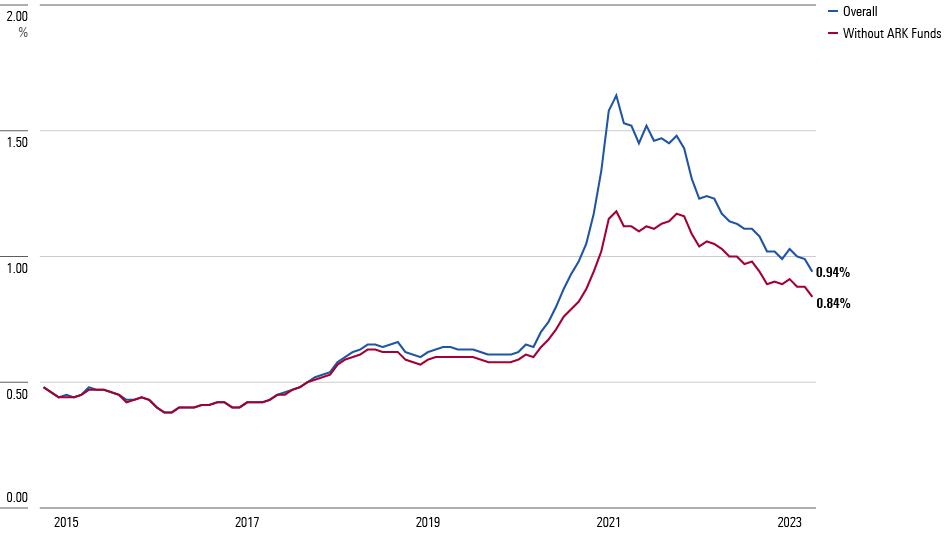

These figures raise the question: how much of the sales increase was attributable to ARK Funds? During that very time, Cathie Wood’s almost comically thematic investments – Innovation, Genomic Revolution, Next Generation Internet, and so forth – were the talk of the fund world. Perhaps the apparent popularity of theme funds merely reflects the rise (and subsequent fall) of the ARK Fund family.

It should be easy enough to test that proposition: Rerun the previous study while omitting the ARK products.

By this measure, the market share for thematic investing doubled rather than tripled. That is, the ARK funds were responsible for half the sales increase, while other thematic investors generated the other half. Although less dramatic, the pattern excluding the ARK funds still stands: Theme funds were briefly the rage.

Performance Problems

Then came 2022, which convincingly demonstrated that most thematic investors were not, in fact, as well diversified as implied by Schwab’s description. On average, thematic funds dropped 30.1% on the year, more than 10 percentage points worse than the 10.4% loss suffered by the Morningstar US Market Index. Their returns also trailed those of the average small growth fund. Consequently, since April 2022 theme funds have suffered net monthly redemptions.

Of course, one should not condemn funds for a single bad year any more than praise them for a single good year. A longer perspective is required. Unfortunately for theme funds, the longer perspective is also unkind. Below are the annualised total returns for thematic investors since 2017 (when enough theme funds existed to merit computing an average) compared with the stock market average.

To call those results disappointing would be an understatement. Miserable is more like it. Not only have thematic investors sharply lagged the overall marketplace, returning a cumulative 63% as opposed to the index’s 103%, but their successes have been fleeting.

Last year was no anomaly. In 2018, 2019, 2021, 2022, and again so far this year, theme funds trailed the market average. Higher risk + lower aggregate returns + fewer bright spots = investment failure.

On a dollar-weighted basis, the results have been worse yet. Morningstar’s Amy Arnott has delivered the sad news that because most ARK Innovation ETF ARKK shareholders bought near the top, the aggregate return for the company’s flagship fund has been deeply negative. Quite literally, since that ETF was founded, it has lost more money for its shareholders than it has made. The same principle applies to the rest of thematic investing, albeit on a lesser scale.

As such, thematic investing appeals to the worst investor instinct: the desire, based on the combination of avarice and undue self-confidence, to outdo one’s neighbor while knowing no more than one’s neighbor. (That artificial intelligence is the next technological revolution, or whatever.) I had thought that indexing’s overwhelming popularity had eliminated such tendencies. Not so.

Let this be a belated reminder to us all that the odds remain firmly against such endeavours.

John Rekenthaler is director of research for Morningstar Research Services

{kind=link}

{kind=link}