After taking a hit in last year’s bear market, video game stocks are trading at what gamers might call "S-tier" attractive prices. S-tier is a ranking reserved for the best, most powerful characters in a game.

These stocks include some of the biggest names in industry, such as Nintendo NTDOY and Roblox RBLX.

To look for undervalued gaming stocks, we turned to the Morningstar Global Electronic Gaming and Multimedia Index, which tracks global companies that develop or publish video games and other multimedia software applications, including personal computers, video game systems, cellphones, tablets, and other portable media players.

Heading into 2022, video game stocks had seen strong returns stemming from the pandemic. With many people stuck inside, they were looking for a way to distract themselves.

But for gaming-stock investors, those gains turned out to be an "early gg call," which in gamer lingo means saying "good game" before the game is over. With the world reopening, many players do not have the same free time they used to have, and many stocks "got sent back to the lobby."

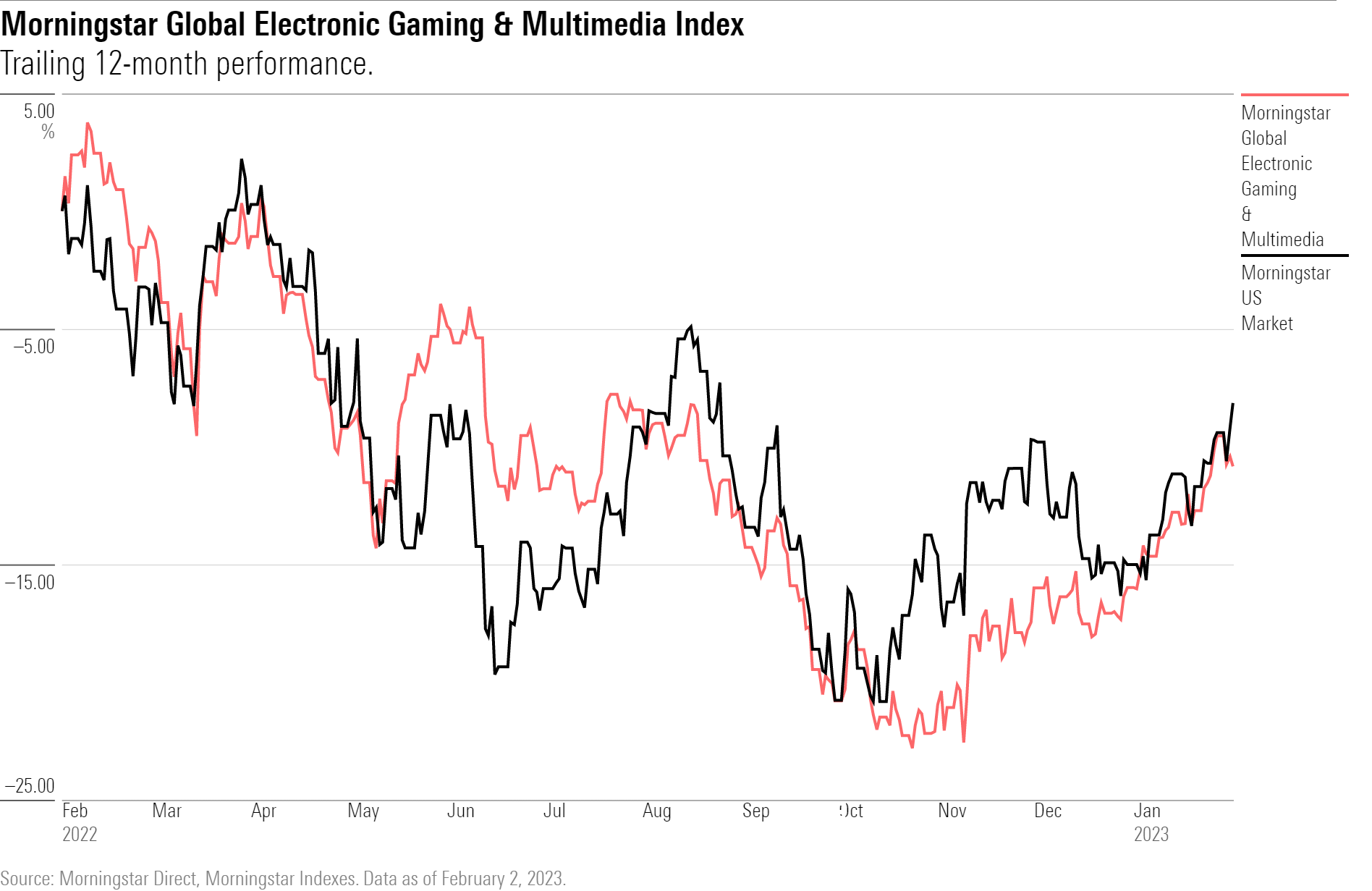

As of February 2 this year, the Morningstar Global Electronic Gaming and Multimedia Index lost 10.8% for the trailing 12-month period, while the broader stock market fell 8.2%, as measured by the Morningstar US Market Index. During 2022, the gaming index fell 16.1%, outperforming the 20.7% decline in the overall US stock market.

Undervalued Gaming Stocks' 'Tier List'

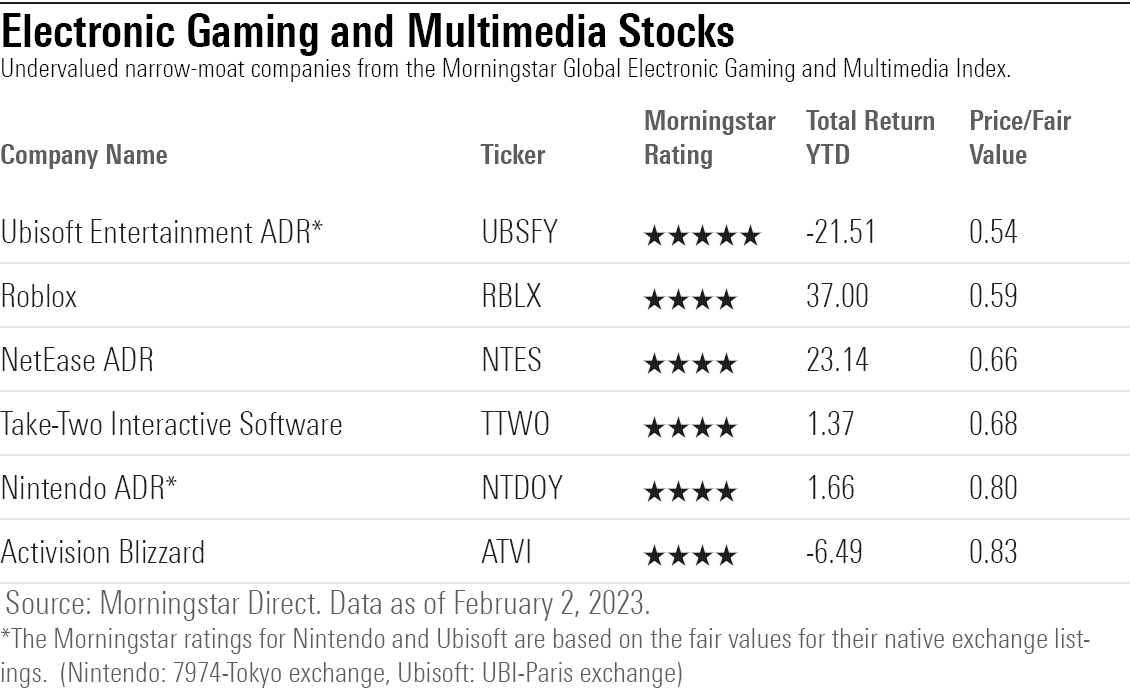

For this article, we looked for the most undervalued stocks in the Morningstar Global Electronic Gaming and Multimedia Index by screening for those that currently carry a Morningstar Rating of 4 or 5 stars and a Morningstar Economic Moat Rating of narrow.

Of the 51 video game stocks in this index, only six are covered by Morningstar analysts, and all of these were undervalued as of 2 February 2023.

• Ubisoft Entertainment UBSFY

• Roblox

• NetEase NTES

• Take-Two Interactive Software TTWO

• Nintendo

• Activision Blizzard ATVI

The most undervalued video game stock is Ubisoft, an entertainment developer, trading at a 46% discount to Morningstar’s fair value estimate. The least undervalued on the list is Activision, trading at a 17% discount. Ubisoft Entertainment, NetEase, and Nintendo are based outside the United States.

Ubisoft Entertainment

• Fair Value Estimate: $7.50

• Total Return Year to Date: -21.51%

Ubisoft announced weak fiscal third-quarter results because of much lower-than-expected sales of both Mario + Rabbids: Sparks of Hope and Just Dance 2023 in December and early January. Management slashed net bookings guidance for the quarter to EUR 725 million from EUR 830 million. For the full fiscal year, it cut expectations from "more than 10% growth" to "more than 10% decline." Ubisoft is now retrenching its strategy to focus on core franchises and live-service games by canceling another three unannounced projects on top of the four terminated in July 2022 and accelerating the depreciation of EUR 500 million in research and development next quarter. As a bonus, the often-delayed Skull and Bones was pushed back for the seventh time from its March 2023 launch date to later in fiscal 2024.

Ubisoft’s focus on developing franchises could backfire if any of its franchises fall out of favour with gamers. Success attracts imitators, and the company must constantly fend off competitive attacks from industry rivals while also trying to develop new intellectual property. Video games compete with TV, movies, televised sports, and other leisure activities. The video game space is highly competitive, with both competitors and new entrants spending to create new IP. Ubisoft has been aggressive in releasing new versions of Assassin’s Creed, and the near-annual release schedule could induce gamer fatigue and lead to lower sales. Neil Macker, senior equity analyst

Roblox

• Fair Value Estimate: $65.00

• Total Return YTD: 37.00%

Roblox operates an online video game platform that lets gamers create, develop, and monetise games for other players. The firm offers its developers a hybrid of a game engine, publishing platform, online hosting and services, marketplace with payment processing, and social network. Unlike a full-priced AAA title, there is no entry cost to try out Roblox or the vast majority of user-developed games. Thus, to drive booking growth and keep the Roblox model churning along, the new user must purchase and spend Robux, the platform’s tender.

Roblox operates in a highly competitive marketplace against firms with more financial and development resources. While Roblox’s platform is a unique offering, the firm still competes with video game publishers both to attract new users and to hold on to their current players as they grow older. A key driver to the firm’s long-term growth will be keeping younger users as they age into and out of their teen years, as over two thirds of users are under the age of 17 and around half are under 13 years old. Neil Macker, senior equity analyst

NetEase

• Fair Value Estimate: $139.00

• Total Return YTD: 23.14%

NetEase started as a Chinese internet portal in the late 1990s but has now become the second-largest mobile game company in the world. The firm owns one of the most well-known massively multiplayer franchises in China – Fantasy Westward Journey. Over the past decade, NetEase has capitalised on the industry shift toward mobile gaming and now focuses on developing innovative, high-quality, and long-cycle games with a mobile-first approach.

Over the past years, the firm has established iconic titles such as Onmyoji, Knives Out, and Identity V. Every year, the company publishes dozens of games across almost every genre and game play. In addition, NetEase is also collaborating with firms such as Blizzard, Marvel, and Microsoft to release games based on famous global intellectual property like Diablo, Harry Potter, and Lord of the Rings. Over the foreseeable future, we expect NetEase to continue to leverage its in-house research and development team and user data to develop next-generation games.

We think that NetEase exhibits high levels of risk, in line with most of the Chinese internet firms under our coverage. Online gamers’ interest can be unpredictable, switching costs are minimal and competition is intense. NetEase relies on gaming for 70% to 80% of revenue, and from 2006 to 2021, the segment’s revenue growth has ranged from a low of 2.1% in 2007 to a high of 87% in 2015 during these years. Success or failure in new game launches and legacy game maintenance and expansion packs could lead to significant fluctuations in the growth of gaming revenue and profits. Ivan Su, senior equity analyst

Take-Two Interactive Software

• Fair Value Estimate: $165.00

• Total Return YTD: 1.37%

Take-Two is one of the larger third-party video game publishers and owns one of the largest most well-known video game franchises in Grand Theft Auto. With the acquisition of Zynga, the company is now also one of the largest mobile game publishers. We believe the firm is well positioned not only to capitalize on the success of GTA but also to continue diversifying its revenue beyond its signature franchise. We expect Take-Two to continue to benefit from the high demand for consoles, the ongoing revitalization of PC gaming, and the growth of mobile gaming.

Take-Two has capitalised on the shift within the industry toward a bifurcated market consisting of major AAA blockbuster titles on one side and smaller independent games on the other. Take-Two generally focuses on the higher end, using its capital to fund the higher-budget blockbusters and its marketing advantage over independents in terms of both budget and established networks to support its titles. Over the past 10 years, the firm has established new franchises such as Borderlands while reinvigorating older ones like Xcom. We expect the company to continue to invest in new intellectual property and to fund its development via sequels and expanding its core franchises onto mobile platforms. The Zynga acquisition will speed up the process of creating mobile versions of the franchises. Neil Macker, senior equity analyst

Nintendo

• Fair Value Estimate: $12.58

• Total Return YTD: 1.66%

We believe Nintendo’s fans will increase as people are able to enjoy its characters on various occasions, and that the success of the Switch platform proves Nintendo can induce new fans to its ecosystem by leveraging its characters and preparing attractive game pipeline. Future challenges for the company will be: 1) whether the company can monetise its characters efficiently on the nonconsole business, 2) whether re-entry to the greater China market will succeed, and 3) how the company can adapt to the diffusion of the cloud gaming platform. We nevertheless believe the company’s ability to deliver fun games through its characters is intact.

Competition from other game platforms is a risk factor for Nintendo. However, we think the PlayStation 5 and Xbox Series X/S are designed for older players, as games on those consoles feature high-resolution graphics and rich audio content, targeting different segments. Mobile games may be direct competitors for the company’s products. To address this problem, Nintendo has decided to provide its IP to smartphones, which we think will help expand Nintendo’s user base, as more people will be able to use its content. Kazunori Ito, director

Activision Blizzard

• Fair Value Estimate: $92.00

• Total Return YTD: -6.49%

Activision Blizzard is one of the world’s largest third-party video game publishers and owns some of the largest and well-known video game franchises, including Call of Duty and World of Warcraft. We believe the firm is well placed to consolidate its leading position by developing compelling new versions of its existing franchises and by introducing new experiences, such as Overwatch. We expect Activision to continue to benefit from ongoing console demand, the ongoing revitalisation of PC gaming, and the growth in the mobile market via King.

Like its peers, the firm is focused on engaging users beyond the initial game sale via extending the monetisation window by expanding the use of multiplayer options and releasing downloadable content. Both methods encourage gamers to hold on to the original game longer than in previous generations and provide an income stream from consumers who purchase the game secondhand. Activision has used downloadable content and multiplayer to extend the life of multi-billion-dollar franchises such as Call of Duty, and we believe franchises like Hearthstone and Overwatch can also maintain long-term success. Neil Macker, senior equity analyst

.jpg)