Although July marks the start of a new proxy year, it’s not quite time for stewardship professionals to switch off for the summer just yet.

Tesla’s TSLA shareholder meeting on August 4 features votes on important environmental and social themes. These reflect many of the trends we saw across the US stock market in the 2022 proxy year, which we outlined in a recent research paper. The results may indicate whether those trends are likely to continue in 2023.

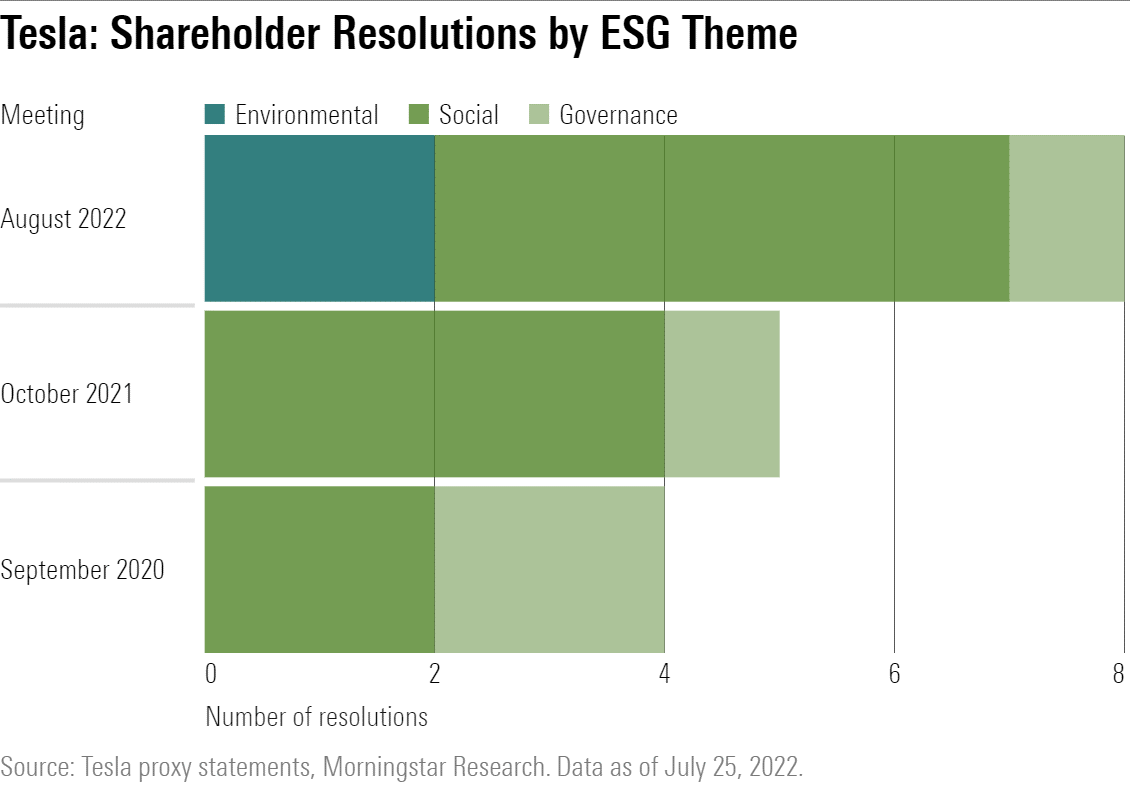

Our research highlighted a steep increase in the number of shareholder resolutions on environmental, social, and governance themes. Tesla’s 2022 shareholder meeting is no exception. The company’s proxy card this year features more resolutions filed by shareholders than by management. There are eight shareholder resolutions out of a total of 13, up from five in 2021 and four in 2020.

Tesla's proxy card for 2022 features eight shareholder resolutions, up from five in 2021 and four in 2020

Seven of those eight shareholder resolutions address environmental and social issues—with social issues being the main area of focus. This is a salient theme for Tesla following the company’s controversial ejection from the S&P 500 ESG Index earlier this year. Tesla’s removal from the index was due to a perceived lack of progress in tackling workforce issues reported within the company, such as discrimination and harassment, and harsh working conditions.

There are 13 resolutions on Tesla's 2022 proxy card: five management resolutions and eight shareholder resolutions

Social Becomes Central to ESG

Last year, before I joined Morningstar, I listened to an ESG analyst at a large global asset manager lament that social was "the forgotten middle child" of ESG. Now, this view seems almost outmoded, as it is accepted that social is central to ESG, and certainly not forgotten.

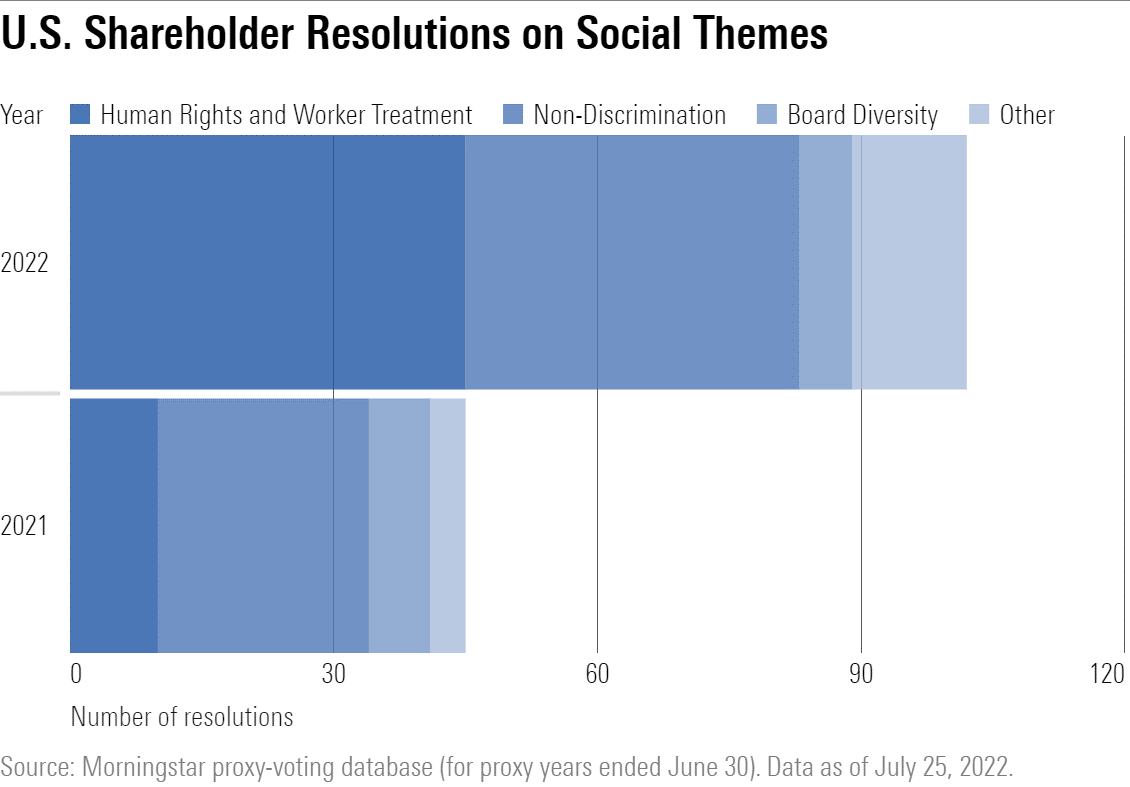

The number of shareholder resolutions covering social issues at US companies more than doubled in the 2022 proxy year compared with 2021. This increase was mostly attributable to a much higher volume of shareholder proposals on human rights, treatment of workers, and nondiscrimination themes (including resolutions addressing equal employment and pay disparity).

The average support level for these social resolutions retreated slightly from 31% in the 2021 proxy year to 27% in 2022. This reflects a similar fall in support for shareholder resolutions overall, as many asset managers push back on what they see as a higher volume of proposals that are unduly prescriptive or duplicate companies’ existing efforts.

There has been a steep increase in the volume of shareholder resolutions on social issues in the US in the 2022 proxy year according to Morningstar's proxy-voting data

At Tesla, Shareholders Target Social Themes

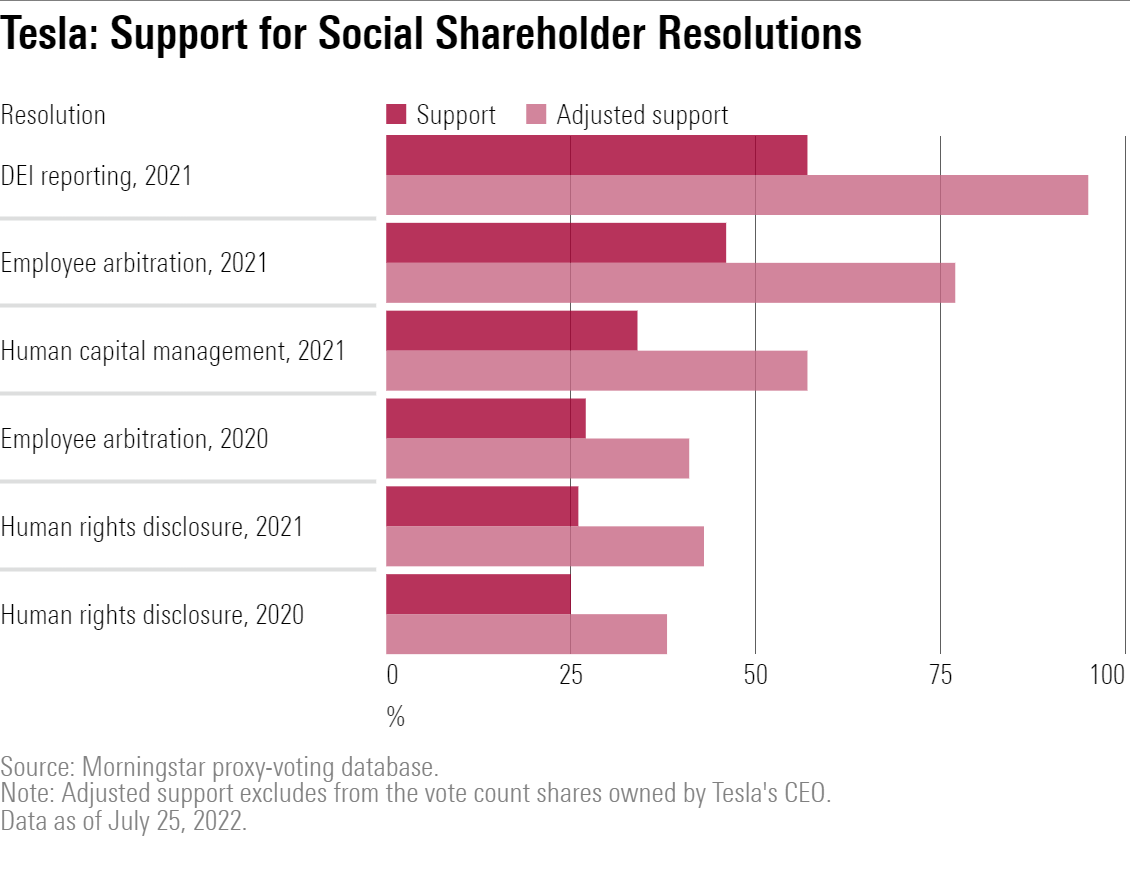

Six shareholder resolutions addressing social themes were filed at Tesla in the previous two years. Notably, all six gained at least 25% support. Last year’s proposal filed by Calvert Research and Management requesting annual reporting on diversity, equity and inclusion practices at the company actually gained majority support (57%). This means that 95% of independent voting shareholders supported it, assuming that CEO Elon Musk’s stake of over 20% in Tesla was voted against the proposal in line with the board’s recommendation.

Such strong support reflects the increasing focus that many of the very largest U.S. asset managers are placing on addressing DEI issues in their proxy voting policies, as identified in our recent research.

Shareholder resolutions on social issues at Tesla at its last two shareholder meetings were well supported by the company's independent shareholders, according to Morningstar's proxy voting data

There were consecutive resolutions in the last two years seeking improved disclosures about the impact of Tesla’s mandatory arbitration policy for employee sexual harassment and racial discrimination claims. Shareholder support for these resolutions increased considerably from 27% in 2020 to 46% in 2021.

The "big three" index investors Vanguard, BlackRock, and State Street are key to the overall support level. All three are top-five Tesla shareholders, together representing around 15% of its share capital.

The "Big Three" index asset managers—Vanguard, BlackRock, and State Street—have voted for social shareholder resolutions at Tesla in different ways in the past two years, according to Morningstar research

Interestingly, in 2021, BlackRock and State Street both reversed their decisions to oppose the mandatory arbitration resolution. BlackRock stated that it considers the proposal to be "in the best interests of shareholders" as Tesla "does not meet our expectations for disclosure of material social policies and/or risks."

The mandatory arbitration resolution returns to the Tesla proxy card for a third time this year. However, this time it focuses on racial discrimination, only following a change in the law prohibiting mandatory arbitration of workplace sexual harassment and assault claims.

It will be interesting to see whether managers’ increasing focus on DEI issues translates into majority shareholder support for this resolution this time around, particularly given that Musk is understood to have reduced his stake in Tesla to around 17% to fund his attempted takeover of Twitter TWTR.

Environment: Going Beyond Emissions

This year, two environment-related shareholder proposals appear on the Tesla proxy card: one on climate, one on water risk.

The climate proposal requests disclosure on "how Tesla’s climate-related lobbying and policy influence activities…align with the Paris Agreement’s goal to limit average global warming to 1.5 degrees Celsius, and how Tesla plans to mitigate risks presented by any misalignment."

This proposal illustrates how the thinking on climate disclosure by shareholders with a strong ESG focus has evolved beyond greenhouse gas emissions targets and reporting and has begun to encompass broader governance and public policy advocacy issues like board-level climate expertise and Paris-aligned climate lobbying.

For example, last year, 30% of shareholders withheld support for the election of James Murdoch, a Tesla director and audit committee member. BlackRock and State Street voted against Murdoch’s election, with BlackRock stating that Tesla’s disclosures on climate risk, scope 1 and scope 2 greenhouse gas emissions, and climate-related metrics and targets fell below their expectations. It remains to be seen whether similar dissatisfaction will surface in the votes for the re-election of two other directors this year.

The other environment-related shareholder resolution requests additional reporting on Tesla’s water risk exposure and mitigation practices. As our research notes, this kind of reporting is also requested by several ESG-conscious asset managers who are placing greater focus on other environmental themes alongside climate, including deforestation, species loss, and water risks.

Tesla Says ‘No’—Will Shareholders Agree?

Tesla’s board opposes all eight shareholder resolutions, believing that its existing governance around proxy access is appropriate, and its actions in addressing DEI, discrimination and harassment, human rights and labor rights, and climate change are all sound.

With asset managers applying greater scrutiny to shareholder resolutions and more often disclosing the rationale behind their votes, managers’ decisions on the shareholder resolutions at Tesla will be a useful indication of what to expect in the 2023 proxy year.

Lindsey Stewart CFA is director of investment stewardship at Morningstar

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/347BSP2KJNBCLKVD7DGXSFLDLU.jpg)