As The BoE Makes its Move, Beware The Currency Effect

As The BoE Makes its Move, Beware The Currency Effect

Despite the central bank’s rate hikes, pound sterling has lost around 13% against the US...

The US Economy is Cooling, and That's Good News

The US Economy is Cooling, and That's Good News

A soft landing is in sight. But could the economic slowdown go too far?

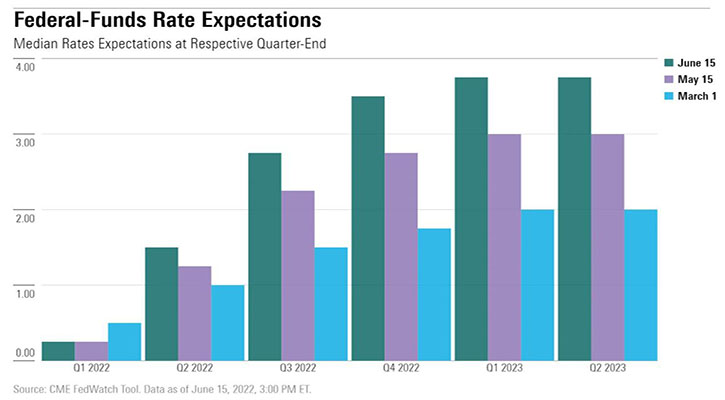

When Will the Fed Start Cutting Interest Rates?

When Will the Fed Start Cutting Interest Rates?

Our latest economic forecast for US interest rates, inflation, and GDP growth

-

Are FTSE Mining Companies Cheap Right Now?

Are FTSE Mining Companies Cheap Right Now?

Mining companies are operating in a challenging environment but could now be the time to top up o...

-

Advice for George Osborne and Stock Market Regrets

Advice for George Osborne and Stock Market Regrets

THE WEEK: Morningstar columnist Rodney Hobson provides two pieces of advice to George Osborne, an...

-

How to Find Solid Dividend-Paying Stocks

How to Find Solid Dividend-Paying Stocks

Businesses that have competitive advantages within their industry are good candidates for dividen...

-

10 Top-Performing Funds in the UK

10 Top-Performing Funds in the UK

Morningstar reveals the top 10 best performers over the last five years

-

Fund Research: Europe’s Shining Stars

Fund Research: Europe’s Shining Stars

Morningstar OBSR reveals the top funds for investors seeking exposure to European equities

-

NatWest Shares Up as Profits Beat Expectations

NatWest Shares Up as Profits Beat Expectations

The bank also announced a deal with Metro Bank, raised its guidance, and increased its dividends

-

After Earnings, Is Netflix Stock a Buy, a Sell, or Fairly Valued?

After Earnings, Is Netflix Stock a Buy, a Sell, or Fairly Valued?

With revenue growth, increased operating margins, but a high valuation, here’s what we think of N...

-

Going into Earnings, is Apple Stock a Buy, Sell, or Hold?

Going into Earnings, is Apple Stock a Buy, Sell, or Hold?

We'll be watching iPhone revenue, gross margins, and services growth when Apple reports its earni...

-

Unilever Earnings: Growth in a Challenging Market

Unilever Earnings: Growth in a Challenging Market

Despite growth, Morningstar's Fair Value Estimate for the consumer goods giant stock is unchanged

-

AstraZeneca Earnings: Steady Outlook but Growth Could Slow

AstraZeneca Earnings: Steady Outlook but Growth Could Slow

Morningstar analysts think the UK's biggest company has a well-positioned broad drug portfolio wh...