The pound is hovering around $1.22 on Monday, the lowest point since the start of the pandemic, after the dollar strengthened in response to rising US interest rates and the pressure from economic uncertainty in the UK and Europe increased.

This matters for British investors holding non-pound-denominated assets in their portfolios. Leaving their foreign currency exposures unhedged could lead to an implicit – and in most cases unintended – bet. Most of the time, currency movements and returns are positively correlated, so currency risk usually adds to volatility.

How it Works

The return of foreign securities consists of the asset’s market performance and the performance of the currency in which it’s priced. If the foreign currency appreciates against the local one, the effect will be positive, while a stronger pound would have a negative effect on overall performance of the investment.

For instance, the Morningstar US Market Index dropped as much as 14.3% for the year-to-date in US dollars, meanwhile it lost “only” 9.7% in pounds, thanks to the favourable exchange rate for British investors.

Inversely, the Morningstar Eurozone Index shed 10.2% in euros since the beginning of the year, while its version in pound sterling lost 10.6% over the same period. As a result of the same dynamic, the Morningstar Japan Index shed 8% in pounds, while the benchmark’s performance in Japanese yen is -0.6%. The value of the pound against the Japanese yen rose about 7.5% so far in 2022.

In this case, Japanese investors holding pound-denominated assets have benefited from the strength of the British currency – the yen-denominated Morningstar UK Index gained only 8.7% between January 1 and June 9, while the return in pounds is 0.7%. Meanwhile, British investors holding Japanese assets would have been wise to hedge against exchange rate risk with an instrument that gives this option.

What’s next for Cable?

Concern about the war in Ukraine, energy scarcity and the impact of Covid-19 lockdowns in China on global economic growth has driven investors toward safe-haven assets like the US dollar. The greenback’s strength in recent months has been supported by the Federal Reserve’s cycle of rate hikes and some weakness in the British economy, which looks to be slowing and facing a potential recession.

Recent key economic data from the UK has been showing signs of decline: the S&P Global flash Composite Purchasing Managers’ Index (PMI), which is a monthly gauge of the services and manufacturing industries, fell to 53.1 in May, remaining well below the 58.2 from the previous month to mark the lowest growth rate in 15 months, as UK private sector firms recorded a slowdown in growth of business activity and new orders, pressured by rising inflation. Looking forward, business confidence slipped to 17-month lows.

The Bank of England has not been sitting on its hands, as it has hiked rates at four consecutive meetings since December to take the base interest rate to a 13-year high. However, that has been insufficient to offset the headwinds weighing on the pound. Now it looks like the market is betting the BoE will deliver a historical half-point interest rate hike by September, but – again – that may not necessarily turn the tide.

“The market is very bearish on sterling,” said Sam Lynton-Brown, head of developed markets strategy at BNP Paribas, in an interview with the Financial Times. “Domestic political uncertainty (Boris Johnson’s “no-confidence” vote) hasn’t been a big driver of the currency. So even if it alleviates, you shouldn’t expect the pound to recover. We still think it can weaken further.”

At this time, therefore, it does not seem to be on the agenda for British investors to hedge the currency risk of their foreign investments. In the future, though, a strengthening pound might suggests some prudent hedging strategies to avoid the risk of significant pound appreciation or foreign currency depreciation.

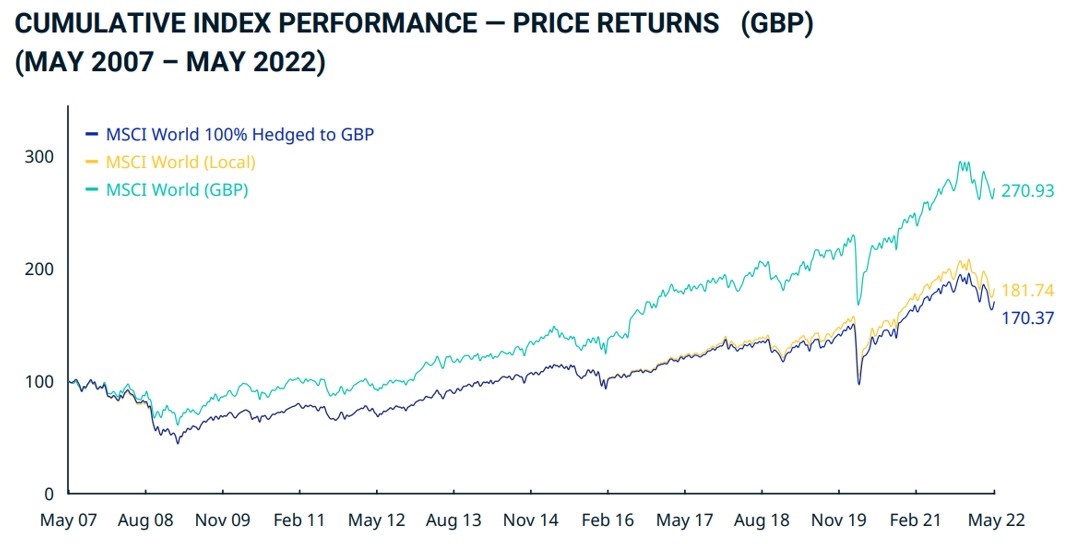

Hedging comes at a cost

As the chart below shows, the return of currency-hedged foreign assets will fall slightly short of those asset’s local-currency returns. That’s partly because currency-hedged funds charge higher fees. Additionally, most such funds use forward contracts to hedge currency risk. These contracts – which simply lock in a future exchange rate– are subject to the “rolling effect”.

What’s that? Futures contracts must periodically be replaced at maturity, and this generates the “roll yield”. Such yield – which can be positive or negative – is determined by the difference between the price of the rolling near-term expiring contract and the price of the new forward contract with expiration date further in the future.

Source: MSCI

Is it worth it?

The primary benefit of hedging is a significant reduction in currency risk. But this benefit comes with trade-offs like higher fees and a limited menu of choices.

“The first item to check when deciding to hedge is the expected relationship between an asset’s local returns and foreign exchange rates”, Daniel Sotiroff, Senior Manager Research Analyst at Morningstar said. “The expected correlation between these two should be positive to justify any hedging activity, because a positive correlation causes currency risk to increase the volatility of assets listed in foreign currencies. Generally, this relationship has been positive in the past and should continue to be positive in the future, but exceptions like the Japanese stock market can occur.”

Investors should also be mindful of their investment horizon. “Returns attributable to foreign exchange rates can ebb and flow over time and add to an investment’s volatility, but they tend to have a muted impact on long-term rates of return”, explains Sotiroff. “Meanwhile, the impact of exchange rates on returns can be quite dramatic over short periods of time.”