This week we asked our Twitter followers to choose between stocks that have been caught up in the Omicrom market turmoil, and they’ve chosen oil company BP (BP.) by a small margin over lockdown stalwart Amazon (AMZN). Oil firms have been in sharp focus since the pandemic started, because of the volatility of oil prices and the impact this has had on the once generous dividend policies. ESG investing has come to the fore too, meaning shareholders are piling pressure on oil company boards to commit to carbon reduction targets. Energy prices are also feeding into the current inflation scare, with the price of petrol and natural gas soaring.

Last year, crude slumped and has since rallied, and has recently tumbled amid fears over the new coronavirus variant. Oil’s recent wobble has reminded the world of the fragility of the re-opening trade, the narrative that energy demand will surge as the economy comes out of last year’s deep freeze, with people starting to use transport again in all its fuel-hungry forms. Brent crude was at aound $25 a barrel in 2020’s nadir but has roared back to $85 in 2021, and now stands just above $70 after the latest Omicrom-related sell-off. While some investment bank analysts have taken this weakness as a trigger for price downgrades, others have reiterated their bullish forecasts, with sticking with a $150 a barrel forecast for 2022. Morningstar oil analysts have recently published a report on the energy market and predicted stronger demand and continuing support for prices. Higher oil prices are bad news for motorists but positive for those who invest for income using oil company shares. BP chief executive Bernard Looney recently described oil companies as “cash machines” in a bullish market for crude. Whether this scenario makes it harder for fund companies to break the oil dividend habit is a matter of fierce debate among ESG investors. Can shareholders have their cake and eat it with oil companies, taking the income while also supporting firms embracing and backing renewable energy with hard cash? Shell’s chief executive Ben Van Beurden, defending calls to split the company up, says that oil’s (potential) last hurrah can fund green energy, and the legacy and future assets are interconnected.

Morningstar’s Allen Good says that BP’s plans for the energy transition are among the most bold among oil majors. “Its strategy ranks as the most aggressive move away from hydrocarbons among its peers with plans to reduce production by 25% by 2025 and 40% by 2030 and refining capacity by 30% by 2040 through divestment … It has the most ambitious growth plans of its peers for renewable generation by targeting capacity of 20 GW in 2025 and 50 GW in 2030 from 2.5 GW currently, but it also plans to double its LNG equity portfolio,” Good says. BP has teamed up with Lightsource for solar projects and Equinor for offshore wind, for example, and investing in hydrogen facilities in the north east of England. The Deepwater Horizon disaster, which serves as case study for future generations of students on the “E” of ESG risk, has largely been put behind the company – although it has cost the company billions in the last decade.

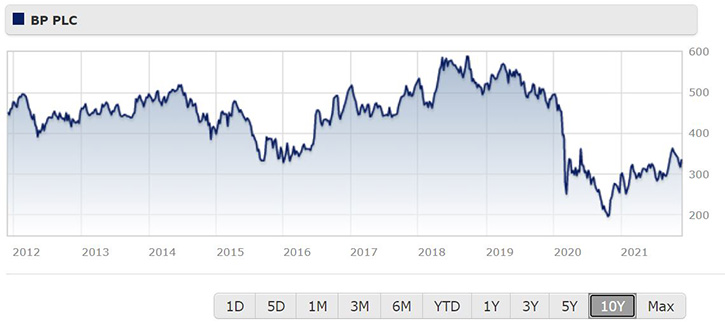

Let’s look in detail at BP’s numbers. Morningstar estimates BP’s fair value as 380p per share, and shares are currently around 340p per share, having risen a chunky 35% so far this year. Still, over the long term, the shares have struggled to get back above the pre-Deepwater Horizon levels of 600p, despite a strong run in 2018. Shares currently yield just over 4.5% - Shell yields around 3.6% - and so far investors have received three payments this year, of just under 4p a quarter, with another dividend to be paid before the year end. The company is also engaging in share buybacks, and we’ve explained why FTSE 100 firms are doing a lot of that this year here. Existing investments can break even with oil at $50 a barrel and new ones at $40 a barrel, according to Morningstar’s Good. Third quarter net profit was $3.3 billion, above forecasts and the $2.8 billion in Q2 – and the $100 million in the lockdown-affected third quarter of 2020. Morningstar analysts think there’s a danger that BP will make the green transition too early, especially given the second wind the fossil fuel industry is having this year, and perhaps next if fears over new Covid variants recede. BP may be sacrificing some profitability if it divests legacy assets too soon, Good adds.