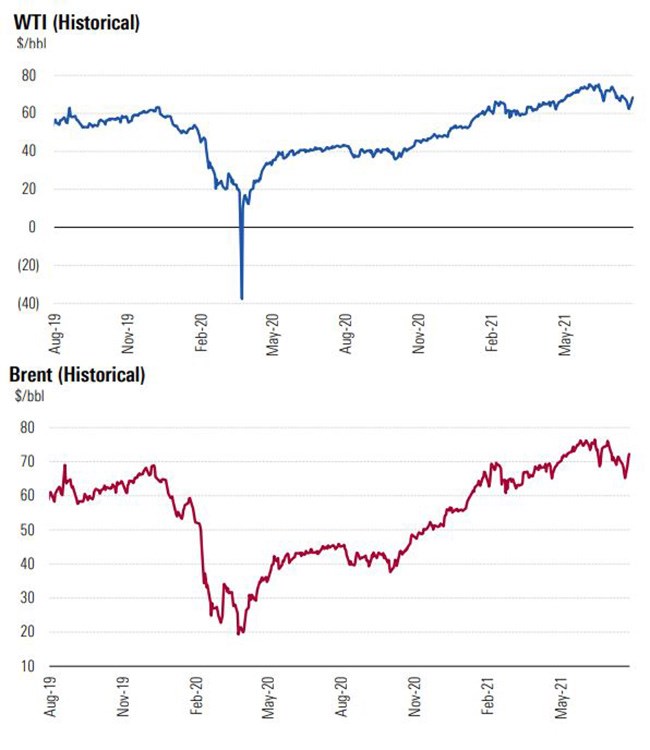

Last month, we sounded the alarm about the potential for oversupply and lower prices due to robust private operator US production growth. This month, we've changed course and now expect tight supply and high prices into 2022. In this case, the changing fact is the continued underperformance of OPEC+ production compared with its stated targets, which combined with an on-track demand recovery will lead to inventory draws the remainder of the year and require additional US production in 2022 to balance the market. But for this to happen, prices will need to remain high. Prices could remain high into 2023 as well if Iran volumes do not return as we expect, requiring even more US volume growth. Markets have already begun to recognise the tightening supply, sending oil prices and energy equities higher, but some opportunity remains.

The delta wave of Covid-19 has been on the downslope globally since early September. Supply chain issues may have pulled down consensus global GDP estimates down slightly for 2021, but the impact to oil demand is marginal as long as driving and flying continue to recover. Meanwhile, oil use for power generation is growing in the face of high natural gas prices, providing incremental demand. As a result, there's no change to our outlook for global crude demand. We currently project global consumption to reach 96.2 mmb/d and 100.4 mmb/d, respectively, in 2021 and 2022. The latter estimate exceeds the prepandemic consumption level of 100.2 mmb/d (2019).

But on the supply side, our forecasts have changed. August was the fourth straight month in which OPEC failed to meet its quota, and this month the deficit widened to almost 700 mb/d. In the third quarter, nine of the 10 OPEC countries with quotas underproduced. The struggle suggests chronic underinvestment and is likely to persist through 2022. That means the oil markets are considerably tighter than we previously thought, which changes our opinion about the trajectory of near-term prices.

We previously wrote that the planned OPEC increases left little room for US growth and that lower prices could be needed to stymie an unnecessary advance in US rig activity. That no longer looks accurate. After moderating our OPEC outlook, we now think global inventories will end the year below the normal range, which is why prices are spiking. We still expect inventories to normalise in 2022, but less growth from OPEC leaves more room for US expansion. So, oil prices seem likely to remain above midcycle levels in the next six to 12 months to encourage incremental drilling.

OPEC Struggles to Hike Output

OPEC increased its production by just over 100 mb/d in August, far below its planned raise of 400 mb/d. This marks the fourth consecutive month of underproduction, and the shortfall has been steadily widening. And despite Brent oil hitting a three-year high of over $80 a barrel and increased pressure from consumers, the cartel has no plans to accelerate the unwinding of its curtailments. During its October 4 meeting, the OPEC+ partnership reaffirmed its plan to gradually ratchet volumes (adding 400 mb/d until December 2022). However, we now suspect this is an acquiescence of necessity rather than a strategic choice, as many of the group's participants have been unable to meet their quotas. These difficulties are very likely to persist through the end of the year and into 2022.

Nigeria and Angola are facing the steepest challenges. The former's output dropped by more than 160 mb/d from the month prior to 1.27 mmb/d. Nigeria has now missed its target by more than 100 mb/d for four straight months. Meanwhile, Angolan production remained relatively stagnant this month at about 1.1 mmb/d but still well below its OPEC production quota. The country has not met its quota since July 2020, and output has been in freefall since September that same year.

The crucial question is whether the deficit created by underperforming countries can be extenuated or altogether nullified by OPEC’s more stable producers. While Saudi Arabia, Iraq, and Kuwait all have ongoing projects aimed at increasing their production capacities, we believe that at least in the near term, the cartel will continue to fall short of its 400 mb/d increase commitments, especially as monthly shortfalls compound. It’s worth noting that the production target that OPEC (and partners) will likely fail to reach is an exaggerated one.

The cartel bases its cuts on October 2018 production, somewhat arbitrarily. This is a marketing gimmick; it enabled OPEC+ to claim it was cutting 9.7 mmb/d at the outset of the pandemic. Since prepandemic production was more than 3 mmb/d lower than this high-water mark from October 2018, the "real" cuts were closer to 6 mmb/d. The cartel's recent rhetoric indicates that it aims to restore production to the higher benchmark, a feat we think it will struggle to accomplish. But we do think it can reach the lower benchmark. Our 2022 estimate for the combined output of the 10 OPEC countries with quotas is 25.7 mmb/d, and by year-end we expect over 27 mmb/d from these same countries. That compares with early 2020 output of only 25.1 mmb/d. So the struggles we have highlighted are merely limiting the share that the cartel can capture rather than preventing it from fully reversing its cuts.

Iranian Exports Needed for Balance

Our model shows the oil markets will remain supply-constrained through 2022, given our skepticism about OPEC's ability to fully deliver on its ambitious production goals. In prior cycles, US producers may have been willing to close the gap, but the industry's steadfast commitment to capital discipline will restrict its growth and prevent it from acting as a vital release valve. But we anticipate relief in 2023. This relief is underpinned by one critical assumption. We believe the US and Iran can eventually reach an agreement on nuclear proliferation, unlocking 1.5-2 mmb/d of latent supply. This is a substantial component of our supply forecast, without which the world will probably remain short on oil. Negotiations between the US and Iran over Trump-era sanctions have been hitting an impasse in recent months. But a solution makes sense for all parties. Lifting the sanctions and opening up Iranian exports would deliver a strong revenue boost for Iran, while delivering a much-needed political win for the Biden White House, which has thus far failed to persuade Tehran to help revive the 2015 nuclear deal.

A deal would also offer an easy way out of a tricky situation for the US President, who has been calling on other OPEC members – unsuccessfully – to raise production and ease pressure on US oil and gasoline prices, while simultaneously proposing tightening restrictions on domestic producers to promote his environmental agenda and appease the liberal wing of his party. This gives rise to two distinct, binary scenarios. In the first, Iranian exports eventually recover to normal levels, closing the supply gap and balancing the market as long as US producers remain true to their word and target low-single-digit growth. The timing is extremely uncertain, of course, but a resolution before 2023 seems unlikely.

In the alternative scenario, the US remains deadlocked with Iran and sanctions are left in place indefinitely, preventing the necessary resumption of Iranian exports. In the latter case, undersupply becomes chronic and an alternative supply source must be found. That means significantly more rigs in the US shale patch, expansion projects for other OPEC members, or new development projects elsewhere. As we see little impetus for such investments yet, it appears that producers are content to wait and see what happens with Iran and enjoy higher prices in the meantime.

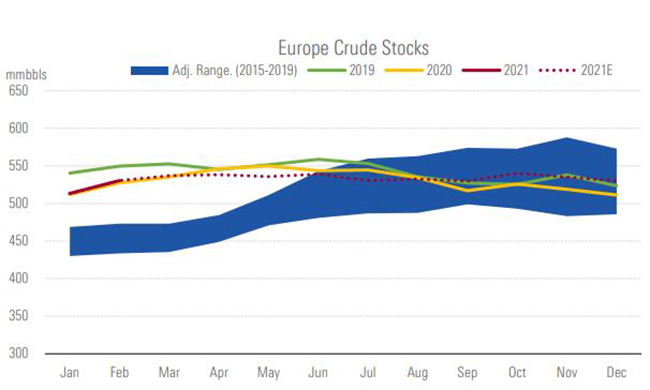

This report was produced by Morningstar analysts David Meats, Allen Good, Marloes Spanjersberg and Justin Pan. A full version is available on Morningstar Direct. Europe Crude Stock data is from Capital Economics (as at end of August 2021).