Each week we ask our Twitter followers to pick a stock for us to write about. This week’s theme has been US companies that are reporting results in the coming weeks, and there are plenty of these as Q3 earnings seasons cranks up. But instead of going for this biggest names, we’ve gone for the less obvious companies. Our Twitter followers have gone for conglomerate Honeywell (HON), a North Carolina based company that makes a range of products for domestic and industrial uses and has a long history. These includue home thermostats, cockpit instrumentation for planes and lighting and heating controls for buildings.

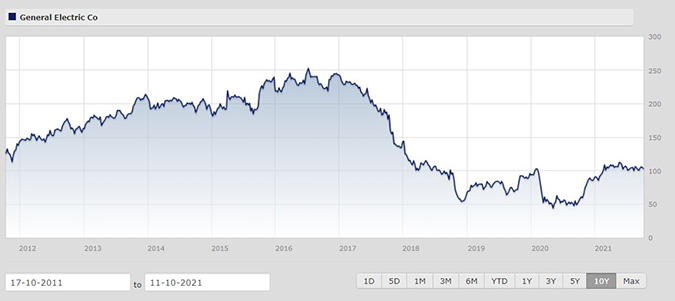

One of our other Twitter choices this week was General Electric (GE), which during the imperial Jack Welch era bought Honeywell for more than $20 billion in 2000 before EU competition authorities intervened. As things often turn out, Honeywell is now much bigger than General Electric, with a market cap of $150 billion versus GE’s $112 billion. Morningstar analysts rate Honeywell highly, awarding the company a wide economic moat. Joshua Aguilar says: “Honeywell is one of the strongest multi-industry firms in operation today, which we think the market rightly recognises by awarding the firm a conglomerate premium. We predicate our thesis mostly on: a) the commercial aerospace recovery; b) continued strength in defence; and c) an increasingly automated world in mission critical end-markets like warehousing, utilities, and oil and gas.”

Software is central to maintaining this competitive advantage and generating excess returns in the future, Aguilar explains. “The key to Honeywell carving a wide moat, in our view, is the firm’s increasing ability to leverage its software technology across its massive industrial installed base. This software technology is integrated into both mission-critical operations, as in cockpit control during commercial aircraft flights, and in customer operations, through diverse offerings like warehouse automation in factories or connected solutions in buildings. In our opinion, aerospace is Honeywell’s widest-moat business, both from a qualitative installed base perspective, and from a quantitative returns-based perspective.”

Shares are rated as 3 stars, with a fair value of $211 versus a current market price of $218 (the fair value was increased after the last quarterly earnings, from $203 to $211 per share). As the price graph shows, shares have risen four fold in 10 years, not including dividends. While the yield of 1.73% isn’t too punchy, the company has managed to increase its dividend 11 times over the last decade (the equivalent list of UK companies is here).

Honeywell reports third quarter results on October 22 and investors will be looking closely at the recovery in the commercial aerospace division, which took a unsurprising hit in 2020. The last set of results showed that sales growth in this area were up by double digits, because of an increase in the amount of hours flown by aircraft using Honeywell products. Our analysts think this market will perform best in the latter half of the financial year. “We were mostly expecting stronger signs of a recovery in the commercial aero market in the back half of the year, and still maintain the view that commercial aero will lap 2019 results in 2024,” says Aguilar. Consumer demand for commercial flights is growing, especially having been thwarted by lockdowns last year and restrictions into 2021, according to the International Air Transport Association (IATA). Honeywell management are also confident this positive trend can be maintained. “We agree with the management’s view that there is significant pent-up demand in commercial travel,” Aguilar adds.

Our analysts also rate Honeywell’s management and governance. More than four years into Darius Adamczyk’s tenure as president and chief executive, the company has one of the strongest balance sheets under Morningstar US stock coverage. Aguilar says: “We assign Honeywell’s management an exemplary capital allocation rating based on its sound balance sheet, exceptional investments, and appropriate shareholder distributions. The firm has one of the strongest balance sheets in our coverage, with a net debt to EBITDA level that typically runs below 1 times. Second, we commend management for making promising growth capital expenditures investments at the height of the pandemic to take share from competitors. We expect the firm will earn significant economic profit from these investments. Finally, we like management's disciplined M&A process and its unwillingness to overpay for growth.”

Adamczyk’s career also has an element of the American Dream about it: arriving in the US aged 11 from Poland, not speaking English, he graduated with an MBA from Harvard and started at General Electric as an electrical engineer. While investors would have been happy with the share price surge since he took over, life hasn’t all been plain sailing for Adamcyk, with activist investor Third Point pressuring him to spin off Honeywell’s aerospace division. Aguilar says that the CEO handled this pressure well. “Activists often call for spin-offs and pressure under the rationale that near-term volatility weighs down multiples, and ultimately, shareholder returns. While we’ve agreed with Third Point in the past and acknowledge spin-offs can sometimes serve as positive catalysts to help close the gap between price and value, we think it's management's job to figure out over the long term whether business declines are secular or cyclical, if they ultimately fit in with a conglomerate’s strategic goals, and if keeping or separating a business ultimately adds or detracts to returns on capital,” Aguilar adds.