Great companies are companies that you want to hold forever, because of their intrinsic positive qualities and their ability to deliver high and growing returns, which in turn will drive share price higher over the long run.

But how do you recognise a great company?

There are many factors to consider. You will have to rely on financials (provided the numbers reported are truthful), but you could also use other non-financial and qualitative indicators.

In this article, we will mostly focus on financials. Remember, though, you can find ESG ratings information on the Sustainalytics website, and look for qualitative factors by reading the financial materials public companies provide (examples include annual reports and proxy statements). You can also read books on strategy, such as the work by Jim Collins, author of the seminal Good to Great.

Now, let’s consider the financial aspects that make a company ‘great’. To do that, start by asking questions, like:

- How strong is its balance sheet?

- How much cash is generated by the company’s activities?

- How competent and decent is the management of the company both in terms of capital allocation, and in their alignment of interests with shareholders?

The answers to these questions will help you determine how ‘great’ a company is. Let’s look at these characteristics in some detail. We’ll also illustrate these points with an example, ASML Holdings (ASML). This company is one of the world largest makers of semiconductor manufacturing equipment, and earns a ‘Wide’ economic moat – meaning it can fend off competition for years to come.

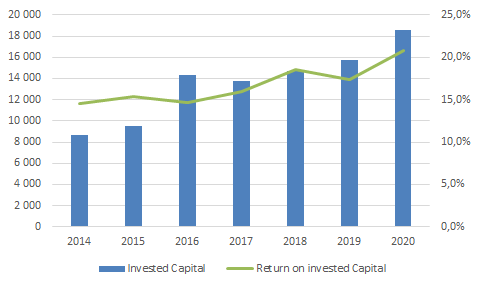

Return on Capital (ROIC)

ASML’s ROIC

Source: Morningstar Direct

Return on capital is a percentage number of how much money you get for 1$ invested in a business. Warren Buffett explained in the 1979 Letter to Berkshire Hathaway shareholders:

“The primary test of managerial economic performance is the achievement of a high earnings rate on equity capital employed (without undue leverage, accounting gimmickry, etc.) and not the achievement of consistent gains in earnings per share. In our view, many businesses would be better understood by their shareholder owners, as well as the general public, if managements and financial analysts modified the primary emphasis they place upon earnings per share, and upon yearly changes in that figure.”

For an in-depth look at return on capital, you can refer to Michael Mauboussin and Dan Callahan 2014 paper, which is pretty comprehensive. Most companies publish some information that can help you assess it, but you can also check the finance page of almost any public company on Morningstar website.

In the key ratios section of the Morningstar website, you will find historical information about the gross margin, the operating margin and the return on equity of the company, and see that all those metrics are elevated and growing, which tends to show you’re dealing with a highly profitable company.

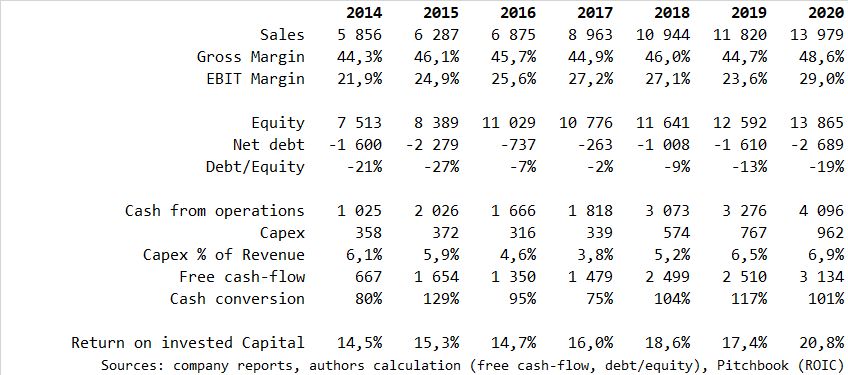

A Strong Balance Sheet

ASML’s Balance Sheet

Source: Morningstar Data

A strong balance sheet is generally characterized by low debt, strong liquidity and solvency (i.e. the ability to meets its financial obligations). Solvency is usually assessed by looking at Debt-to-Equity, Debt-to-Capital, Debt to EBITDA ratios. Liquidity is assessed by looking at ratios such as current ratio, metrics related to working capital (the cash needed to run the business during one year).

For instance, ASML’s equity is close to US$14 bn and represented close to 50% of its balance sheet at the end of year 2020. Debt to equity ratio stands out at 33% if you only count long-term financial debt, but is actually negative once cash is taken into account.

Its liquidity ratios are also strong with current ratio of 2.4 in 2020 compared with 2.6 in 2016.

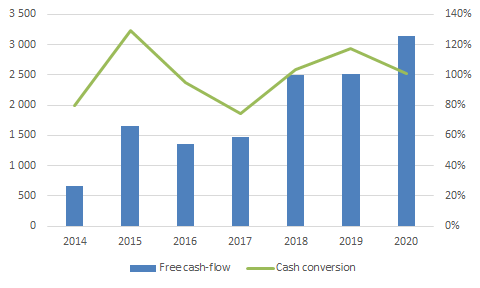

Solid Cash Generation

ASML’s Free Cash Flow

Source: Morningstar Direct

Cash is probably the ultimate metric for any company. It’s the lifeline that permits its operations to run, its investments to be financed, and its obligations to be met. It’s also the basic indicator that helps estimate the intrinsic value of a company.

Several popular metrics allow assessing how much cash a company generates but we will focus on 2 in particular: cash conversion and free cash-flow.

Cash conversion measures the ability of a corporation to turn earnings into cash, and is calculated as the ratio between Cash-flow from operations (from the cash-flow statement) and operating profit or Earnings Before Interest and Tax (EBIT) in the income statement.

Why is that important? From an accounting perspective, all expenses in the income statement are not necessarily cash outflows. For instance, when a company buys an equipment (say a computer), it will recognize a depreciation every year for 2 or 3 years to account for the economic benefit this computer brings before needing a replacement. Depreciation charges are not cash per se, and contribute mostly to the discrepancy that can arise between earnings and cash-flows. That’s the reason a high level of cash conversion shows a high ability to generate cash from the operations of a firm.

Free cash-flow is also very important. It’s simply the cash available to the owners of the firm after its capital expenditures have been financed. It’s the cash left to the discretion of its management, to be used in M&A, share buybacks, dividend or debt repayment. For ASML, both cash conversion and free cash-flow have been improving over the last 5 years.

Good Management Teams

In his book “Good to Great”, Jim Collins writes that great companies have “Level 5 Leadership”. Those leaders have a number of characteristics, such as humility and “professional will”. In fact, to Collins, who’s going to define and execute a strategy might be more important than the strategy itself.

Warren Buffett and Charlie Munger often say that the best companies they wanted to be partners with are companies run by honest, decent and competent managers. Most of the time, those managers have built the company they run, but you can also find managers that have been groomed internally for a long period of time, who are truly passionate about their industry and will dedicate to increase the value of their company.

Another key characteristic of these outstanding managers is their ability to focus on capital allocation rather than day-to-day management. Berkshire Hathaway is probably exemplary in this regard. The holding company, which employs only 25 people, controls about 75 medium-to-large sized businesses.

Buffett and Munger admit they rarely talk to the management of those firms, because they are considered competent in their field and responsible for their decisions.

It's not always easy to see how competent and decent a manager is. But by reading interviews, biographies and by looking at the way their compensation is structured, you can find glimpses of the qualities that CEOs have, and may be able to gauge if they are in line with your expectations.

How Morningstar Can Help

Morningstar has focused its equity research process on the economic moat (originally from Warren Buffett) and the capital allocation decisions of managers. Those analytical tools allow investors to assess exactly how long a company can withstand competition and generate high return on capital. Those synthetic indicators can help guide you through thousands of stocks available to you in the equity markets.

A good place to start your research into a company (and its stock price) could be to look at the company’s competitive advantage, through Morningstar’s Economic Moat Rating, its current price, through the Morningstar Star Rating, and the Morningstar Fair Value Estimate, and the risk it carries, through the Morningstar Risk Rating.

Good luck!