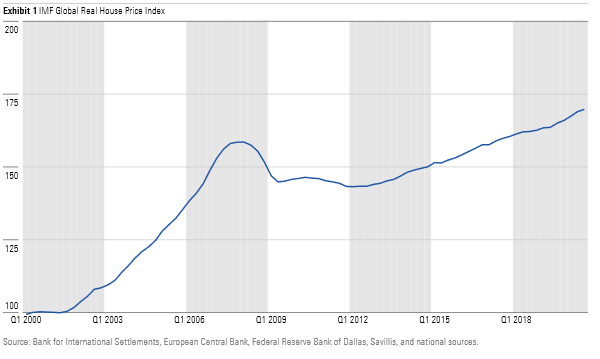

The age-old question of whether to invest in real assets (like a buy-to-let property) is more relevant now than ever, seeing as globally, housing prices are growing at a rapid pace.

The rise in housing prices puts a wrench in the seemingly simple calculation of determining whether to invest in property, because the perceived prospects of capital gains can seem more enticing today when compared to just a decade ago.

That said, many things have not changed, including the pros and cons of investing in an income property versus stocks.

Pros of Owning an Income Property:

1. You own a real asset, one that you can see/feel/touch, and have some degree of control over the physical observable quality of that property through further investments (of time and/or money)

2. Assuming you have longstanding occupancy in that property, it will provide a steady supplementary income stream that will help you offset lending and upkeep costs.

3. Over a longer time frame, the property itself will likely rise in value (hopefully in excess of inflation), providing you with capital gains alongside a steady income stream from tenants.

4. With historically low interest rates, the costs of borrowing to invest in an income property have dropped (but will eventually rise again).

Cons of Owning an Income Property:

1. An buy-to-let property is a significant investment into a single asset class: real estate. Most research firms categorise 11 sectors of the economy, with real estate representing one. Keep in mind whether you can still effectively diversify your portfolio (inclusive of the property) to take advantage of the only “free lunch” in investing.

2.The financial cost of maintaining an income property can be significant, both in terms of property upkeep and in time to service your tenant(s). It would be worthwhile considering the value of hiring a property manager if this is a service available in the area, while considering those costs versus maintaining the property on your own.

3. Real assets like property are generally illiquid, meaning that you cannot sell the property quickly in secondary markets unlike financial assets like stocks. Here, consideration of investment time horizon is important. If you require the money invested back within a short time frame, it’s likely that an income property is not your best bet.

4. For many investors, purchasing a property will require borrowing capital from a financial institution. Though mortgages are generally considered ‘good’ debt, remember that borrowing to invest is a form of leverage, which increases risk. If for some explicable reason property prices fall, your change in financial position can be dramatic. Consequently, if rental rates fall, your ability to service debt will also be affected. Since interest rates are at all-time lows, it would not be unexpected for these to rise once again, thereby increasing your cost of debt in the future.

5. Depending on which jurisdiction you live in, tax treatment of secondary properties may not provide the same tax benefits as a primary residence. In the UK, the sale of investment properties is subject to capital gains tax, while those owning more than one property face higher stamp duty bills when buying.

Finding a Happy Medium

There is no argument that an allocation to real estate within a larger portfolio is a reasonable bet. Indeed, real estate values are generally less volatile than stocks, and can offer diversification benefits. Investors would be served well to consider investments in real estate investment trusts (REITs) which will still give you exposure to real estate prices and access to cashflows generated by tenanted properties, while maintaining the liquidity of a stock. Moreover, REIT investors have the choice of investing in residential or commercial REITs, allowing further choice in the types of ‘tenants’ occupying your slice of property. Real estate exposure is also available through funds and ETFs that invest in a pool of REITs.

Investors are cautioned here that mortgage funds (which may sound like real estate exposure) are fundamentally very different from REITs, since they invest in pools of debt instruments (mortgages) as opposed to equity within a REIT structure.

Questions to Ask Before Buying an Investment Property

After this investment, will a significant portion of my money be invested in a single asset? If so, perhaps consider REITs instead, that can occupy a more reasonable portion of your overall asset allocation.

Will I be able to make monthly mortgage payments if my cost to borrow (i.e. mortgage rate) rises in the future? If the maths works out now, consider recalculating using a mortgage rate that is 2-3% higher than currently posted rates as a safety buffer.

Will I require my investment dollars back in the short term? If the answer is yes, perhaps an income property is not the way to go since it may be difficult to exit the position in a timely manner.

This article does not constitute financial advice. It is always recommended to speak with an adviser or financial professional before investing.