We asked our Twitter followers to choose a UK bank as stock of the week and they’ve gone for Lloyds Banking Group (LLOY), whose shares are on a strong run this year after collapsing in 2020 as banks got clobbered during the pandemic sell-off.

Lloyds and NatWest (formerly Royal Bank of Scotland) were the two UK banks bailed out by the Government during the global financial crisis of 2008. In 2017, the state sold its last remaining stake in Lloyds in 2017 but it’s still a 60% owner in NatWest. Lloyds owns high street bank brands Halifax, Bank of Scotland and pension provider Scottish Widows.

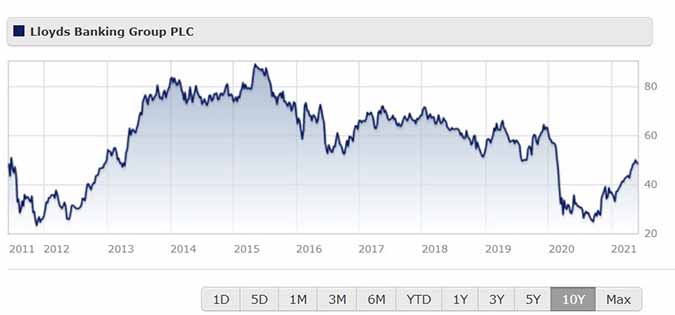

At around 43p, shares in Lloyds have a long way to go before reclaiming their pre-financial crisis levels around 300p. As one of the most bought UK stocks on retail investment platforms, some shareholders are betting that it can, at some point, regain its glory days before the banking crash. For now, Morningstar analyst Niklas Klammer assigns the stock a fair value of 62p per share, 30% above the current price.

As long-standing shareholders rediscovered last year, as a UK-focused bank company shares is for better or worse seen as a lightning rod for the UK economy. Shares took a hit after the Brexit vote in 2016 as investors feared the decision would plunge the UK into recession, and during the depths of the market crisis in 2020, hit lows last seen during the 2008-2009 crash. High PPI compensation costs, which hace cost Lloyds billions, have also dragged on investor sentiment. Customers of banks and building societies had until August 2019 to lodge a complaint for mis-sold payment protection insurance, and the industry is hoping this draws a line in the sand.

Lloyds Share Price Over 10 Years

Lloyds shares have been buoyed by Britain’s lead on the vaccine rollout, which has helped spur forecasts for the best growth since the 1940s. According to the latest Morningstar Market Barometer, Lloyds is the fourth-best performing large-value stock in the Morningstar UK index with a 38% gain in the year to date and nearly 70% over one year.

Why do Morningstar analysts assign a narrow moat to Lloyds, when fellow financial crisis survivor Natwest has none? Klammer says the group’s restructuring programme has stripped out billions in costs and reduced its exposure to more risky assets, and has managed to increase margins even as interest rates have slumped (rates near zero make it much harder for UK banks to make profits on loans, credit cards and mortgages). “Since its massive restructuring, which started in 2011, the bank has emerged as a low-risk domestic retail and commercial … Today, Lloyds operates one of the strongest retail franchises in the United Kingdom,” he says.

To help diversify away from its sizeable mortgage book – it’s one of the biggest home loan lenders in the UK – Lloyds has expanded its financial planning services and targeted loans to small and medium-sized enterprises, which are primed to lead Britain out of the coronavirus slump. Overall, despite the obvious risks of being exposed to the fragile UK economy, high regulation and lingering “antibank sentiment” in the UK, the UK banking sector is still a profitable space to be in, says Klammer. He describes the current Big Five banks as a “comfortable oligopoly”, where Lloyds can carve out a niche because of its low-cost set-up and because of the high “switching costs” in the UK banking scene.

Until last year’s intervention by regulators was a favourite among dividend investors, yielding around 5%. Shareholders are eagerly awaiting developments on that front when the group releases results in July - the company has a holding position in our list of top FTSE dividends and is likely to re-enter the top 10 when the dividend is restored.

ESG-wise, Lloyds rates as a “Leader” in corporate governance, according to Morningstar-owned ratings agency Sustainalytics. But its score is marked down because of “legacy business issues” relating to among others, fraud uncovered at its HBOS division. Still, the company was the first FTSE 100 firm to imposed gender diversity targets in 2014, and the outgoing chief executive Antonio Horta-Osorio, has been praised for his openness in taking time off for stress in late 2011.

.jpg)