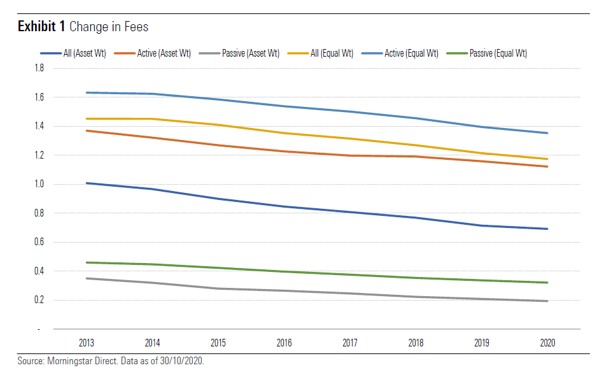

European investors are paying lower expenses, on average, than ever before. According to a Morningstar study, for a group of equity and fixed-income Morningstar Categories during the period from 2013-20, the average fee paid by investors, represented by the asset-weighted average ongoing charge, was 0.69% in October 2020, a 31% decline from 2013.

What's Driving Fees Down?

There are several factors that have driven fees lower:

Investors are increasingly aware of the importance of minimizsing investment costs, which has led them to favour Exchange traded funds (ETFs) and index funds.

Intensifying competition among asset managers has resulted in many cutting fees to vie for market share.

The move toward fee-based models of charging for financial advice.

Why do Retail Investors Pay More?

However, there is room for more improvement. The 2020 ESMA analysis of the performance and costs of Ucits investments over time clearly shows that the costs paid by retail investors are significantly higher than those paid by institutional investors, leading to lower net returns for this category of investors.

For example, an investment of €10,000 in a hypothetical retail portfolio, composed of equity, fixed income and mixed funds, would grow to a value of around €21,800 after 10 years (2010-2019). When costs are taken into account, the value declines to €18,600. Around €3,200 in costs are paid by the investor. If we consider the same type of investment undertaken by an institutional investor, the value after 10 years would be €22,744 in gross terms and €20,743 in net terms, implying costs of €2,000. A retail investor would therefore pay around €1,000 more than an institutional investor.

Why Fees Matter

Cost are a key factor for investors. Research has demonstrated time and again that fees are a reliable predictor of future returns. Low-cost funds generally have greater odds of surviving and outperforming their more-expensive peers. This is because fees compound over time and eat into returns. Expenses are also one of the easiest factors for mutual fund investors to control. You can’t be certain how a fund is going to perform, but you can know exactly how much you’re paying for it.

Low fees help a fund’s Morningstar Analyst Rating, because they confer an advantage right off the bat over more-expensive counterparts. As a reminder, the enhanced Morningstar Analyst Rating for funds introduced late in 2019, amplified the fee assessment. The Morningstar Manager Research team subtract a fund’s expenses from their estimate of how much value it can add before fees. If there’s nothing left for investors, then they won’t recommend the fund. This approach makes the fee assessment as important as People, Process, and Parent combined. They also tailor ratings to each share class by taking its specific fees into account. Thus, costlier share classes see lower ratings in some situations.

What Else?

Of course, fees aren’t the only investment consideration. People, Process and Parent are important as well.

People

The overall quality of a strategy’s investment team is significant to a strategy’s ability to deliver superior performance relative to its benchmark and/or peers.

Process

Morningstar analysts look for strategies with a performance objective and investment process (for both security selection and portfolio construction) that is sensible, clearly defined, and repeatable. It must also be implemented effectively. In addition, the portfolio should be constructed in a manner that is consistent with the investment process and performance objective.

Parent

The asset manager and its management set the tone for key elements like capacity management, risk management, recruitment and retention of talent, and firmwide policies, such as incentive pay, that drive or impede the alignment of the firms’ interests with those of fund investors. The Morningstar research team prefers firms that have a culture of stewardship and put investors first to those that are too heavily weighted to salesmanship.

Performance Before and After Fees

Past performance isn’t necessarily predictive of future results. When considering past performance, investors would do better to focus on long term return and risk patterns. Moreover, as expenses are one of the better predictors of future outperformance, investors should weight them in the assessment.

Several Morningstar studies show that the typical active manager can beat the benchmark, but that he struggles to do it after fees. We don’t know if a top performer fund in the past years, will be a top performer in the future, but we know the cost we pay for it and this tell us a lot about the odds of being successful in the future.