The trials and tribulations of stock markets are such that in observing short-term returns, there has been a fairly remarkable comeback. Over 12 months to the end of March 2021, global equities are up 39%, and while the UK has lagged with a 26.7% rise over this period, more-recent performance has started to paint a different picture.

If you think back to last year's volatility, it was airlines, oil, banks, energy, and cyclical parts of the market that felt the brunt of the downturn, while technology and disruption quickly started to appear as winners in the Covid-19 pandemic. As an investor, remaining calm was key, and if you were able to allocate capital, the “Covid trade” worked.

The following days and months saw sharp rallies in this part of the market, but that’s not been as clear-cut over the past six months. Indeed, with the market being forward-looking and a potential recovery in sight, plus trough valuations in cyclical areas, there has been significant outperformance from these stocks.

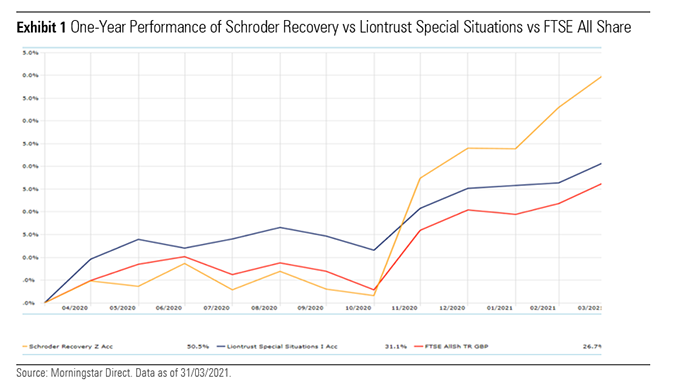

We can start comparing performance over one year and the past six months to see this in action, picking out funds that have biases to each side of this coin. For example, in UK equities we can compare Liontrust Special Situations (with a Morningstar Analyst Rating of Bronze) with Silver-rated Schroder Recovery. The Liontrust team seeks to identify firms with intellectual property, strong distribution channels, and significant recurring business. With around two thirds of the portfolio in small- and mid-caps, there is also a leaning to growth companies. Schroder Recovery follows a process founded on value investing and has high overweights in energy and banks.

The above chart shows that the most recent six months or so has helped propel the performance of Schroder Recovery, resulting in pretty much doubling the market returns over the 12-month period.

In the first quarter of 2020, however, which included the deep market sell-off in March, the fund fell 33.9%, compared with 25.1% for the market and 21.1% for Liontrust Special Situations.

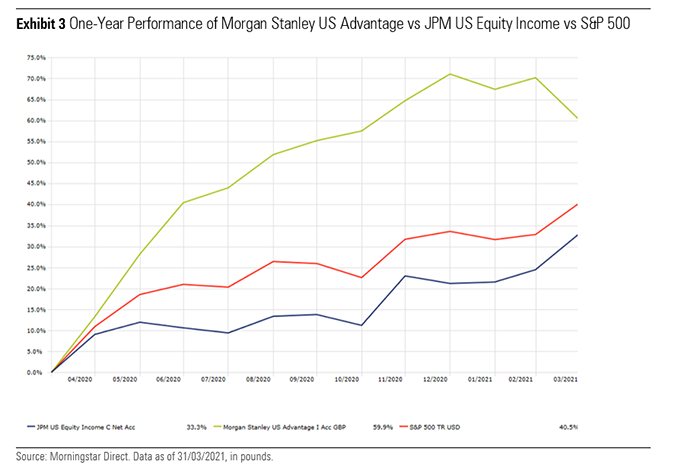

Turning to US equities, the high technology weighting has been a boon to help drive performance and the sell-off was much shallower than in the UK. Here we compare US Equity Income and Morgan Stanley US Advantage.

Gold-rated JPM US Equity Income pays close attention to valuation, and in terms of style has a value leaning. On the other hand, Silver-rated Morgan Stanley US Advantage is out-and-out growth. It focuses on established companies that are growing with enduring competitive advantages, such as solid brands, scale, network effects, or advantaged technology or intellectual property. Top holdings include the likes of Twitter (TWTR), Amazon.com (AMZN), Shopify (SHOP), Twilio (TWLO), and Spotify (SPOT). The extent to which these sorts of names motored as part of the “Covid winners” has resulted in a handsome outperformance over the past 12 months. The S&P 500 is used as a reference point in Exhibit 3 to capture the whole market, but the fund was still ahead of its growth comparator.

We would expect JPM US Equity Income to underperform the main market across this timeframe given its value bias, but what is perhaps not immediately obvious in the graph, is the extent to which the situation flipped in the latter part of 2020 and into this year.

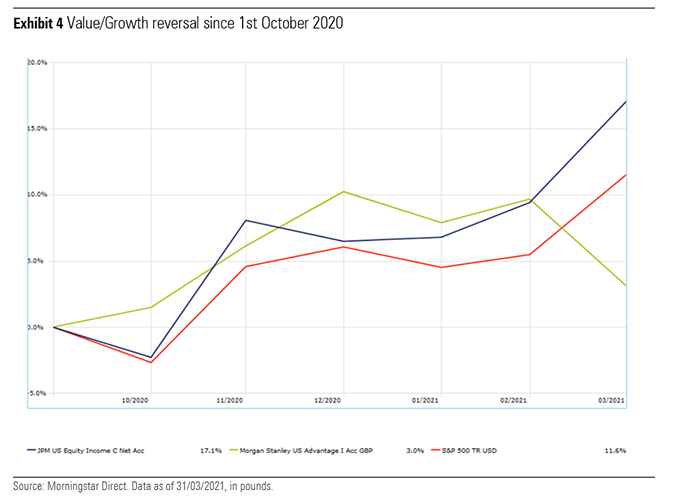

More broadly, it’s not uncommon to observe funds that were top-decile over the past year, ending up in the bottom decile during the past six months. When turning to fund flows, as markets started to pick up in April and May 2020, it was evident that investors were backing previous winners whose structural tailwinds over the last five and 10 years were still in play--namely quality growth, technology, and disruption.

But being a contrarian would have also reaped rewards, and stronger ones at that, so far in 2021. Popular themes have been underperforming, and with inflation or even a cyclical uptick on the horizon, unloved areas have started to come back to the fore. While this doesn’t mean investors should necessarily overstretch in that direction, hanging on solely to the darlings of the past decade might not be prudent as part of a balanced portfolio.