“Diversification, diversification, diversification” is the mantra we must repeat every time we make an investment decision. In other words: don't put all your eggs in one basket (or portfolio, in this case). But what if we have more than one investment basket? The risk, in the investment world, is that being overweight in assets can unbalance the investment plan we have made.

Firstly, what is asset allocation? It is the mix of different asset classes (equities, bonds, etc) in your portfolio. Historically a simple method of 60% equities and 40% has sufficed for many investors, but others like to have exposure to additional assets such as gold, property and renewable energy.

The wisdom behind such diversification is largely about reducing risk. Asset classes tend to behave differently in different conditions. In good economic conditions, for example, equities might do well while bonds may struggle. In this situation, someone invested purely in bonds will be at risk of capital losses whereas a more diversified investor will be less exposed. The same applies to regions, sectors and investments trends.

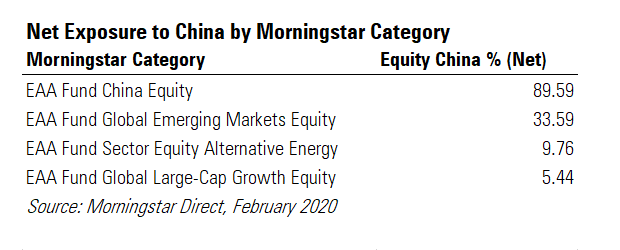

Let's take, for example and for simplicity's sake, three Morningstar categories that, at least on paper, should guarantee sufficient diversification: Global Emerging Markets Equity, Global Large Cap Growth Equity and Sector Equity Alternative Energy.

Imagine we want to add an Equity China fund into the mix to ride the post-Covid recovery of the Asian country. If, within the different categories, we choose the wrong fund, we risk finding ourselves excessively biased towards Chinese equities.

Beware of Revenues

When we choose a category that gives good diversification, we must consider another element: revenue exposure. In other words, where companies in the portfolio generate most of their earnings. The FTSE 100 is a good example of this, with around three-quarters of the stock market's earnings coming from outside the UK.

Imagine we have the usual China category. We want to be diversified at the sector level and we move across different Morningstar categories: Sector Equity Consumer Goods & Services, Sector Equity Technology, Sector Equity Water. For geographic diversification we choose the Global Large Cap Value Equity category. In this case, depending on the fund we choose and where the fund's constituents make their revenues, we still could have a strong bias towards China.

“As companies continue to expand their global footprint, traditional means of measuring geographic diversification are increasingly insufficient”, says Ben Johnson, director of global exchange-traded fund research for Morningstar. Measuring global diversification along dimensions of fundamental exposures - such as revenue - can paint a more complete picture of funds' degree of diversification.

“Small-cap stocks tend to sell more in their home markets, while large caps make more sales away from home” Johnson says. Favouring small-caps may then provide more direct exposure to local market fundamentals.

Some sectors are globetrotters, while others are homebodies. Financials, utilities, and real estate stocks typically have local asset bases and clientele and will tend to be most sensitive to fluctuations in local interest rates. Technology and materials stocks have a more global reach.

Looking at your portfolio through the lens of regional revenue exposure might show that even the most home-biased portfolios are better diversified than they first appear.

Your Portfolio To-Do List

What does all this mean for your own portfolio? Here are some things to consider:

- Consider the objectives of your portfolio. This will inform how diversified you need to be and how much risk you can afford to take. With a long-time horizon, a retirement savings pot can afford to be more aggressive than a short-term rainy day fund which can't afford to endure capital losses. This means your asset allocation mix will be differ between the two pots.

- Assess your equity and bond exposure: “Your broad asset-class exposure will be the key determinant of how your portfolio behaves. But your positioning within each asset class also deserves a closer look”, says Christine Benz, director of personal finance at Morningstar.

- Understand your portfolio. Asset allocation usually breaks down into strategic and tactical. Strategic positions are designed for the long term. Tactical calls are more short term in nature, usually to take advantage of changing economic or market conditions.

- Consider a core and satellite approach. Choose core and satellite. Core funds form the heart of your investment portfolio and are the main building block around which to construct satellites. Core funds are solid performers that deliver regardless of stock market conditions. Satellites are the additional positions you can use to build on your core and help to strengthen returns. These may be more volatile options, perhaps in riskier or niche areas.