Dividend investors, like so many others, experienced 2020 as an annus horribilis. The pandemic-driven economic downturn prompted a raft of companies to cut or suspend planned payouts to shareholders.

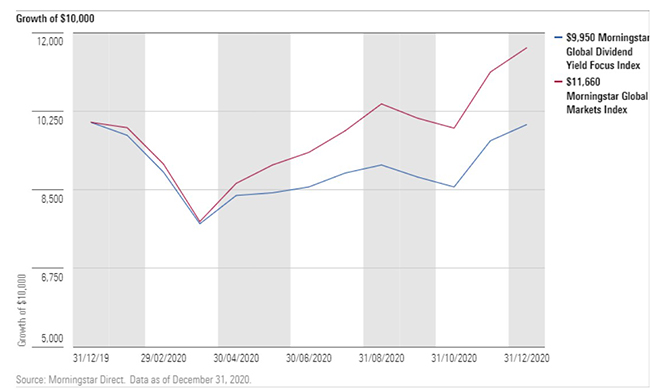

While the Morningstar Global Markets Index showed equities across developed and developing markets advancing 16% in US dollar terms in 2020, the Morningstar Global Dividend Yield Focus Index declined half a percentage point for the year. Dividend payers underperformed during the first quarter’s painful bear market then lagged when stocks bounced back.

But in November, dividend-payers mounted a comeback. The Morningstar Global Dividend Yield Focus Index gained nearly 10% between November 8 and the year’s end, in line with the broad market.

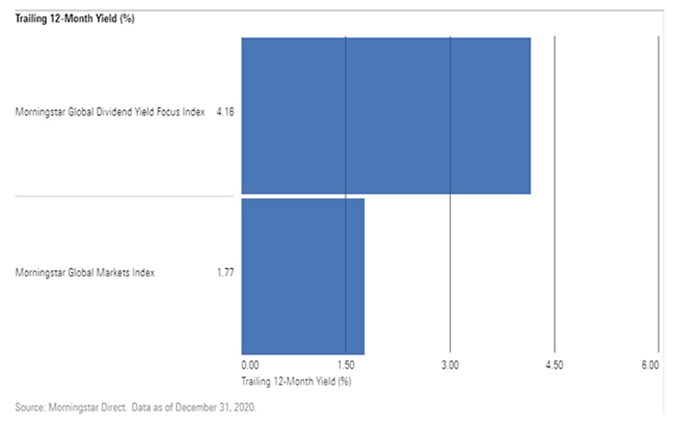

The dividend index has also yielded more than 4% over the past year. That more than doubled the yield for the global equity benchmark and towers over the income paid by most developed market government bonds these days.

Dividend-paying stocks still have a lot of catching up to do. But a market rotation to value stocks is good news for equity income investors. Meanwhile, the long-term case for dividend-paying stocks remains solid.

Why Dividends Were Caught in the Value Meltdown

Dividend-paying stocks tend to cluster toward the value side of the equity market. Companies in slower-growing sectors like consumer defensive, utilities, energy, and financial services, are likelier to pay out cash to shareholders than in faster growing areas such as technology. The Morningstar Global Dividend Yield Focus Index lands in the large-value segment of the Morningstar Style Box, where most equity income strategies sit.

That value bias was a huge problem for dividend payers for the first 10 months of 2020. The pandemic-driven downturn hit many value-leaning sectors hard. Consumer-oriented companies plummeted. Energy stocks suffered from falling demand and a price war among oil producers. Financials fell due to low interest rates and loan losses. Even utilities stocks, which had been prized in recent years for their rich yields, retreated in anticipation of lower electricity use by industrial and commercial customers. Unsurprisingly, dividend cutters clustered in oil and gas, consumer-related areas, and anything related to travel.

Meanwhile, technology companies benefited from work-from-home, learn-from-home, shop-from-home trends. In 2020, the market value of semiconductor maker Nvidia surpassed that of Nestle. The gulf between growth stocks and value stocks came to resemble the heights of the dot-com bubble of 1999.

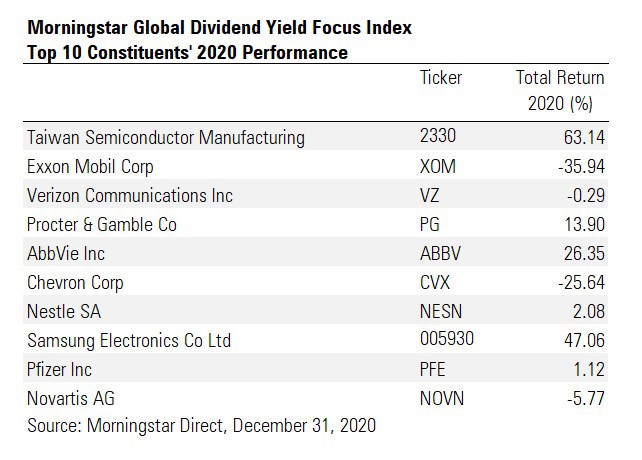

The Morningstar Global Dividend Yield Focus Index suffered for most of 2020 both for what it held and what it didn’t. Constituents like Exxon, Shell, HSBC, and BASF struggled mightily. Meanwhile, not including Apple, Amazon, and Tencent held it back relative to the global equity market.

Then came November. Promising vaccine results raised hopes for an end to the pandemic. The market saw the US election outcome as benign. Expectations of economic recovery lifted many beaten-down sectors. Dividend stocks soared as the value side of the stock market recovered. The Morningstar Global Dividend Yield Focus Index was boosted by soaring energy and bank stocks, vaccine maker Pfizer, and Asian technology leaders Samsung Electronics and Taiwan Semiconductor.

What Happens Next for Dividends?

We don't yet know whether or not the dividend renaissance will continues. From a valuation perspective, the market seems to be offering more upside within dividend-paying value sectors than on the growth side of the market. As 2021 begins, Morningstar Equity Research sees the most attractively valued sector as energy and the most overvalued as technology. Economic recovery would be good news for economically sensitive areas, where many dividend payers ply their trade. Low interest rates are likely to continue to push many income investors into equities.

Meanwhile, the long-term case for dividend payers remains strong. Not only does a significant portion of the long-term total return from equities come from reinvested dividends and dividend growth, but dividend payers have posted a strong track record relative to non-payers and the overall market. Companies that return cash to shareholders tend to be solid businesses. Committing to a regular payout instills discipline.

But dividend payers should be approached selectively. The market’s highest yielders are often troubled companies that turn out to be dividend traps. Investors who blindly chase yield can end up sacrificing returns. Dividends aren’t guaranteed and their sustainability must be always be gauged. The Morningstar Global Dividend Yield Focus Index, for example, focuses on high-yielders but screens them for quality and financial health.

.jpg)