The end of a year is a natural time to reflect on your investment portfolio and perhaps make a few changes for the year ahead. So how should equity income investors position for 2021?

After a volatile year, which saw a raft of dividend cuts, picking the best income options has never seemed so difficult. But we know from Morningstar research that companies with a solid business model have proved able to constantly increase their pay outs over the years.

The Morningstar Economic Moat is a good indicator of such businesses. Morningstar analysts pay high attention to how companies are positioned within the competitive environment and assign them an economic moat (wide or narrow) to those that demonstrate a business model so solid that can generate returns in excess of their cost of capital in the next give or 10 years.

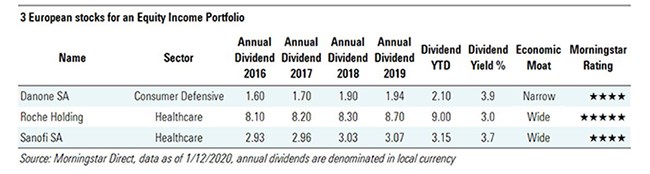

Here we have found three stocks with a very disciplined dividend policy and which have increased their dividend for at least the past five years. The stocks all have an economic moat and are currently trading at a discount compared to the fair value as estimated by Morningstar. The last point goes in the direction of not incurring in a capital loss and not falling into a dividend trap.

Danone

Danone (BN) shares are down a hefty 25% since year-to-date in euro terms, and are now trading at a 20% discount compared to their fair value of €64. The French company has business divisions in dairy, plant-based foods and specialised nutrition. Shares in the firm fell further in November when it announced plans to cut 2,000 jobs in a bid to make cost savings of €1 billion.

But in addition to the potential capital gains the stock offers, it also has a dividend yield above 3% (based on current market prices). Morningstar analysts assign to Danone a narrow economic moat and approve the management's decision to reduce operating costs.

"We think Danone commands a narrow moat, supported by its entrenched position in the supply chain, pricing power in its specialised nutrition business and a cost advantage”, says Ioannis Pontikis, Morningstar equity analyst. “The group announced a new cost-savings plan (€1 billion by 2023), with the majority expected to be delivered by the end of 2022, and it expects to translate this into a margin improvement."

Roche

Roche Holding (RO) is down about 1% year to date and is now trading at a 30% discount compared to the fair value estimate of 417 Swiss francs. Some investors may find this surprising given that the race for a Covid-19 vaccine has put the healthcare sector very much in vogue this year. The Swiss healthcare company has a wide economic moat, assigned because of its robust portfolio of drugs and a strong positio in the oncology and multiple sclerosis segments, in which the company has a great pricing power.

Morningstar equity sector director Damien Conover adds: "Thanks to strong information sharing with Genentech, Roche will be able to gain a significant market share also in the biologic drugs industry.” He praises the firm's excellent financial strength - in recent years it has managed to reduce its debt, and analysts expect this trend to continue in the future. "Over the next five we forecast 10% bottom-line compound annual growth and a payout ratio of around 50%," says Conover.

Sanofi

French pharma giant Sanofi (SAN) has seen its stock price slide 2.6% so far in 2020 and it is rated a four-star stock by Morningstar analysts, indicating that it is trading below its fair value estimate.

But the stock may be a solid option for income-seekers as it has consistently paid a dividend over the past five years, even during the recent market turmoil. Based on its current share price, the stock yields a tidy 3.7%.

Sanofi's wide line-up of branded drugs and vaccines and robust pipeline create strong cash flows earns it a wide economic moat. However, analysts point out that over the long-term, increasing branded and a deteriorating pricing environment will likely lead to continued sales declines for some of the group's key products like Lantus, an insulin treatment for diabetics.

Conover forecasts five-year average annual revenue growth rate of 3%, largely driven by steady gains with consumer products and vaccines along with new product launches offsetting deteriorating pricing for the company's top drug Lantus, and a margin improvement thanks to a careful cost-cutting.