Owners of commercial property like offices, bars and shops will have dismayed by the return of lockdown measures in November and the latest national lockdown introduced at the start of this year.

Some commercial property funds had begun to re-open in the autumn after a summer saw some workers return to the office and the retail outlets began to open again following the first lockdown. Despite the rollout of vaccines to tackle Covid-19, the sector still faces many serious challenges.

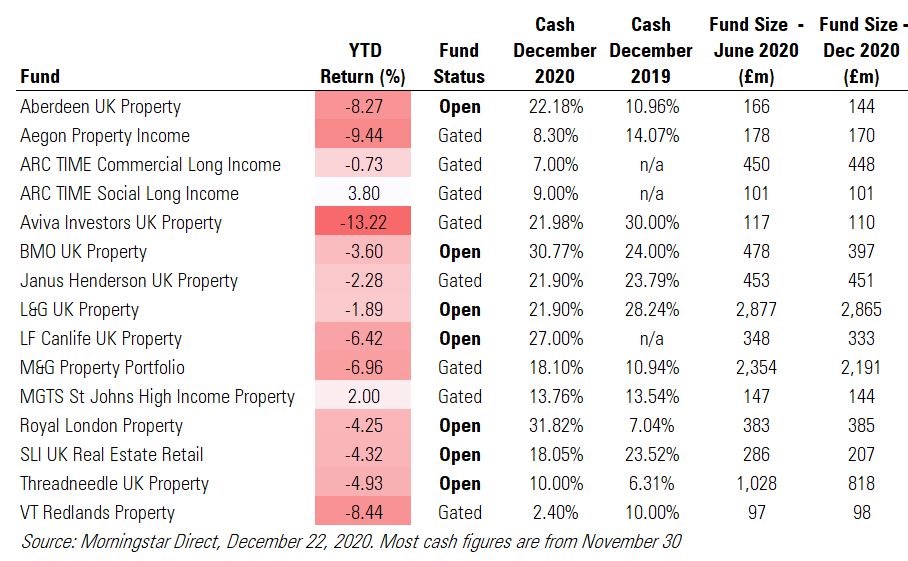

Most open-ended property funds gated in March 2020, M&G Property Portfolio has been closed since December 2019 and just a handful have re-opened since: Threadneedle on September 17, Royal London on September 30, LF Canlife on October 8, and Legal & General (the sector’s largest with nearly £3 billion of assets under management) on October 13. BMO UK Property is the most recent to re-open, on December 14. Janus Henderson said its UK Property fund could re-open in the first quarter of this year.

Mediocre Performance

Performance-wise, most open-ended property funds were in negative territory for 2020 as a whole, which is unsurprising given the disruption to the sector’s business model and the overall market conditions. The worst performer in the year to December 22 was Aviva Investors UK Property, with a loss of 13%, and the best performer is ARC TIME Social Long Income, the second smallest fund in the sector, with a gain of 3.8%.

While these funds don’t benchmark against the FTSE, it’s worth noting that despite the stock market's November rally, the FTSE 100 was still off 15% at this point, so these fund performance figures don’t look too catastrophic in comparison. Indeed, some of the worst-performing funds rated by Morningstar were down 20% or more in 2020 after a punishing year for value, equity income and special situations funds.

At this point, a return to pre-Covid office life in UK looks unlikely (Morningstar analyst Preston Caldwell has looked in detail at this topic), but no one can accurately predict how 2021 will pan out. And property funds don’t just hold offices and retail, so holdings in logistics and warehouses – which have facilitated lockdown deliveries and the Christmas parcel extravaganza – have thrived in recent months. One of the better performing funds of the year, Arc Time Commercial Long Income, has a 20% portfolio weighting towards logistics and only 2.5% regional weighting towards London.

The Question of Cash

A year ago, we wrote about property funds’ cash levels, and asked if they were holding too much cash. The pandemic year has shifted the dynamic on what is an appropriate buffer to have, and it’s worth comparing the levels year on year. We have comparable figures for 12 out of 15 of the funds and the picture is mixed: many cash levels have increased and some significantly (Aberdeen, Royal London, BMO, M&G, Threadneedle) and these are funds that have re-opened this year to investors. The lowest cash level is VT Redlands with 2.40% and the highest is Royal London with nearly 32%. Some nine out of 15 funds have a cash position above 18%.

The managers of Aegon Property Income, which remains gated with a cash level of 8.3%, said in their latest fund update that the decision to re-open the fund to investors depends on liquidity: “It is our intention to lift the funds’ suspension when we are satisfied that the fund has sufficient liquidity. The portfolio is currently holding a cash position below our target liquidity level and therefore disposals are in progress to raise the cash position to an acceptable level.”

A consultation by the Financial Conduct Authority into property funds closed in November. In August, the regulator proposed a solution to the “liquidity mismatch” that is inherent in open-ended property funds; the buildings owned by these funds cannot be offloaded as easily as shares and valuing these assets becomes more problematic at times of stress. Currently, property funds must provide daily pricing to investors and allow them to buy and sell whenever they like, but under the proposals investors could have to give 180 days’ notice to buy or sell units.

Are Investors Bailing Out?

With most funds gated for much of the year, fund flows in the direct property UK category have remained stable in recent months, says Morningstar analyst Bhavik Parekh. The point of gating a fund is to prevent a “rush for the exits” where managers have to sell assets to meet redemption requests. Parekh notes that the re-opening of some funds has seen immediate outflows. For example, Aberdeen Standard Investments re-opened the Aberdeen UK Property fund and SLI UK Real Estate in November. “The £1.6 billion SLI UK Real Estate fund shrunk to £1.47 billion by the end of November because of a £138 million net outflow. Similarly, Aberdeen UK Property saw net outflows of £89 million, meaning the fund size was £869 million at the end of November,” says Parekh. (For more on fund flows, head to our latest monthly report).

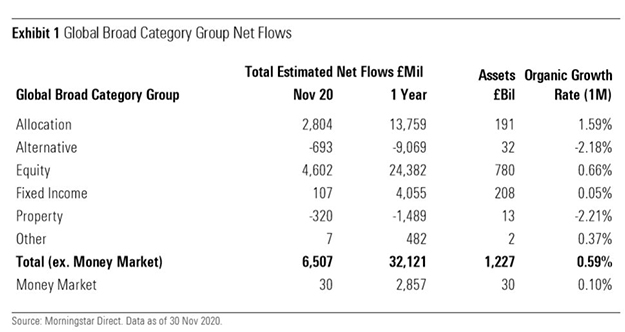

As a group, property funds saw £320 million of net outflows in November and £1.49 billion over the past 12 months. Property was just one of two categories to register net outflows for the year.