With many shops open already and lockdown about to ease for pubs, bars and restaurants, the commercial property sector is looking to get back on its feet after a bruising year.

We last looked at the open-ended property sector in March when most funds gated to investors in the midst of the coronavirus panic, meaning no one could buy or sell units in the funds. Now BMO Property Growth & Income has re-opened to investors, raising hopes that more could follow suit as conditions improve. The fund largely invests in property company shares rather than directly owning office blocks and shopping centres, so is more liquid than most, but the move is an important first step for the wider sector.

Yet, shopping centre owner Intu's (INTU) collapse into administration highlights the perilous state of the property market. Many retail tenants are struggling to pay their rent as lack of business during lockdown has seriously drained cash buffers – and that has a knock-on effect on the income that direct property funds can pay out to investors. British Land (BLND), one of the UK's largest real estate investment trusts, said it had collected 88% of rent from office tenants for the last quarter, but just 36% of rent due from retailers.

Material Uncertainty

M&G Property, the second largest fund in the sector after L&G, suspended in December, before the coronavirus crisis, raising concerns over how appropriate open-ended funds are for direct property investments. It said “unusually high and sustained outflows” had forced the temporary suspension of the funds.

In June, M&G said re-opening the fund will depend on cash levels and something called the “Material Uncertainty Clause” being lifted. The FCA requires that less than 20% of a fund’s portfolio is subject to material uncertainty (i.e. uncertain conditions making it impossible to put a value on the building) before it can re-open.

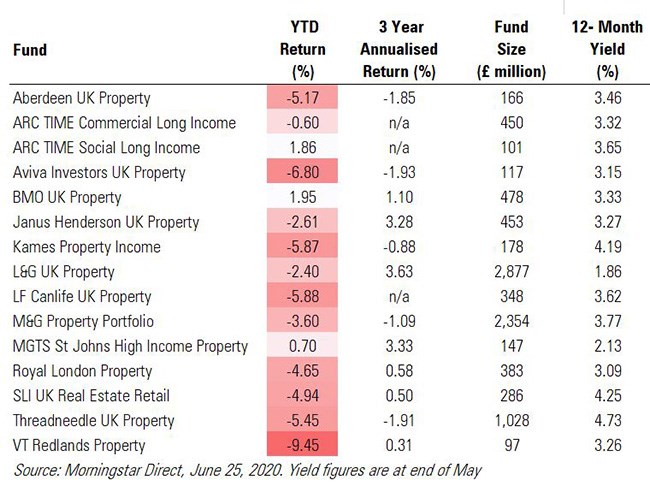

Despite the majority of funds being suspended this year, a handful have posted positive returns. By comparison, the FTSE All-Share is down around 18% year to date, backing the argument that commercial property is a good diversifier away from equity markets.

The best performer, BMO Property Fund, is up 1.95% so far this year, while the worst performer is VT Redlands Property, with a drop of just under 10%. What’s behind this disparity? BMO Property went into the crisis with a very low retail property exposure and its manager, Guy Glover, says he’s had concerns about the retail sector for years. The fund’s largest exposure is to the industrial sector, with a 38.5% weighting at the end of May 2020, followed by 31.7% in offices. Some 16.6% is in retail warehouses, which have been much in demand during lockdown.

VT Redlands, meanwhile, is a fund of funds that invests in a number of open-ended property funds and real estate investment trusts rather than directly in buildings and offices. Its biggest holding, is Janus Henderson UK Property (12.8%), followed by SLI UK Real Estate (10.1%). Other holdings include closed-end funds like Schroder Real Estate Investment Trust (SREI) – which is down nearly 40% over one year – and Silver-rated TR Property Investment Trust (TRY), which has fallen 13% since last June.

There’s a smaller disparity in performance when looking at 3-year annualised returns, with top-performing L&G UK Property posting gains of 3.63% and the worst performer, Aviva Investors UK Property, off 1.93%.

The Death of the Office?

Since the first wave of the Covid-19 outbreak, there has been much speculation that home-working means the office as we know it is doomed. That would spell disaster for funds that own expensive city centre properties if companies no longer wanted to rent them. But with many workers stuck at home with their families for three months and more, some may welcome a return to the office where there are fewer distractions and more chances to collaborate. BMO’s Glover says it will be quality over quantity for company office space in the future: “The demise of the office has been overstated. People will use offices less, but more intelligently.”

It’s been a torrid six months for the commercial property sector and the re-opening of the economy should mean the outlook is brighter for the rest of the year. All open-ended funds in the property sector have beaten the FTSE All-Share this year, but the industry is still highly exposed to the fortunes of the UK economy, which could fall into a deep recession.

And in an environment where UK blue-chip shares are axing dividends and gilt yields are negative, the funds also provide some decent income, with most yielding over 3%. As funds review their suspension every 28 days, there could potentially be a wave of re-openings this summer.