Royal Mail Group (RMG) has just inched ahead of Imperial Brands (IMB) as our stock of the week, as voted for by our Twitter followers.

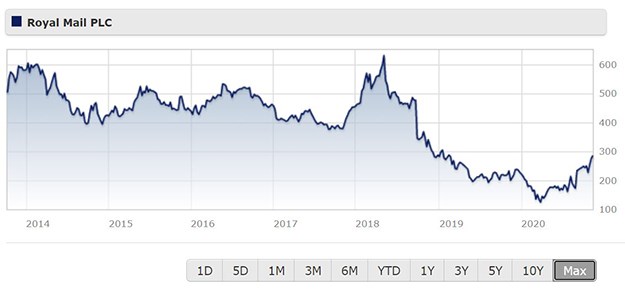

The listed letters and parcels business has had a tough time in recent years. Last time we wrote about the company, it was the second most shorted stock in the FTSE and had just cancelled its dividend for the full financial year of 2020-2021. But Royal Mail has benefited from the lockdown delivery boom and its shares are higher than at the start of the year, moving back above 300p after the recent market rally, not far off its float price in 2013 of 330p. Is this recovery a sign that investors are finally buying into Royal Mail’s restructuring plans?

The company has just put out results for the last six months and the profit figures were very much second class rather than special delivery: pre-tax profits dived 90% to £17 million (they were £173 million the year before), pushing Royal Mail to an operating loss of £20 million, which is even steeper if you factor in redundancy payments and Covid-19 costs.

However, revenue was up nearly 10% to £5.6 billion. And for patient income investors, the company said that it plans to restart dividend payments in the next financial year. Before the crisis, the company was a staple of many income funds, but its yield started to push above 13% after a slump in the share price.

The company did deliver a milestone in the reporting period: for the first time revenue from parcels exceeded that from letters, a sign of the times as e-commerce booms in lockdown. The number of parcels delivered (excluding Amazon deliveries), was up 51% in the last six months, while parcels revenue was up 33%, against a decline of 21% for its letters business. It has tapped into the European logistics boom via its GLS business, which makes up over 30% of group revenue.

Beware Amazon

Even though the current environment has broadly been good for Royal Mail’s parcels business, the company has admitted it has underinvested in this area and was unprepared for the sudden spike in deliveries. Former stock of the week Amazon has built its own delivery and logistics network and bypasses Royal Mail for many larger parcels.

Why doesn’t Royal Mail just ditch its letters business and focus on lucrative parcels? Any other listed business would be able to do this, but Royal Mail is bound by regulators to deliver to every UK address six days a week for a standard price. If you’ve ever been taken aback by the price of a first-class stamp – it’s gone up from 12p in 1980 to 76p today – regulator Ofcom says it’s ready to step in if Royal Mail charges too much. The next review of this “universal service obligation” is due in 2022.

Keith Williams, interim executive chair, says that Royal Mail needs to speed up the pace of change to make the UK business profitable again, but expects the parcels division to keep growing this year:

"It remains difficult to give precise guidance but parcel growth is expected to remain robust in Q3, with more uncertainty over trends in Q4 due to the development of the Covid-19 pandemic, further recessionary impacts and trends in international volumes."

In share price terms Royal Mail floated in 2013 at 330p and members of the public and staff snapped up shares at discounted rates in a much-hyped IPO. The shares quickly spiked to above 600p in the aftermath of the float, but have been on a steep decline since May 2018 until hitting a trough of 124p in the midst of the March crash.