With just a week to go before the US presidential elections, it may be worth considering how investments can help to minimise volatility. A number of exchange-traded funds (ETFs) have this remit and are a valuable tool in a portfolio for times of uncertainty.

US presidential elections are almost always a source of volatility for stock markets. Adding to the usual tumult this time around are uncertainties surrounding postal ballots, which are set to surge this year as voters stay home amid Covid-19 concerns. A close result could trigger recounts or even an arbitration in court, which could leave the country in limbo and set the stock market spiralling.

Investors in US equities seeking to position themselves defensively may consider using minimum or low volatility ETFs, which are designed to thrive in periods of uncertainty. By building a low risk portfolio, these funds tend to outperform the broader market in downturns while also allowing investors to participate in market gains.

What are Minimum Volatility ETFs?

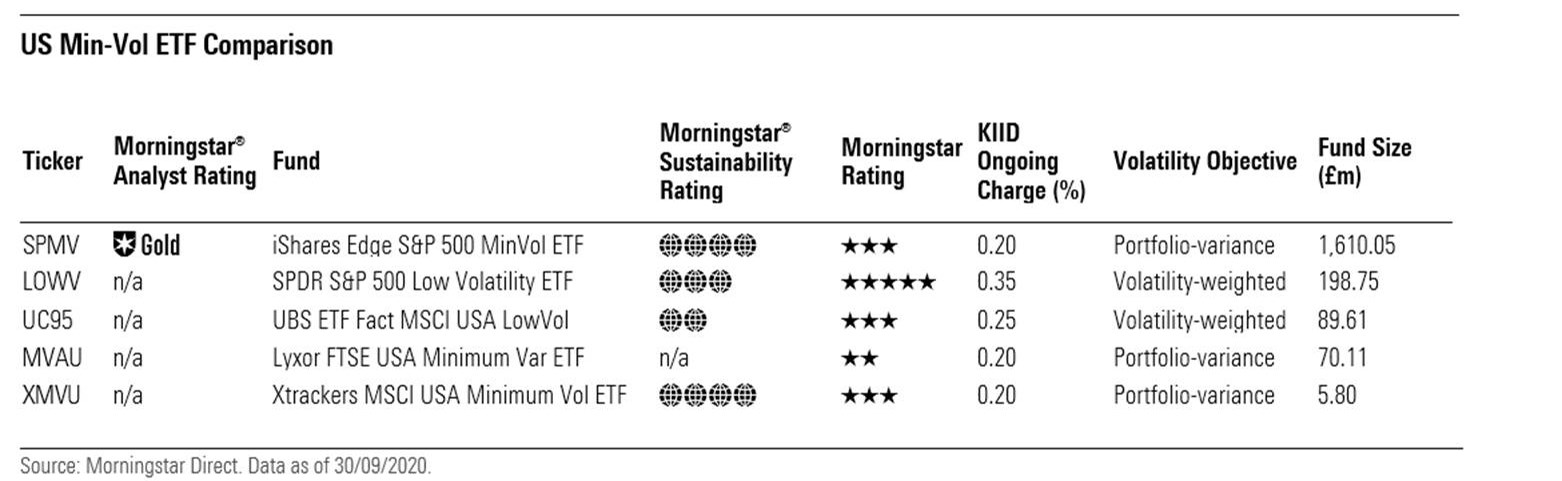

Minimum-volatility (or min-vol for short) ETFs aim to make a smoother ride of equity markets by lowering volatility and improving downside risk and remain. These funds have proved themselves as some of the more popular strategic-beta offerings in Europe. The below table highlights some of the options for US equities available to UK investors.

Constructing a portfolio that focuses on reducing volatility typically takes one of two approaches: creating risk-weighted portfolios of low-volatility stocks, or creating optimised minimum-volatility portfolios.

The first approach includes volatility-weighted strategies such as SPDR S&P 500 Low Volatility ETF (LOWV). These funds seek to maximise exposure to the volatility factor by overweighting stocks with low historic volatility and underweighting stocks with high-volatility characteristics. Ranking stocks this way offers a certain degree of style purity, as the methodology ensures that only stocks with low-vol metrics are included in the final portfolio.

On the other hand, minimum-volatility portfolio strategies such as the iShares Edge S&P MinVol ETF (SPMV) use optimisation techniques to find the right combination of stocks that create the lowest portfolio variance/volatility on a forward-looking basis. In this example, the index selects around 100 stocks from the S&P 500 Index. This methodology focuses on how the stocks interact with each other in the portfolio. While pure low-volatility portfolios hold only low-volatility stocks, this minimum-volatility portfolio may comprise of average- to high-volatility stocks because of the diversification benefits they bring to the overall portfolio. The constraints built into the optimiser ensure that the overall volatility of the portfolio is kept in check.

How do Minimum Volatility ETFs Perform?

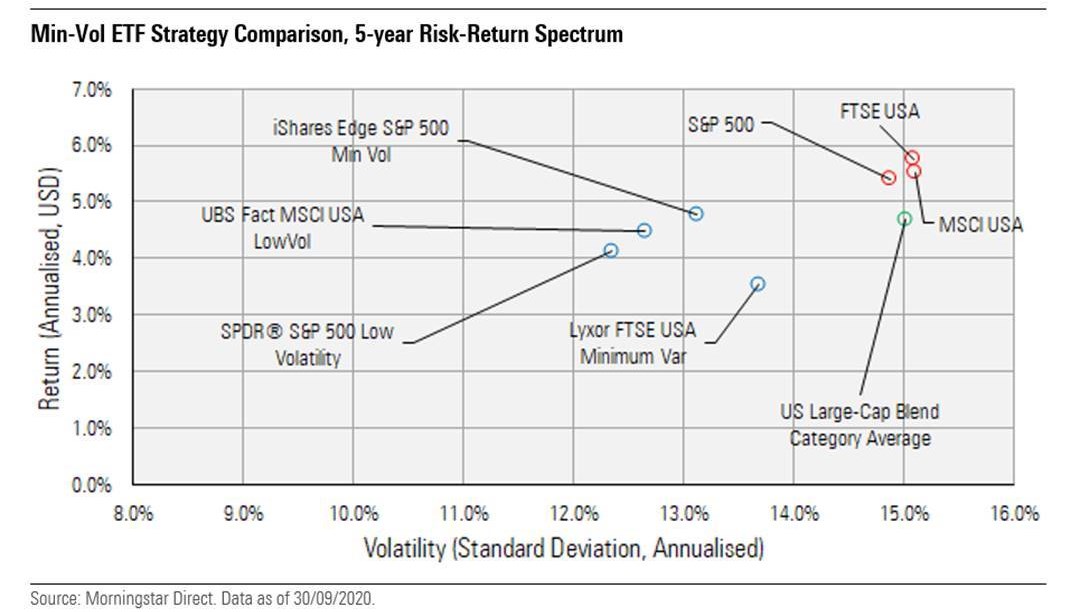

Irrespective of the approach, these strategies have historically offered lower volatility compared to both their parent benchmarks and active US equity funds. The diagram below compares some of these strategies on a risk-return spectrum over five-years, with lower volatility strategies sitting towards the left of the spectrum. Over this period, the min-vol strategies have proven the less-risky option.

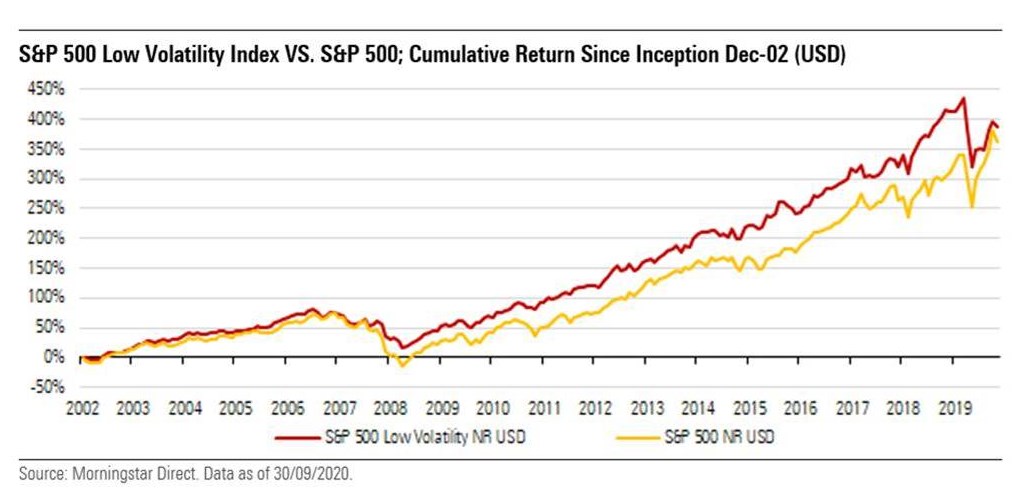

Comparing the S&P 500 Low Volatility Index with the broad S&P 500 Index in the chart below, we can also see how consistent downside protection during periods of market stress – for example, the financial crisis of 2008 – has so far translated into superior performance for the low-vol index over the full period of analysis.

But performance during 2020’s Covid-19 pandemic sell-off and subsequent recovery highlights the weakness of these strategies, namely lagging the broad market in strong bull markets and recoveries. While delivering a portfolio that is inherently less correlated with market returns is indeed characteristic of such a defensive offering, limited upside potential is something for investors to bear in mind.

.jpg)