Much of Europe is housebound and the global economy is still reeling from the unprecedented impact of the coronavirus and plummeting oil prices. At this point, the implications for the global economy are far from clear.

That said, the lessons learned from previous crises offer are more obvious: sit tight and wait it out. While this remains sound advice for investors with a long-term outlook, for those with shorter investment timeframes, preserving capital may be a higher priority.

Switching core allocations out of equity into fixed income is a move which may still benefit some investors considering the large risks still left on the table. We have recently looked at three fixed income ETFs which would be worth considering in this circumstance. On the other hand, a switch of this sort now may also crystalise losses and stop investors enjoying any equity recovery.

Factor investing with strategic beta ETFs can provide a middle ground, allowing investors to trim risk while maintaining exposure to a market rebound.

A Refresher on Factor Investing

Strategic or smart beta ETFs often track an index which attempts to exploit the same well-established alpha “factors” targeted by active managers. The five equity factors that best hold water are: value, momentum, size, quality, and minimum volatility. Each factor has its own unique investment characteristics.

Quality and Low Volatility are the two factors considered to be most counter-cyclical, meaning that they tend to lag in bull markets and outperform in downturns.

Quality strategies look to build a portfolio of stocks composed of quality companies, which are characterised by their durable business models and sustainable competitive advantages. These companies tend to have high and stable levels of profitability and clean balance sheets, meaning they are well positioned to weather a downturn.

Minimum volatility strategies attempt to build a portfolio with the lowest volatility from a given universe. Investors in low vol strategies are also making an implicit quality bet – as lower volatility stocks also tend to operate with lower leverage and have more stable earnings growth. Unsurprisingly this approach also favours defensive stocks.

How have they performed so far?

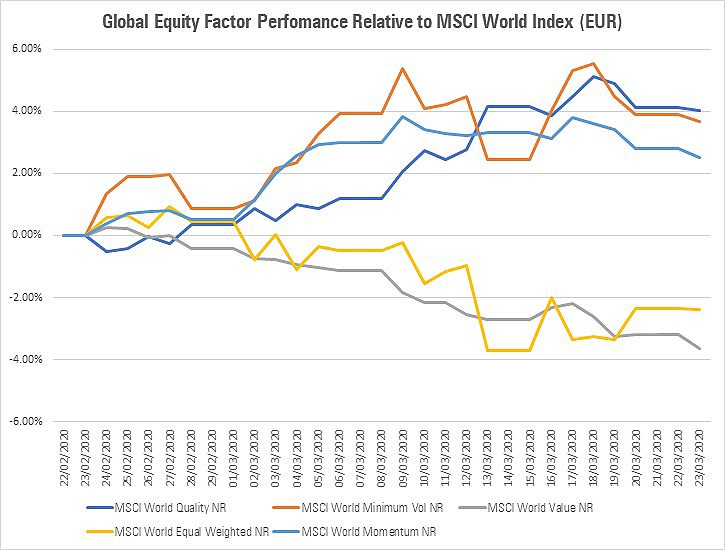

Both strategies have performed as expected. The chart below shows the one-month trailing relative performance of each of the five main equity factors versus the MSCI World Index, a proxy for global large.

We can see that both Quality and Minimum Volatility are the best performing factors, falling around 4 percentage points less than the MSCI World Index (which has itself plummeted 33%) over the past month.

This contrasts with the pro-cyclical Size and Value factors which have each sunk around 3% lower than broad equities over the same period.

Three Defensive ETFs

The Silver-rated iShares Edge MSCI World Minimum Volatility ETF (MVOL) is one Morningstar's top-rated global equity funds. It attempts to construct the least-volatile portfolio possible with stocks from the flagship MSCI World Index, under a set of constraints. These include limiting turnover, exposure to individual names, and sector tilts relative to the index.

Other funds within the same stable which leverage a similar strategy in different equity markets include the Silver-rated iShares Edge S&P 500 Minimum Volatility ETF (MVUS).

Elsewhere, the Bronze-rated Xtrackers MSCI World Quality ETF 1C (XDEQ) targets large- and mid-cap global developed stocks with the best profitability (measured by return on equity), the strongest balance sheets, and most consistent earnings growth within each sector.

To mitigate unintended sector bets, the fund matches its sector weightings to the broad market-cap-weighted MSCI World Index. Within each sector, the fund weights its holdings according to both the strength of their quality characteristics and their market cap. This pulls the fund toward stocks with durable competitive advantages, such as Microsoft, Apple, and Johnson & Johnson.