The amount of money invested into sustainable ETFs in Europe has increased almost sevenfold over the past three years. Investors now have €41 billion in these low-cost tracker funds.

As interest in such funds has increased, so too has the array of options available to investors. There are now nine sustainable ETFs focused on emerging market equities.

Emerging markets may not strike investors as a typical hunting ground for ESG investments; they have historically lagged their developed market peers when it comes to environmental, governance and social matters. Economies that are rapidly industrialising and fast-growing populations, for example, mean its little surprise that emerging markets include some of the world’s worst polluters.

In 2017, China was the world’s largest carbon dioxide producer, accounting for around 27% of global emissions, says Morningstar associate analyst Briegel Leitao. He has taken an in-depth look at sustainable Emerging Markets ETFs, to see how they approach the ESG challenges in the region.

Tracker Funds for ESG

ESG ETFs can provide investors with a cost-effective and transparent way to access a market of their choice. These funds may use screening to exclude stocks with unfavourable ESG characteristics to help accommodate investors’ preferences. Leitao adds: “This can certainly improve the sustainability profile of many standard index trackers, but it inevitably adds risk.”

There is, says Leitao, typically a positive correlation between how the strictness of the sustainability screen and the amount of active risk compared to the wider index. Investors can offset this by adding in sector or geographic constraints to help reduce the big bets being taken, but that can be difficult to achieve when you’re considering emerging markets, where there are 26 very different countries in the index.

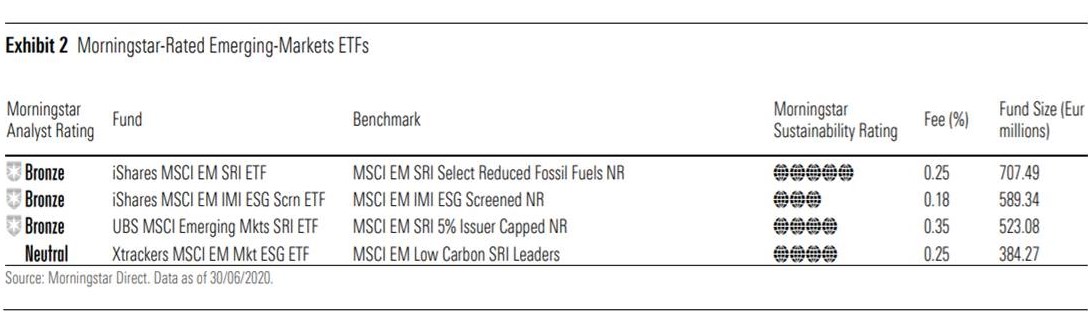

The chart below identifies the four largest ETFs in this part of the market, detailing their fees and sustainability rating. Scores range from the highest Morningstar Sustainability Rating of five globes, to an Average rating of three globes. That gives us some indication that these funds are taking very different approaches.

Leitao explains: “All four of these ETFs use the same basic controversy screen, taking the underlying universe and, based on MSCI ESG Controversies and Business Involvement Screening, exclude companies involved in controversial and nuclear weapons, civilian firearms, thermal coal, oil sands and tobacco.” This screen targets the very worst offenders and filters out around 9% of the parent index.

This forms the core of the strategy of the iShares MSCI EM IMI ESG Screened ETF; it has the lowest sustainability rating of these four, indicating the fairly light-touch screening process.

Those looking for a stricter screen might instead look to the Xtrackers MSCI Emerging Markets ESG ETF, says Leitao. This tracker adds further screens, cutting the bottom-scoring 50% of companies in the universe based on their environmental, social and governance scores, and the top 20% of stocks based on carbon-emissions intensity.

“As of June 2020, the fund tightened its business involvement screening and also introduced a new screen covering adult entertainment, GMO products, and thermal coal,” he adds. And a final screen is applied too, ruling out tobacco producers or firms earning 5% of more of their revenues from tobacco-related products. The stricter process earns it a four globe rating.

The two five-globe rated ETFs in the table go further still. Both target the top 25% of companies in the MSCI Emerging Markets index based on their ESG scores, and each holding is capped at a maximum of 5% of the portfolio to avoid concentration.

Consider Sector and Country Risk

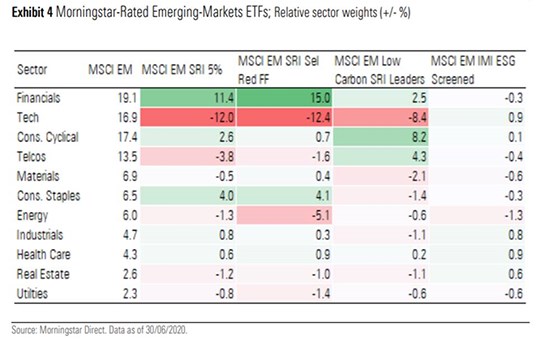

Using screening does, of course, mean you are taking active bets, which brings with it risks. Three of the funds in the table use sector constraints to limit exposure to various sectors, but Leitao says the results are mixed. The below table shows a snapshot of sector positions, highlighting how radically the funds’ positions can deviate from parent benchmark.

The MSCI Emerging Markets SRI 5% Index, for example, has an 11.4% overweight position to financials compared to its parent index, and is 12% underweight to tech. These positions represent steep bets on the respective sectors. It’s worth pointing out, too, that financials already make up the largest sector allocation in emerging markets at 19%; the SRI strategies further build on this by bringing the allocations to more than 30%.

Leitao adds: “Ultimately the success of targeting sector weights is reliant on the percentage of the original opportunity set that’s left after applying ESG screens. This can lead to persistent overweights and underweights, and a performance drift versus the unscreened sector.”

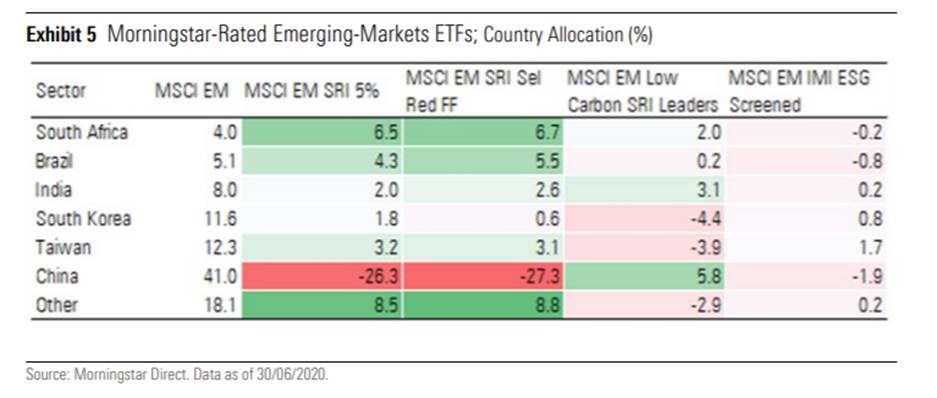

Country risk is always a factor for investors to consider, and particularly within emerging markets where political instability or currency-fluctuations can seriously influence returns. While none of these ETFs apply geographic constraints, some of the funds allocate quite differently across emerging markets countries, as shown below.

Leitao says: “Again we find the stricter SRI strategies making the biggest impact. For these, China’s weighting more than halves to 15%, a drop that can be attributed to the low ESG scores awarded to Chinese firms. The 5% individual stock cap also disproportionately impacts the larger stocks in an index, many of which are Chinese.”

Meanwhile, countries with higher ESG scores, meanwhile, such as South Africa and Brazil, are over-represented in many of the portfolios. However, the MSCI Emerging Markets Low Carbon SRI Leaders strategy, which has no cap on individual holdings, is overweight to China.

Leitao adds: “Investors in this fund will find themselves with nearly half their allocation to Chinese equities and a disconcertingly top-heavy portfolio. At the time of writing, the top 10 constituents accounted for more than 40% of the total weight. Risks such as these may make this strategy unviable for some investors.”