With shopping centres closed and high streets deserted because of the coronavirus lockdown, this is not a good time for funds that own commercial property.

Concerns about liquidity have plagued the sector since the Brexit vote in 2016, and many experts argue that open-ended funds are not suited to investing in illiquid assets such as office blocks and shops. Most open-ended funds that invest directly in property have now suspended trading to stop a wave of redemptions from investors, meaning around £5 billion of investor’s money is frozen in these funds. Industry experts appointed have warned that in the current climate it’s impossible to put a proper valuation on these assets.

M&G Property, one of the largest funds in the sector, suspended dealings in December, and this year more funds have followed suit as the coronavirus outbreak has sparked widespread panic across global markets. The last time there were so many property funds suspended was after the Brexit vote in June 2016, when there were fears the UK's exit from the bloc could cause a collapse in the property market.

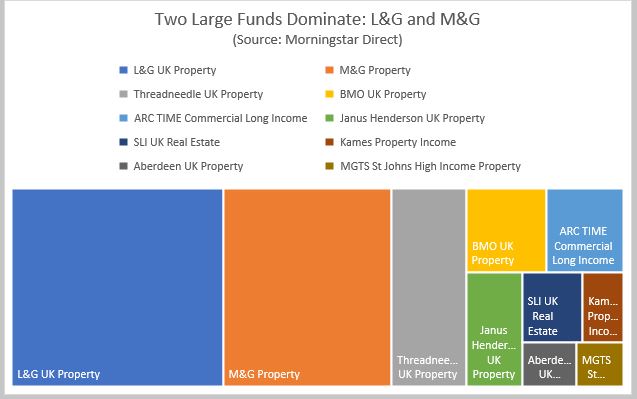

We have looked at the 10 biggest funds by assets under management in the IA UK Direct Property sector to assess their performance year to date as well as since the Brexit vote. The below chart indicates the funds by size.

As you would expect, performance has been hampered this year by a move away from risky assets, especially those exposed to the fate of the wider economy such as commercial property. There are widespread predictions that after months of home working while on lockdown, many businesses may look to reduce their office space in the future.

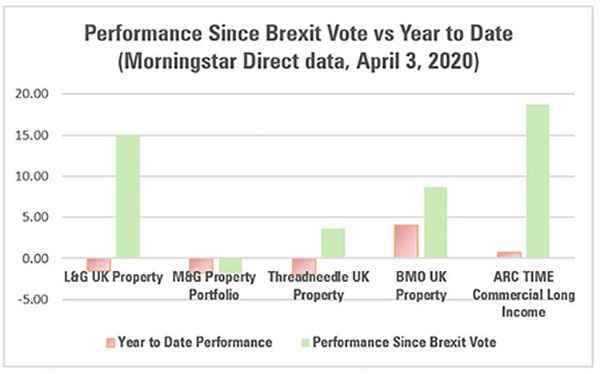

Just three funds have achieved positive returns in the year to date – BMO UK Property, ARC TIME Commercial Long Income and MGTS St Johns High Income – but this is impressive in the context of a slump in equity markets. In comparison with the equity markets, the FTSE All-Share is down 26% so far this year and down 6.8% since the Brexit vote. The three funds that have gained so far this year are also the ones that have posted positive returns over both time periods.

Looking at the longer-term performance there is a big difference between the strongest and weakest funds: ARC TIME Commercial is up 18.8% since the Brexit vote, but Aberdeen UK Property down 2.4% since then.

Supermarkets and Shopping Centres

A delve into the types of buildings these funds own gives some clue as to why there is such a disparity in their performance.

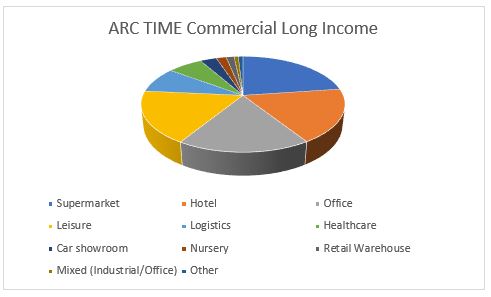

For the ARC TIME Commercial Long Income fund, supermarkets make up a big chunk of the portfolio and these have been key retailers in recent weeks. The fund owns stakes in Sainsbury’s and Morrisons outlets across the country, for example. Retail warehouse and logistics space, meanwhile, make up more than 10% of the fund’s assets and these are areas which have proved resilient, if not vital, in recent weeks as households rely on e-commerce to get goods delivered while they are on lockdown.

On the flipside, leisure, hotel and office space have been hit hard by the lockdown: the fund owns stakes in Holiday Inn Southend and a Travelodge branch in Kingston.

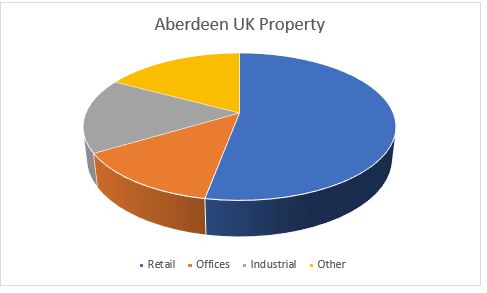

Retail space dominates the portfolio of Aberdeen UK Property, meanwhile, which has been the worst performer since the Brexit vote. With the sector accounting for more than half of the fund's portfolio, its assets include Sheffield's shopping district The Moor and the Broadwalk shopping centre in Edgeware.

For these retail-heavy funds, a lot depends on how quickly the lockdown is lifted and how soon people can go back to work and shoppers to venture out again. The question of fund suspensions is another one for investors to grapple with; Ryan Hughes head of active portfolios at AJ Bell says the length of time M&G has been suspended (currently five months) may give a clue to how long investors will have to wait. “Investors will understandably find these closures distressing at such an uncertain time in markets. However, there’s nothing they can do now but wait it out and hope that the suspensions don’t drag on for too long,” he says.