A fall in the stock market can often be an opportunity for brave investors to pick up shares at bargain prices. Indeed, after the March sell-off, many stocks covered by Morningstar are now trading below their fair values.

And while some of these companies have strong economic moats that should hold up well even in a downturn, others may be little more than a value trap - a stock that is cheap, but for good reason.

The Morningstar star rating, which runs from one to five, can be a useful in tool in identifying these. A five-star rating indicates a business trading for less than what it's worth, while a one-star rated stock is deemed to be expensive relative to its fair value - these could be stocks to avoid.

Avoid the Value Traps

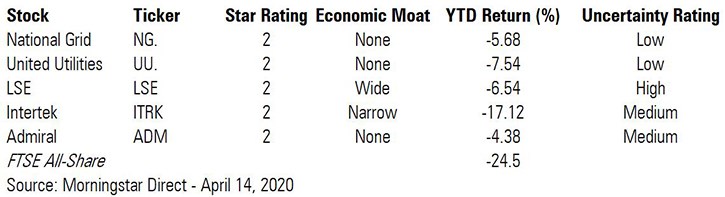

While no UK stocks have fallen to a one-star rating, a handful have dropped to two stars stocks and they come from a wide range of sectors, including car insurance, utilities and industrial testing.

Classic defensive companies like National Grid (NG.) and United Utilities (UU.) now look expensive compared to their fair values, according to Morningstar analysts, and come with the added risk of having no economic moat. Although the Uncertainty Rating for the businesses is categorised as low, utilities analyst Tancrede Fulop thinks UK companies in this sector are currently carrying too much debt and that their dividends are under threat.

While these firms have not been immune to the recent sell-off, year to date their share prices have fallen less than the FTSE All-Share, which is off nearly 25%. National Grid is down from 950p at the start of the year to 896p now, a fall of just under 6%, but analysts think this is still too high, assigning a fair value of 800p to the shares. United Utilities shares are 7.5% lower than at the start of the year at 880p, but analysts think they’re worth 700p.

London Stock Exchange (LSE) shares are off 6.54% since the start of the year but are up on a one and five-year basis: since April 2019, the shares are up 58% and 209% higher than in April 2015. Still, Morningstar analysts say the shares are worth £59 - some 16% below the current price of £70.

LSE is a favourite of many “buy and hold" managers such as Nick Train, whose Finsbury Growth & Income Trust (FGT) has the stock among its top holdings. Unlike all the other companies on our list, LSE has a wide moat and is overvalued. Analyst Eric Compton the company's track record speaks for itself: “LSE’s shares have produced an annualised total return of about 30% for the past decade, an impressive achievement. If anything, we have had a hard time projecting just how successful LSE’s future endeavours would be.”

Pricey Tech Stocks

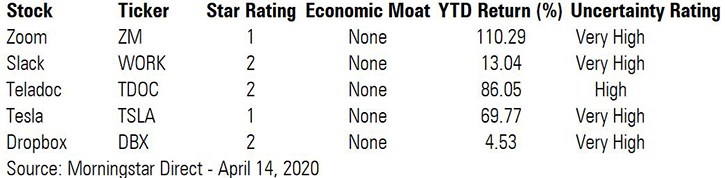

Looking further afield, a number of high-profile US companies are now trading way above their fair values. Among them are companies whose shares have soared as lockdown life boosts demand for video conferencing (Zoom), remote working technology (Slack) and virtual medical appointments (Teladoc).

Zoom’s (ZM) share price has more than doubled this year to more than $140, but Morningstar analysts think they are significantly overpriced, with a fair value of just $69. They argue the current value is unsustainable. “Shares have run ahead of levels that fundamentals can support,” says Dan Romanoff, noting that many of those using Zoom for the first time have signed up as free users. He also points out that if corporate life returns to “normal”, demand for the company's services will drop off again.

File-sharing firm Dropbox (DBX) is also overvalued with a very high uncertainty rating, as is electric vehicle company Tesla (TSLA), which saw a big spike in its share price before the coronavirus sell-off. "Tesla has a chance to be the dominant electric vehicle firm ... but we do not see it having mass-market volume for about another decade," analyst David Whiston says. Tesla is assigned a fair value estimate of $239, a staggering 66% below its current price.

According to Morningstar analysts, none of these companies have economic moats and all have high uncertainty ratings, a measure of risk, which we’ve recently looked at this in the context of UK companies.

Morningstar’s Susan Dziubinski says this uncertainty can take many forms – including less predictable sales, bigger debt and more vulnerability to external events. “In a turbulent and uncertain economic and market environment, these are the types of stocks to avoid,” she says of those with a high uncertainty rating. She says that even though Zoom et al have ridden the wave of the home-working boom, investors must consider shares prices in their longer-term context and these are overvalued after strong gains this year.

.jpg)