.jpg)

2023 has been tumultuous. At the time of writing, global markets are up almost 15% year to date. That's a very solid return given the sub-optimal market conditions we've been facing. But these returns were not delivered in a straight line, with two significant market falls in April and October. You really did have to be "in it to win it".

Inflation has come down a long way from the double digit levels of late 2022, and has now back to 2.4% in the Eurozone and likely below 3% in the US at next print. Growth across the two regions contrasts however, with the Eurozone treading water and the US economy continuing to grow.

Lower inflation does not mean we are entering the sunlit uplands, and it's important to recognise the challenges that 2024 will bring.

- We might not have seen the last of inflation. Energy prices are notoriously volatile, and a spike over the winter could have a major impact. Likewise, while it is great that the US economy is so resilient, labour markets remain tight, and the danger of overheating lives on.

- Central banks took swift action to combat inflation, bringing interest rates to the highest levels since before the global financial crisis. The impact of these elevated rates is now setting in and will negatively affect growth in 2024. We forecast GDP to fall next year from 2023 levels.

How Should Investors Position Themselves?

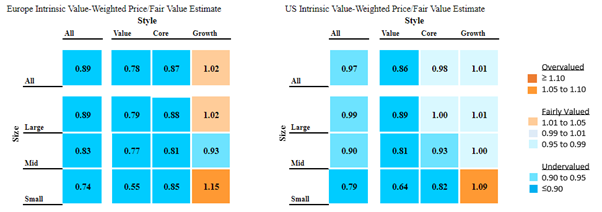

Stylistically we are seeing similar patterns in US and European markets. Overall the markets themselves are still undervalued, though just barely in the case of the US. Within that, the picture is bifurcated.

Growth as a style is slightly overvalued in both regions, a situation we do not see changing soon, with interest rates likely to fall next year and investors keenly aware of the benefit lower rates would have for growth stocks.

Are There Opportunities in Value Stocks?

Value stocks are trading at an attractive discount to their intrinsic fair value estimates, even more so in Europe. The reasoning here is obvious; investors are still concerned about the health of the economy, and value stocks, often in cyclically exposed areas, will take a big hit if the economy stutters in 2024. That said, within the value segment we definitely see pockets of opportunity, particularly amongst Moaty names – companies with a competitive edge.

Lastly, small cap value stocks remain the sick man of equity markets. The worst of both worlds to many investors, they combine cyclical exposure with the downsides of being small, such as reduced access to cheap debt. Everything has a price of course, and 50% upside potential, in the case of US small cap value stocks, is tempting. Be aware of the tail risk here.

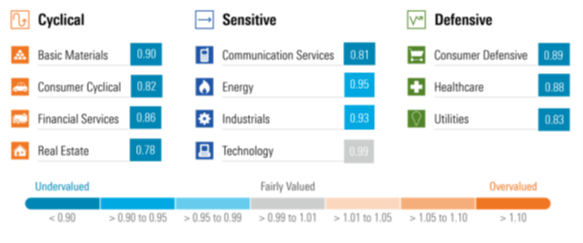

What Sectors Should I Invest in?

On a global basis, the likes of consumer cyclicals, communications, and real estate offer the most attractive discounts right now. While there is merit to scoping out these areas in more detail, there is no obvious catalyst for these discounts to fair value to close, other than a material improvement in the underlying macroeconomic environment.

So instead, I'm going to highlight two other sectors to look at in 2024, for the reason that these sectors weren't always cheap; their attractive discounts only appeared recently. Given the uncertain macroeconomic situation, both sectors' defensive qualities could prove helpful should the winds change for the worse.

Healthcare

It's rare we get to highlight this sector as attractive, as its defensive qualities and growth profile are usually well appreciated by investors. This time around, however, investors are concerned about patent cliffs and whether innovation growth will come through over the next few years to offset this. We see plenty of interesting areas of innovation, particularly in places like oncology and immunology, which traditionally have strong pricing power.

Utilities

It's no mystery as to why investors have lost their enthusiasm for the utilities sector over the last six months. For the previous decade, the sector had offered an attractive dividend yield north of 4.5% in Europe. Compared to the pittance government bonds were offering at the time, the choice was easy for income seekers. Today, yields on 10-year government bonds exceed the income from utility stocks, and investors have fallen out of love. The pattern will reverse as interest rates fall, creating upside for a sector that's trading at steep discounts.