.jpg)

In Morningstar's inaugural European Telecoms Pulse report, analyst Javier Correonero takes stock of the sector's valuation and future upside, and highlights two strong contenders in the space.

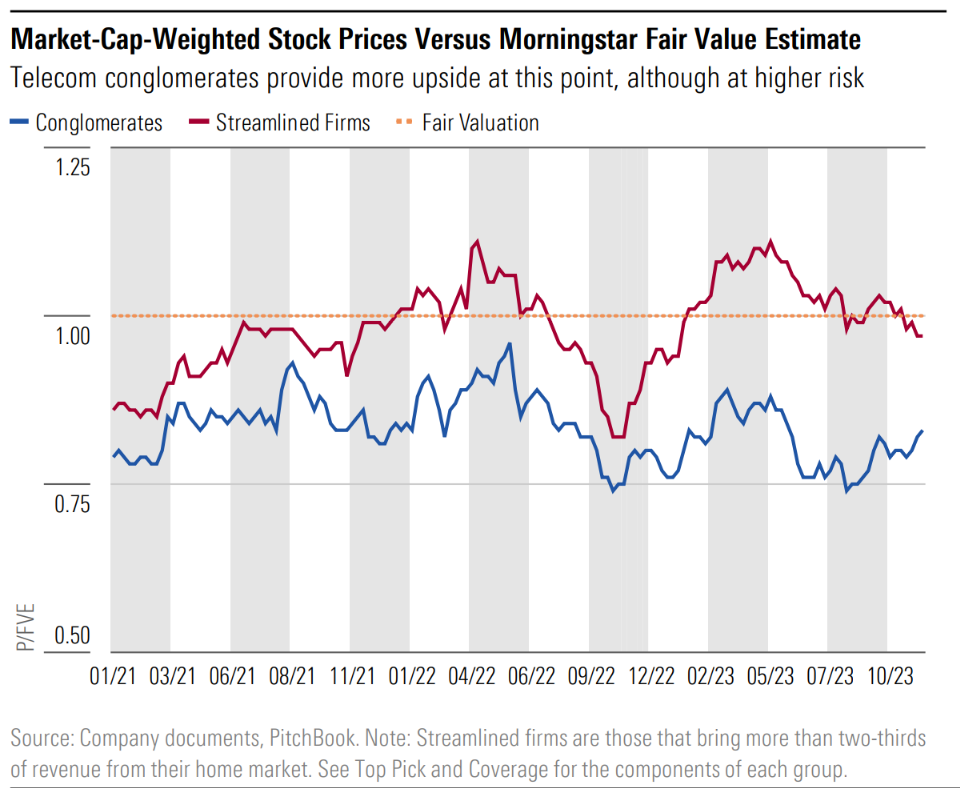

1. Telecom Conglomerates Offer Higher Upside, Albeit at Higher Uncertainty

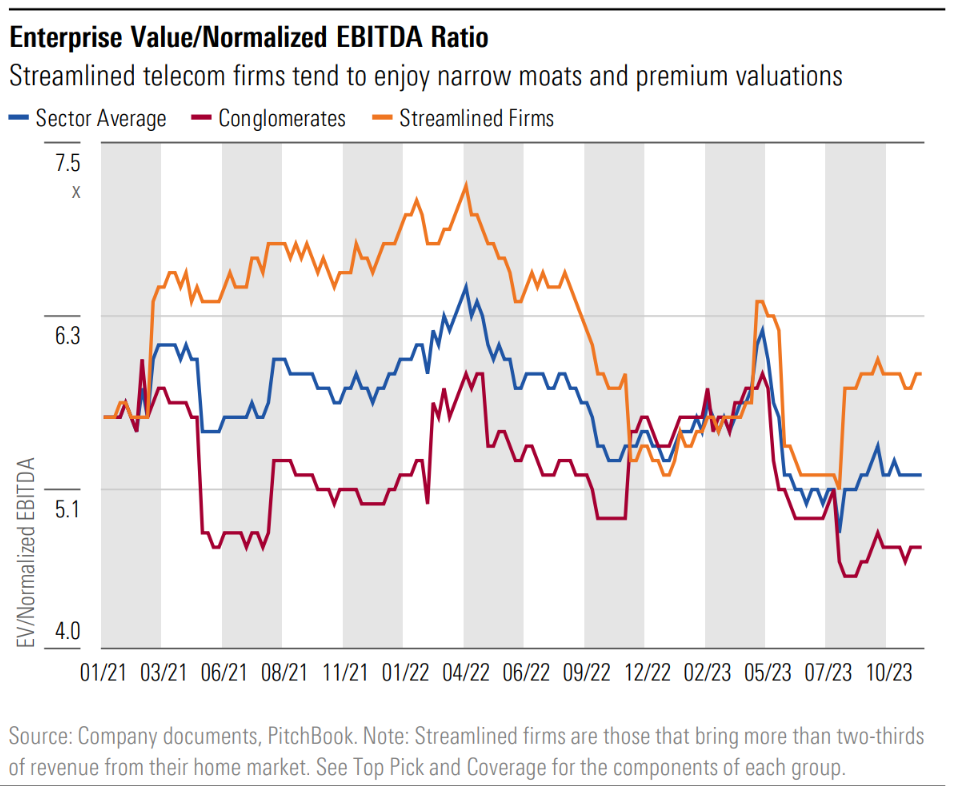

Telecommunications conglomerates are trading at around 0.8 times price/fair value, offering a larger discount than streamlined firms. Historically, conglomerates trade at lower enterprise value/EBITDA multiples given their more complicated corporate structure and lower cash flow visibility explained by differing market dynamics in different countries and currency fluctuations. Investors in conglomerates can get a higher return on investment but must be aware of the pitfalls mentioned above. At similar valuations, we tend to prefer streamlined firms due to their more straightforward narratives and better visibility.

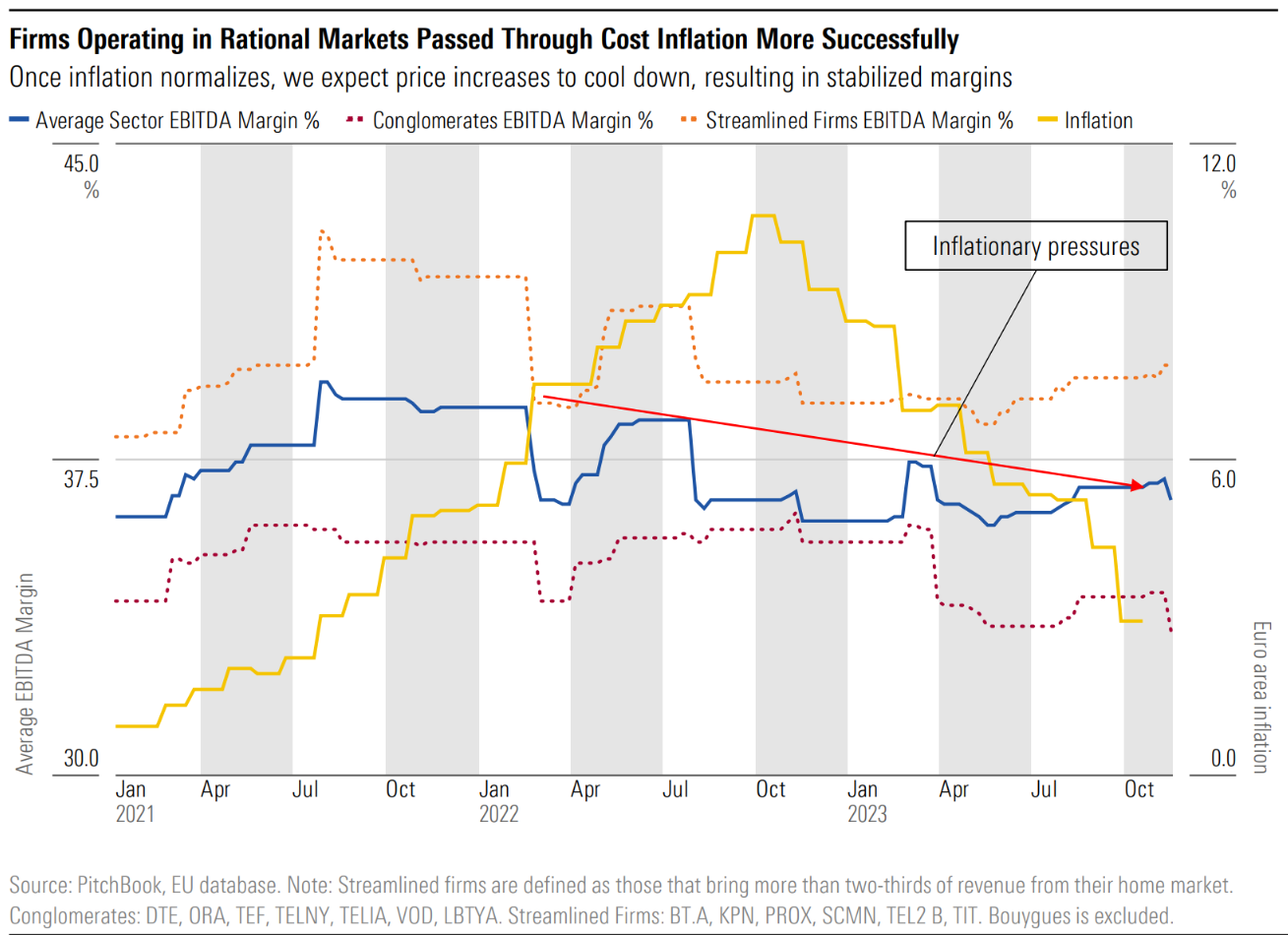

2. Wage and Energy Inflation Has Put Pressure on EBITDA Margins

Inflation has affected telecoms’ cost base, mainly wages and energy expenses, and has put pressure on EBITDA margins in the last few quarters. Firms are passing inflationarypressures to its end customers through price increases, although more successfully in some cases than others. The U.K. has successfully passed through inflation to final customers, as the industry increased prices with limited effect on churn rates. BT Group executed several price increases while keeping churn close to 1%. In other rational markets, like the Netherlands or Germany, price increases were also effective. In Italy and Spain, where a price war and very tough competitive conditions exist, price increases are yet to be effective, as subscribers switch to cheaper operators. The same occurs in France, where Orange and Bouygues experience market share drip to Iliad, given its lower prices.

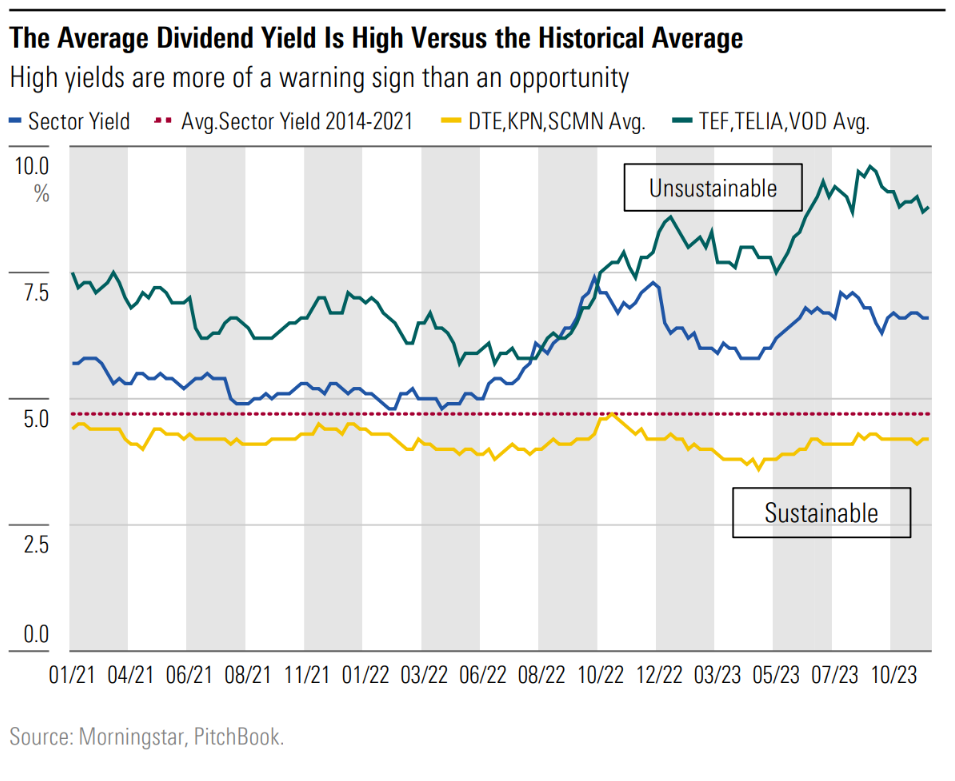

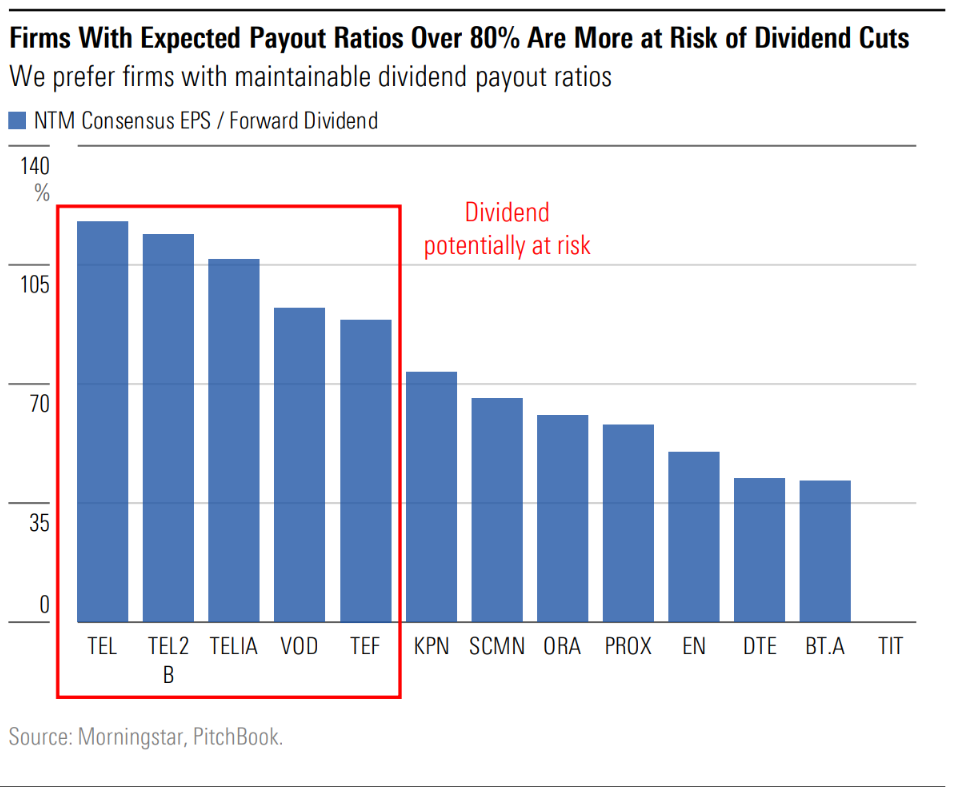

3. As Yields Trend Higher, Investors Should Grow More Cautious

The average dividend yield stands at 6.7%, with some firms offering 8% to 9%. Firms with maintainable yields have lower risk of dividend cuts and the potential for dividend

growth in the future. For example, DTE, KPN, and Swisscom have offered stable or growing dividends in the past five years.

Payout ratios above 80% carry dividend cut risk. Historically, European telecoms offering unmaintainable payout ratios have often cut dividends or resorted to scrip dividends, which are dilutive. Investors looking at high dividend yields as opportunities should be aware of these risks.

Our Top Picks

Deutsche Telekom (DTE)

Market cap: EUR110.6b

Rating: ★★★★

Moat Rating: Narrow

Narrow-moat DTE offers investors exposure to two rational telecommunication markets, U.S. and Germany, and to a management team with an Exceptional Capital Allocation Rating. Deutsche Telekom shows the financial discipline and operational knowledge required to generate excess returns in the competitive telecom industry. In the U.S Deutsche Telekom has executed a brilliant M&A strategy over the years, acquiring MetroPCS and Sprint acquisitions and realizing ambitious cost synergies. Since its merger with Sprint in 2020, DT has steadily been gaining share from Verizon and AT&T. In Germany, Deutsche Telekom leverages its better networks and knowledge of the market and executes gradual price increases that result in steady revenue and EBITDA growth. Investors in DT can expect good organic execution, with growing shareholder distributions in the form of buybacks and dividends. Since 2019, DT's dividend has grown from EUR 0.60 per share to EUR 0.77, and we see room for mid-single-digit dividend increases.

Tele2 (TEL2B)

Market cap: SEK57.8b

Rating: ★★★★

Moat Rating: Narrow

Investors in Tele2 can expect nicely growing dividends in the future thanks to good management execution, a cost-conscious mentality and exposure to stable or growing markets. In the past decade dividends have grown at a 4.5% CAGR. We grant Tele2 an Exceptional Capital Allocation Rating. We expect revenue will grow at low-single digits with EBITDA growing at mid-single digits in the coming years. In Sweden (80% of revenue), Tele2 is outperforming Telia, stealing market share in both mobile and fixed thanks to better execution and Telia's overpriced services. Tele2 has a costconscious mentality, paramount in the competitive telecommunications industry, having reduced its operating expenses meaningfully in the past decade. Around 20% of revenue comes from the Baltics, where Tele2 has been growing its top line at mid to high-single digits for many years. Over the years, Tele2 has properly understood the dynamics of European telecommunication markets and has acted accordingly. The firm understands that telecommunication companies tend to have stronger positions in their home market and weaker positions abroad. It has therefore narrowed its business, selling most of its operations abroad.

Compiled by Lukas Strobl.

.jpg)