As part of our special emerging markets week, we look at how African equity markets have performed and what countries are emerging as new powerhouses.

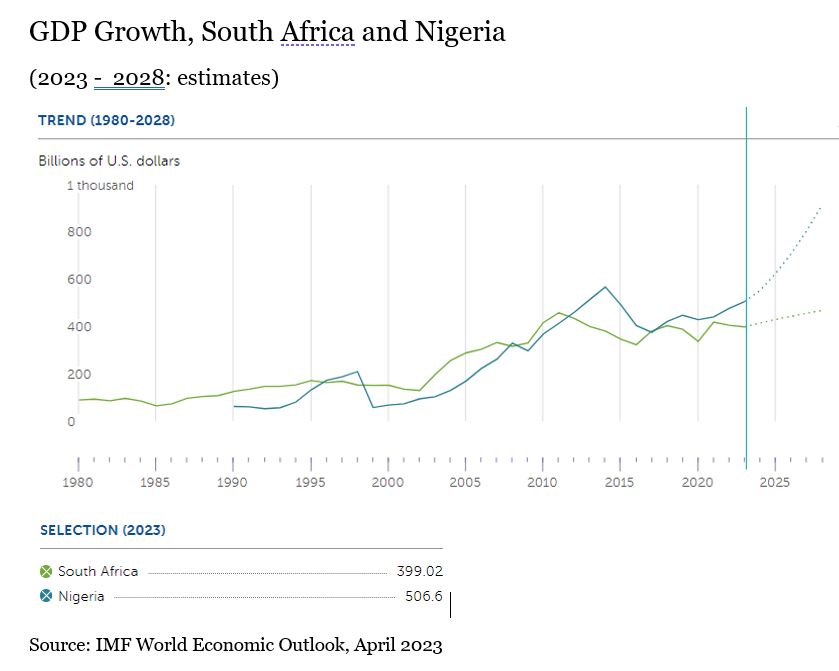

Let’s start with the country that might first come to mind: South Africa. Rich in natural resources (and popular with European tourists), the BRICS member was once considered the key “gateway to Sub-Saharan Africa”. But poor governance, corruption, high inflation, and devastating electricity shortages have crippled the economy. In terms of GDP, the country has fallen behind Nigeria, now the largest economy in the region, according to the International Monetary Fund (IMF).

“South Africa’s economy was already weak (real GDP grew at only 0.3% year-on year in 2019) when the pandemic broke out. Even though inflation increased less in South Africa compared to many peers, its impact on domestic demand has been large,” says Karine Hervé, senior EM macro strategist at the Amundi Institute.

In a country where inequalities are important, household income is low, and unemployment is around 30%, while elevated food and energy prices sharply affect household purchasing power. Similarly, supply chain constraints coupled with elevated production costs have weighed on industrial output, notably as South Africa structurally suffers from deficiencies in energy and transport infrastructures, Hervé adds.

As most of its peers, the South African Reserve Bank (SARB) had no choice than to start raising interest rates to limit inflation, stabilise its currency, and continue to attract foreign investments. This tightening was tangible, with a 475 basis point hike to a rate of 8.25%.

In addition, the negative impact of electricity load-shedding that occurred this year pushed down GDP growth by around 2 percentage points. But recent initiatives to tackle electricity outages should bear fruit, says Reza Karim, portfolio manager of emerging market debt at Jupiter Asset Management. He estimates that the economy will at least not shrink this year (GDP growth is estimated to be around -0.3% in 2023, according to the Bloomberg consensus), and the forecast for 2024 is 1.3% growth.

South African equities, as a result, have strongly underperformed their peers and global markets since the pandemic broke out.

Enter Nigeria

So where have fund managers channelled money? Nigeria’s favourable GDP outlook is mirrored by investment choices made by asset managers, Morningstar Direct data reveals.

“Thanks to the new government's unexpected reform agenda, Nigeria was the biggest positive surprise in recent times,” according to Jupiter AM. “We have recently re-engaged in the country and find more safety in US dollar exposure there,” the asset manager says. “South Africa is less interesting, mainly due to less favourable relative valuations,” it adds.

Jupiter is not the only asset manager that has favoured the emerging West African heavyweight. We have looked at the top 10 holdings of the actively managed funds that performed best over the past year. Here is where the companies are domiciled:

- Coronation UF Africa Frontiers A: Egypt (3 stocks), Kenya (3), Nigeria (2)

- HMG Africa Picking Fund A: Nigeria (4), Kenya (2) Egypt (1)

- Old Mutual African Frontiers B Acc: Nigeria (3), Egypt (2), Kenya (1)

Leading performer Coronation UF Africa Frontiers’ largest position is Eastern Tobacco, an Egypt-based tobacco manufacturer that constitutes 11.68% of Coronation’s portfolio. The stock was up 7.33% in the past year on a USD-basis. The largest Nigerian position is Stanbic IBTC Holding, part of Standard Bank group, whose stock has soared by a stunning 114% in the past twelve months.

Among HMG’s top 10 holdings, Nigerian companies dominate, followed by Kenya. The largest South African position is Clover Industries, a branded foods and beverage group. The group’s shares account for 2.17% of HMG's portfolio, making it the 13th largest position. The managers selected Mansard Insurance Plc from Nigeria as the top holding, which is part of the AXA Group. The stock was up 107% over the past 12 months.

Old Mutual African Frontiers channelled 6.84% of the fund into Commercial International Bank (Egypt), whose stock price was nearly flat over a year. But the Nigerian picks meanwhile outperformed, among them United Bank for Africa (+111% year-on-year), Guaranty Trust Holdings (+96%) and Zenith Bank (+83%).

Actively Managed Funds Dominate

Of the 23 strategies that are available for the European investor, just two are index funds: Lyxor Pan Africa ETF Acc and Xtrackers MSCI Africa Top 50 Swap ETF. Returns last year range anywhere between 3.11% and -12.32%, though on a three-year annualised basis, returns were between 10.17 to -1.32%. This was accompanied by high volatility.

Volatility and inconsistent performance are the main drawbacks for the African equity investor. Here is another: an investor mindful of ESG may find it hard to find vehicles that meet their own criteria – Coronation’s massive exposure to a tobacco manufacturer being just one case in point.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/K37XP2B425AIRFXOASS7WIGPLM.jpg)