Sometimes what we see in equity markets bears no relation to what is happening in the real economy. This is one of those times.

In both the US and the Eurozone GDP growth is still relatively anaemic, rising by 1.6% and 1% respectively year-on-year in the first quarter of 2023. Despite this, earnings season so far in both regions has been pretty decent.

I’m going to avoid talking about "beats" versus "misses", because as we all know this is just a reflection on how well firms did at under promising and overdelivering. Rather, I’m going to walk you through some of the global trends we’ve been seeing this earnings season, and where the differences lie between US and European earnings.

What's Happening to Banks?

Banks are on the mend. That’s the short story from what we have seen so far from the banking world. Capital ratios, particularly in Europe, are solid, while interest rate rises are allowing banks to improve their profitability once again, after so many years of operating with tight spreads on their loan books. While some concerns remain in the US around banks geared toward specific sectors, such as commercial real estate, most the large banks we cover in both regions have proven themselves resilient over the last quarter.

What's Happening to Consumer Stocks?

The ability to raise prices has never been so important in the consumer sector, with inflation finally falling, but from elevated levels. Luxury goods firms, many of which are domiciled in Europe, have been particularly proficient at this, with their customers generally less price-sensitive. Further down the food chain however it has been more of a bun-fight, with consumer goods firms like Colgate pushing through price increases, but barely offsetting rising costs.

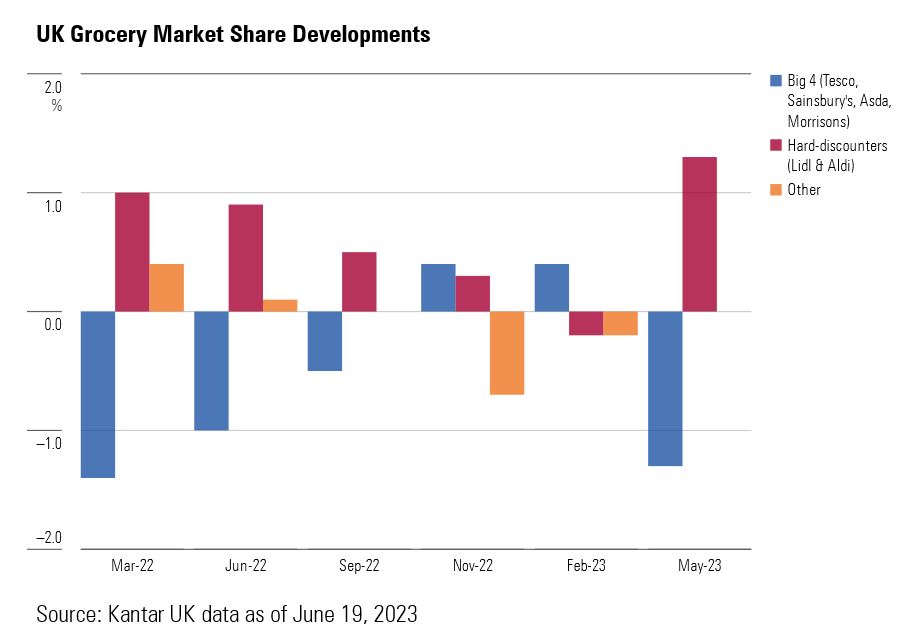

Similarly, US-based Kraft has managed to push through price increases, but at the expense of market share, with private label firms and smaller competitors pushing hard on promotional activity to gain market share. In Europe this problem is even worse, with private label penetration even higher than north America. In the UK most recently, market share data showed the hard discounters have been continually taking market share from the large traditional supermarkets.

And Travel and Transport?

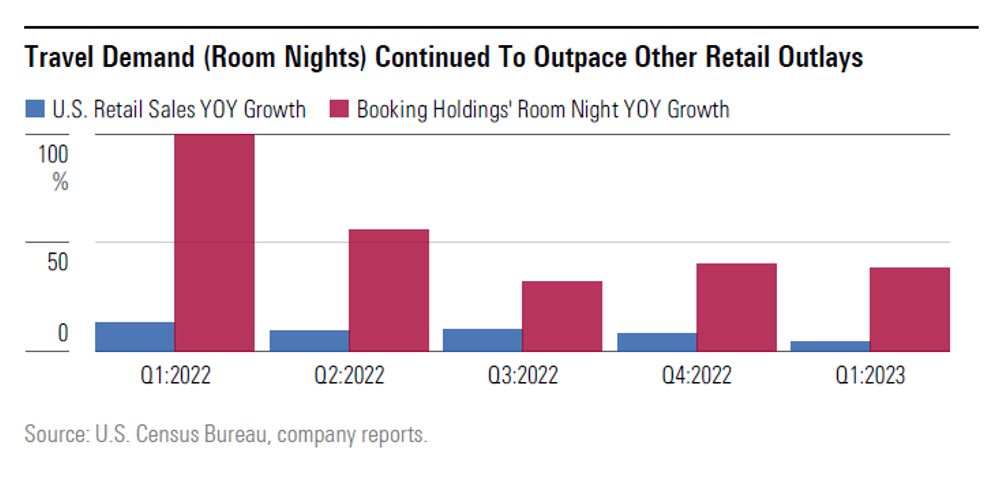

Travel has been a strong theme on both sides of the Atlantic, with Accor hotels in the US, and counterparts like Whitbread in the UK, reporting strong levels of bookings, and room revenues. This is despite many consumers feeling the pinch from higher mortgage rates and elevated food bills. But after an extended period of lockdown, consumers are placing a high value on being able to travel once again. Vinci, the European listed concessions firm, also affirmed this trend, with rising passenger numbers through European airports.

Another knock-on effect from the pandemic was the resulting bottlenecks in the shipping industry. This led to a scramble by industrial and consumer firms to get their hands on as much stock as possible. This quarter’s earnings have confirmed that many firms are finally destocking, with chemicals firm BASF reporting this negative effect on sales, and the global third-party logistics firms Kuehne + Nagel and DSV reporting falling volumes as a result. Materials, which have been harder and more expensive to come by, are finally becoming available again, according to European elevator manufacturer Kone.

Oil and Housing

The oil majors in the US and Europe sang from the same hymn sheet this quarter, with the effects of depressed oil and gas prices earlier this year coming through in the form of lower revenues. The silver lining however was falling costs, which rose in tandem with energy prices last year. Despite similar levels of performance, we see a big opportunity with the European oil majors, namely Shell and BP over their US counterparts Exxon and Chevron. The valuation gap between the two is partly driven by ESG concerns by European investors, a situation we believe will rectify itself over time as the European majors ramp up their investment in green energy.

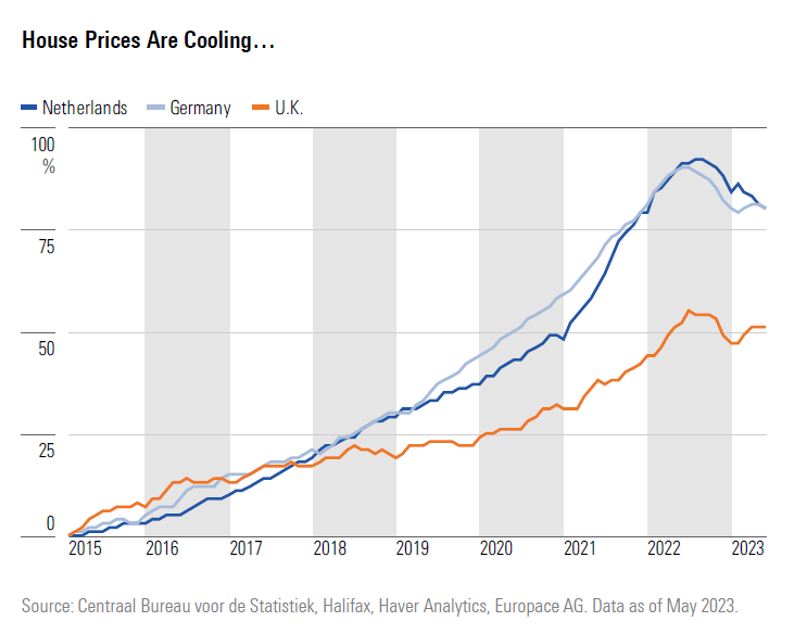

One major discrepancy between the US and Europe is around housing markets. House prices in the US have largely held up over the last year, despite rising interest rates. In Europe the price declines have been felt more sharply, heaping pressure on homebuilding stocks, some of which have more than halved in the last year. The good news however, is that interest rate rises should soon be coming to an end, while input costs, namely housebuilding materials, are coming down from their recent highs. This should alleviate the pressure on the European homebuilders and allow their share prices to correct.