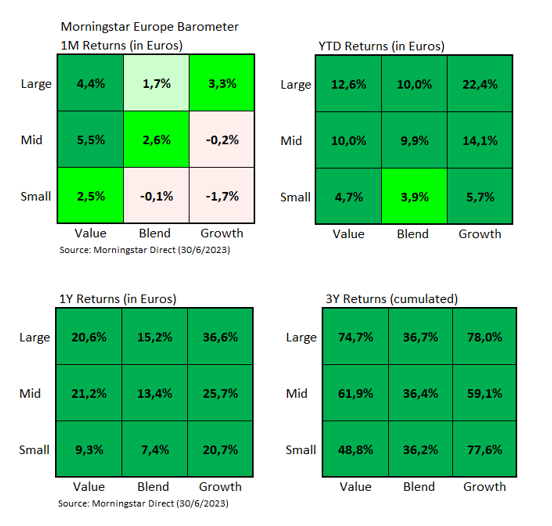

The first half of 2023 has favoured growth companies. If we focus on large-cap stocks in Europe, the Large Growth style gained 22.4% (in Euros) versus 12.6% for the Large Value style.

In this last month of June, however, value companies have done better than growth companies, both in large, mid and small caps.

The Large Value segment gained, for example, 4.4% in June versus 3.3% for Large Growth. The difference in mid-caps was much greater: 5.5% versus -0.2%.

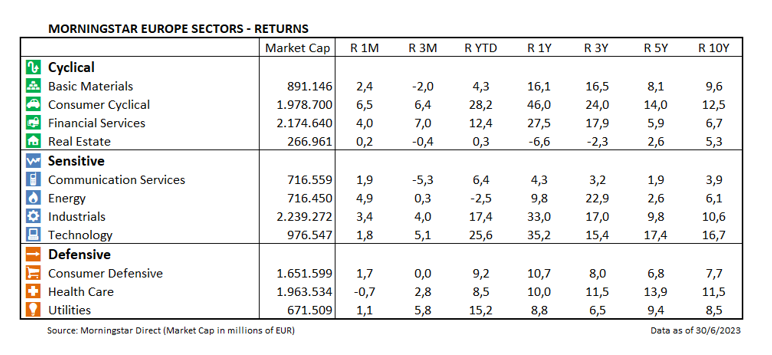

The good performance of the two key sectors for value, financials and energy, is clearly the explanation for these differences in performance. The energy sector advanced by 4.9% in June and financials by 4.0%, compared with 2.3% for the Morningstar Europe NR index.

The largest contributor to the Large Value performance in terms of capitalisation last month was the oil company Shell, which gained 5.7% in euros (it is the largest capitalization company in the Large Value segment).

In banking, Italian and Spanish banks stood out in June: UniCredit SpA rose by 18.7%, Banco Bilbao Vizcaya Argentaria by 14.9%, and Banco Santander by 11.1%.

Another sector also helped the value style to perform well: automotives. Large German companies like BMW and Volkswagen, advanced by 10.4% and 5.5% in June, respectively.

In the Large Growth segment, two companies achieved good rallies last month. French fashion and drinks giant LVMH Moet Hennessy and L'Oreal SA, which gained 6.0% and 7.0% respectively.

But the poor performance of large pharmaceuticals (AstraZeneca PLC and Novo Nordisk lost 3.1% and 1.5%) meant the Large Growth segment did not advance as much as the Large Value segment.

In fact, at sector level, it is worth noting the only sector to post a negative return in June was health, which was down 0.7% in euros.

The best performer was consumer cyclicals, up 6.5%. Within this sector, Carnival PLC, the world's largest cruise company, made significant progress, gaining 66% in Euros.

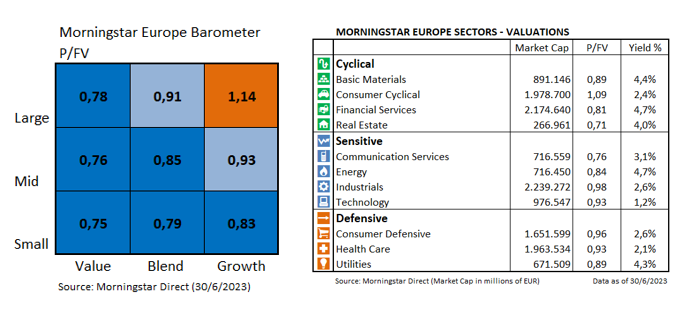

As far as valuations are concerned, it is interesting to see how all sectors (except Consumer Cyclicals) are trading at a discount (Price/Fair Value below), but the Large Growth segment is significantly overvalued (P/FV of 1.14). This means that within each sector there are value companies and growth companies with significant valuation differences.