.jpg)

"It was the best of times, it was the worst of times" is a quote that crops up in every other earnings note. This earnings season, the cliché fits.

With inflation still high across the Eurozone, much of the success or failure of consumer and industrial stocks came down to their ability to effectively pass through cost increases.

Likewise, falling energy prices meant bad news generally for energy companies. Although given the 2022 they had, can anyone have too much sympathy? Lastly, the banking sector generally outperformed (low) expectations, with rising interest rates a boon in many instances for banks.

After the crisis in March, the banking sector was undoubtedly the most heavily scrutinised going into earnings season, and it didn’t disappoint. Ignoring the ongoing debacle in Switzerland, with UBS (UBSG) now tasked with the herculean effort of integrating Credit Suisse, and deposit flows volatile as investors rebalance their cash portfolios, updates from the sector were reassuringly dull.

Large banks including Barclays (BARC) and Deutsche (DBK) reported solid updates. Rising interest rates have allowed banks to generate stronger profits, as the gap between borrowing and lending rates rises.

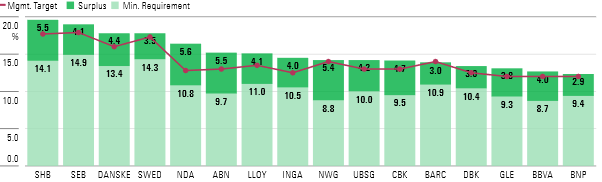

Although rising rates can prove a double-edged sword, as bad debts can also rise, mortgage market products, which have been a tough place to operate for the last few years, should recover strongly over the rest of the year. Importantly, banks remain well capitalised, with our chart below showing that every large bank under our coverage has surplus capital, above and beyond central bank requirements.

Once the top-performing sector in Europe in 2022, the energy sector finally saw a slump in the first quarter of the year as falling energy prices dragged down revenues and profits. This shouldn't come as a surprise to anyone – the energy price spike that began with the Ukraine war was never going to last forever, and energy prices have been waning since late 2022.

Shell (SHEL), Eni (ENI) and big oil peers' revenues fell as a result. However, there were some bright spots. First, operating costs are falling in tandem with revenues. Second, the cost of replacing the oil and gas taken out of the ground is also falling. Both of these elements improve the chances oil majors will retain profitability even at lower price levels.

Inflation across the Eurozone has been running at elevated levels for more than a year now. Although the headline rate has fallen from its peak late last year, core inflation (what we’re left with when we strip out food and energy) is still stubbornly high.

Make no mistake, this is having an effect on businesses. For firms that sell basic, commoditised products, the first quarter of the year has been tough. Phone and internet providers like KPN (KPN) have seen operating margins fall as high competition holds them back from price increases that cover higher costs. Associated British Foods (ABF), owner of retailer Primark, saw margins fall even harder as management made the decision to absorb price increases rather than risk losing customers.

Many of the Moaty names we cover – those with pricing power – have been able to pass these price increases on to the end customer, allowing them to keep profitability steady.

Luxury goods retailers like LVMH (MC) and Hermes (RMS) are fine examples of this; both saw revenues rise by double digits as wealthy individuals, unencumbered by rising prices, splashed out. Likewise, specialised industrial firms like Alfa Laval (ALFA), ABB (ABBN) and CRH (CRH) have managed to push price increases through in a timely fashion. Trees can’t grow to the sky though, and if inflation remains sticky for the remainder of 2023, these firms will find their ability to pass through price increases tested.