What are the consequences of the Credit Suisse collapse? The market volatility in mid-March made European banks even cheaper, but the Swiss bank’s rescue by UBS has not (so far) opened a new Pandora's box. That’s the conclusion of Morningstar banking analysts Niklas Kammer and Johann Scholtz, who argue that fear of contagion in the European banking sector is overdone.

“European banks’ balance sheets are sound and have ample liquidity and robust capital buffers,” they conclude in their Q1 review of the sector. Banks look cheap again, recent volatility should boost investment banking and trading, and credit risks remain under control despite recent strain. However, there are signs of stress in the real estate sector. Inflation is starting to fall but is proving more persistent than expected. “Inflation appears to have peaked across Europe, although a structural decline has yet to materialise,” Kammer and Scholtz say, meaning that central banks will be cautious before easing up on inflation too early.

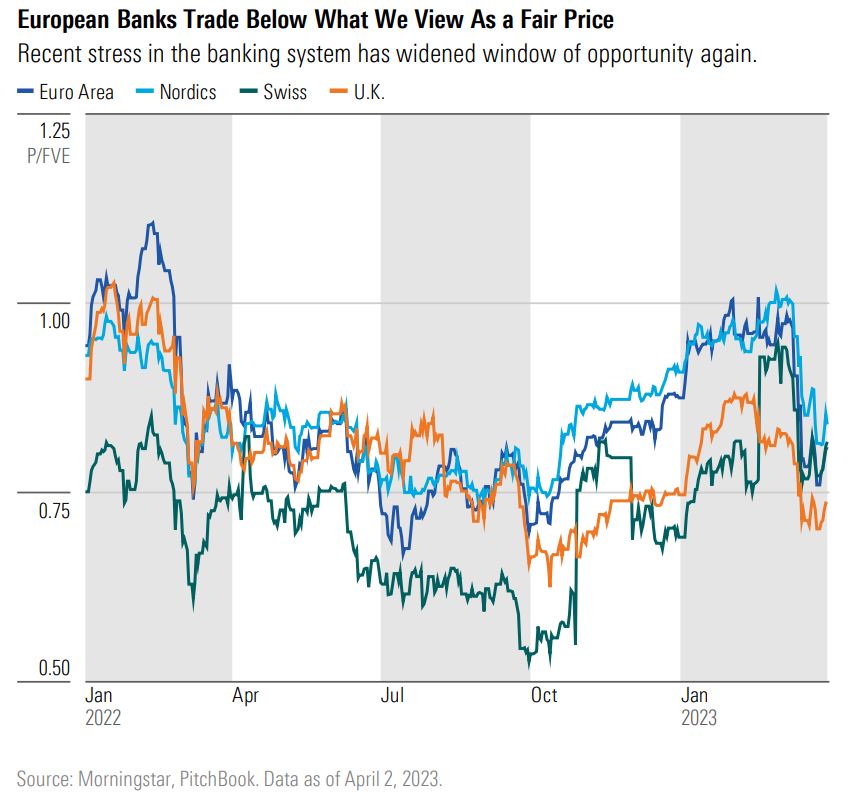

During the two weeks that made investors worry about wider contagion from some US regional banks and Credit Suisse, the Morningstar DM Europe Financial Services index lost 12% (in euros, from 03/10/2023 to 03/25/2023) underperforming the region by approximately 800 basis points. This made the market valuations of European bank stocks, which at the end of February were already discounted by 13% on average compared to their fair value, even more appealing.

“Although short-term volatility may persist, we believe banking stocks in Europe can still create value for a long-term-focused investor. Also due to the strength shown by the sector. Interbank markets have remained calm, supporting our view that issues at Credit Suisse were idiosyncratic,” Kammer says.

“Furthermore, even if we anticipate that funding costs for European banks will increase due to the banking sector turmoil, we expect net interest margins to remain structurally above levels experienced over the last decade.”

What worries the European banks is the worsening economic situation. While inflation is proving more resilient or “sticky” than expected, bond yield curves have started to slope downwards, reflecting expectations of a recession across Europe. A recession would mean banks will have to deal with an increase in credit risk as consumers default on loans and companies get into financial trouble.

“In the last 10 years, European companies have taken advantage of extremely low interest rates to increase their gearing materially, but the higher interest rates, together with the increase of inflation, could make it harder for firms to service and roll their debt and could result in loan losses for banks,” the analysts say.

Real Estate Sector Exposed

State intervention has help cushion the blow for consumers, but the corporate sector is more exposed.

“Governments across the continent implemented an extraordinary range of support measures to prevent job losses and to prevent that higher living costs brought about by high energy costs and inflation could have translated in a worsening of the economic situation. For these reasons we continue to view European banks' corporate loan books as more vulnerable than household loans,” they say.

The biggest threat for the banking sector could be the real estate market. Over the past decade, ultra low interest rates have inflated property valuations, but the rapid rise in mortgage rates and tightening of lending standards have been a shock to borrowers. Inflation hitting real wages has lowered housing affordability as well.

There are already signs of strain across Europe’s housing markets, as Morningstar’s Lukas Strobl shows in his analysis. What would a housing slump mean for banks? “Low loan/value ratios across the banks we cover, not least owed to the high price appreciation of real estate assets over the past decade, suggest overall good resiliency to price corrections in the future”, says analyst Johann Scholtz.

.jpg)