Morningstar European analysts have just put out their equity and inflation outlook for Q1 2023. While 2022 was a tough one to navigate, this year could offer opportunities for investors who position themselves for persistent inflation.

We believe the transitory elements of inflation, namely food and energy, are weakening, but an elevated level of core inflation may remain for some time. Investors should look to companies that can effectively deal with this; we categorise them thus:

• Companies that operate with inflation-protected contracts – examples include telecom tower operators, catering firms, and toll road operators;

• Firms that command pricing power, through strong brands or other intangible assets;

• Last, we have companies that are actually benefiting from inflation, and often elevated power prices – many of these firms are in the energy or utilities sectors.

Let’s pick out some key charts from the outlook.

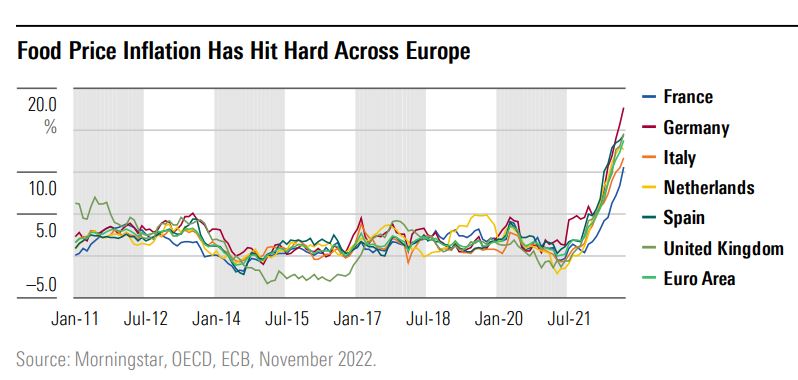

Food and Energy Prices Are Falling

Our first chart shows how quickly and aggressively food prices have risen.

Historically, food and energy cost spikes have generally tended to be transitory. This is again proving to be the case, with power prices already decreasing in parts of Europe, and our forecasts pointing to further falls.

As bottlenecks in the shipping networks ease, we would expect to see the costs of consumables, including food, falling too.

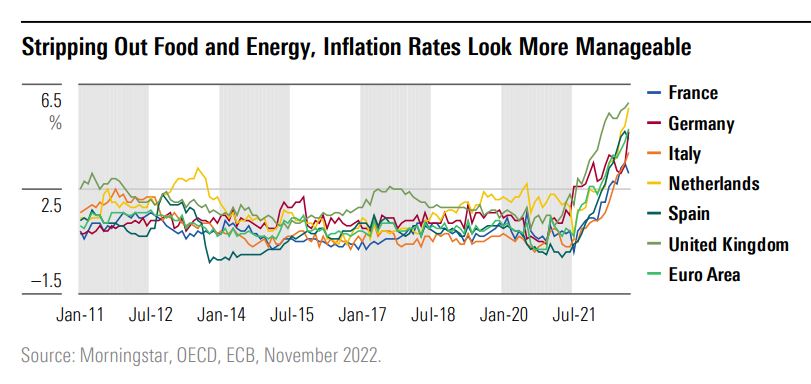

Should this occur, central banks in Europe would be required to deal with core inflation of around 5%, a far more manageable task than headline inflation of closer to 10%. Let’s now look at "core" inflation, which is a measure of price rises without food and energy included. The UK and the Netherlands still have the highest inflation in the region on this measure.

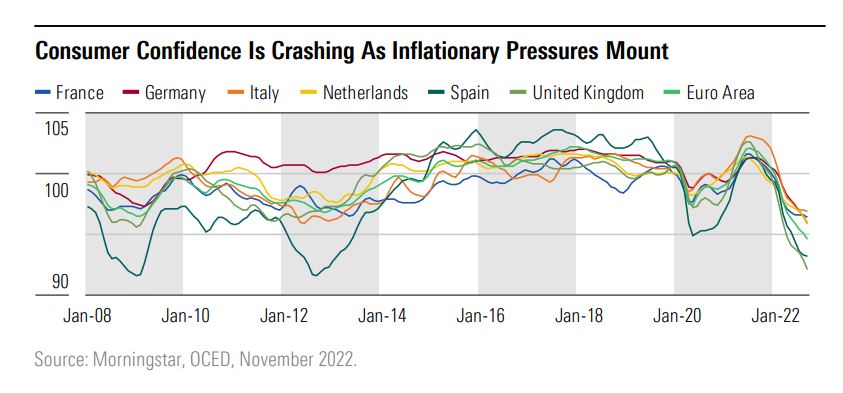

Let’s now look at consumer confidence. What’s interesting here is how the post-pandemic "bounce" has gone into reverse.

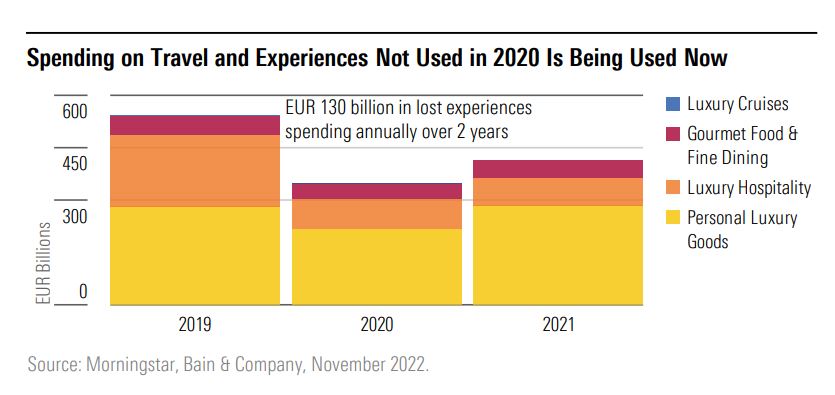

But consumers are still spending some of their lockdown savings. Pent-up demand for travel is still working its way through the system, evidenced by US and Europe industry hotel revenue per available room surpassing 2019 levels.

In a relatively commoditised industry this ability to pass through price increases so easily is unlikely to persist beyond the near term, but hotel and travel firms are certainly making the most of lucrative opportunities. Here’s where the money has gone in the last three years:

Luxury is a recurring theme here. High-end brands have historically been successful in raising prices above inflation, as many have less price-sensitive customer bases.

Examples of successful firms here include wide-moat Swiss premium chocolate manufacturer Lindt & Spruengli. One of the key drivers of our wide moat rating for the company is its brand strength, which enables it to command a significant price premium over mainstream chocolate brands.

Pernod Ricard is a similar story: with high-end spirit brands such as Havana Club and Martell cognac, the firm has carved out a strong brand, underpinning our wide moat rating for the stock. It showed its pricing power in 2022 by raising prices, while also driving sales growth, which is no easy feat.

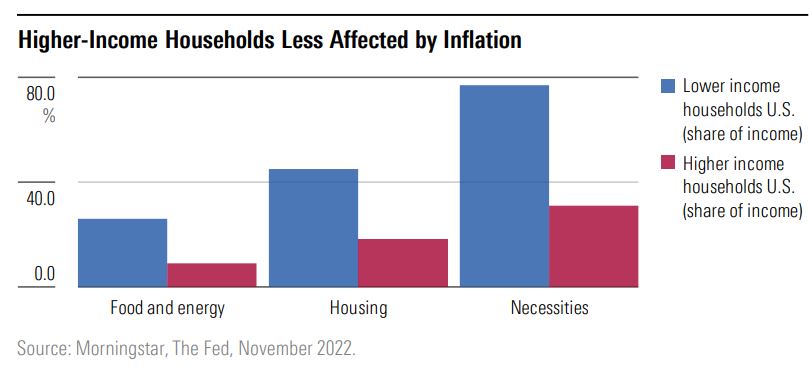

As during the pandemic, the economic pain in the high inflation era is not being evenly distributed. Data from the US bears this out: