Talk about deglobalisation is everywhere – except the data.

It's well known that companies in the UK FTSE 100 source around 75% of their revenue from overseas, meaning that, when you invest in a UK large-cap, you're exposed to economic factors beyond our borders.

Deepening globalisation runs contrary to the dominant current narrative. We live in a "postglobal world," according to the title of a new book describing a trend toward "localization." A recent issue of The Economist focuses on "reinventing globalisation."

"Offshoring," popular in the 1990s and 2000s, has become a dirty word, while "onshoring," "reshoring," and "slowablisation" are trending. Even before the pandemic, inflation, and war in Europe exposed the weaknesses in global supply chains, political currents had turned against globalization. Independence and self-sufficiency are ascendant.

Streams Across Borders

To understand what’s going on, remember the truism that stock markets are markets of stocks. Market-level trends are driven by the behaviour of their underlying businesses.

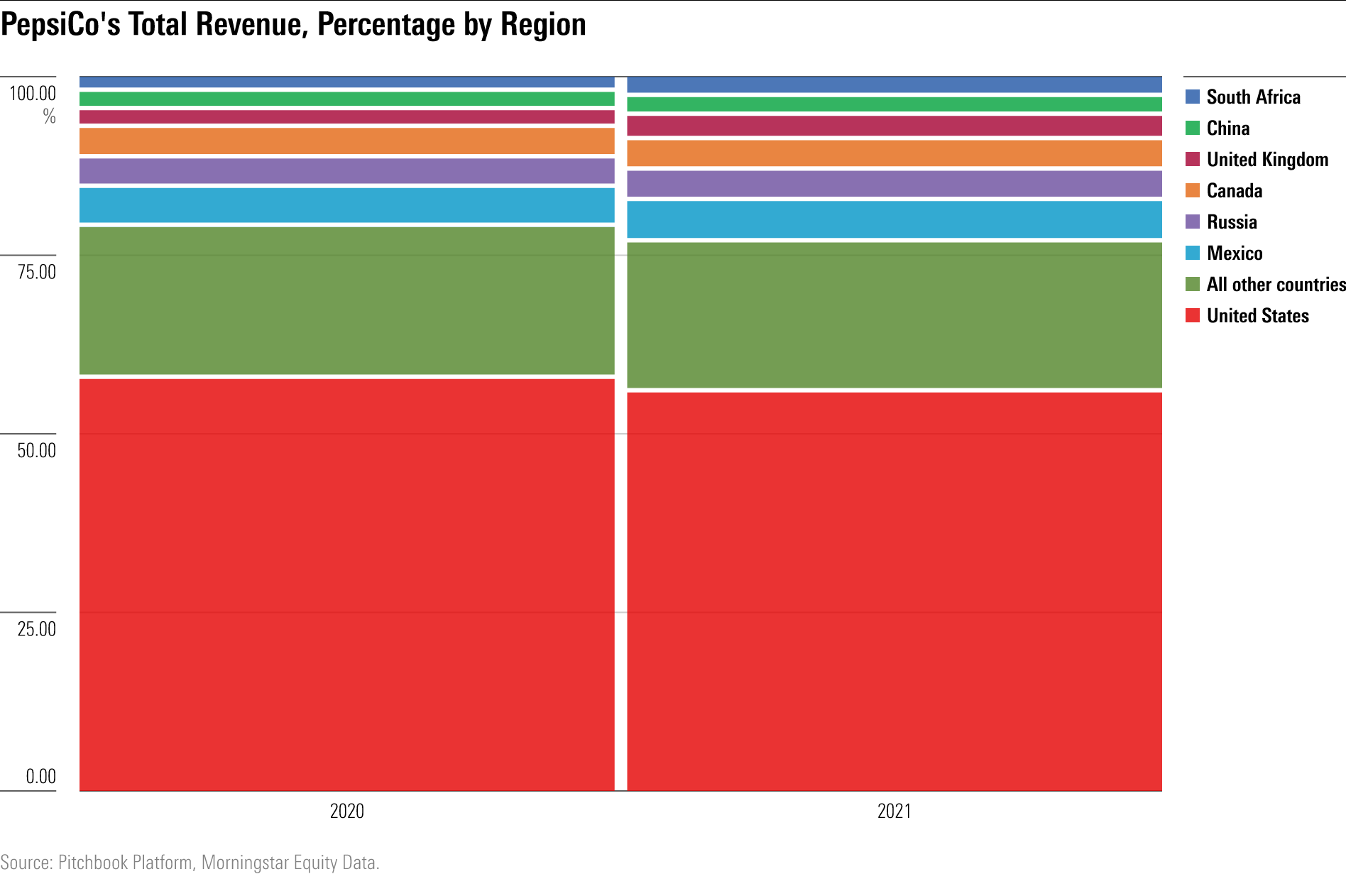

Consider PepsiCo, the US-based food and beverage giant classified in the consumer defensive sector. In 2021, Pepsi’s revenue from carbonated drinks and salty snack sales outside the US grew by a faster rate than its domestic business.

Like many companies, Pepsi doesn’t specify all sources of global revenue. What’s sure is that Russia won’t be one of Pepsi’s top markets when it reports for 2022. The company exited the country after the Ukraine invasion.

Pepsi is among many global giants operating from the US, the world’s largest equity market. Many of the largest public companies, including Microsoft, Alphabet, Meta Platforms, and Nvidia earn the majority of revenues from outside the US.

In aggregate, the US equity market sourced 62% of its revenue domestically as of June, down from 63% a year ago.

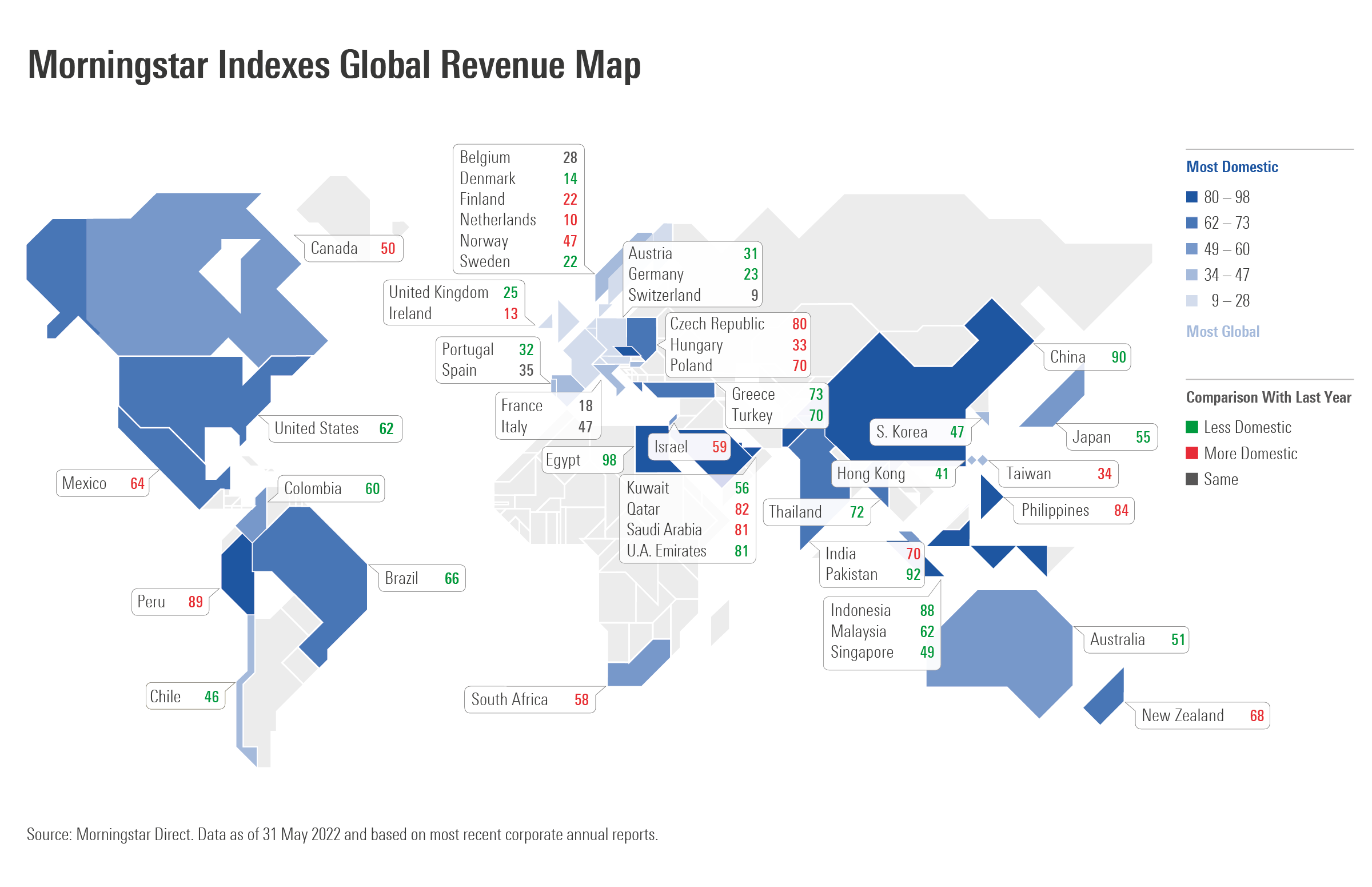

Emerging Markets Remain the Most Domestic

The world’s four largest equity markets (the US, Japan, the United Kingdom, and China) all source a larger share of revenue internationally than they did last year. None of the moves were dramatic. Japan went from 57% domestic a year ago to 55% this year. The UK went from 27% to 25%, and China from 91% to 90%.

Emerging markets, such as Egypt, Pakistan, China, Peru, Indonesia, the Philippines, and Persian Gulf states, remain the most domestically oriented. The fact that the Morningstar China Index sources an estimated 90% of revenue from China, despite the Chinese economy’s export orientation, can be explained by the domestic focus of its top constituents Tencent, Alibaba, Meituan, China Construction Bank, and JD.com.

European markets remain the world’s most outward-looking. With the exception of Greece, which is largely domestic, European markets are dominated by global companies. The Morningstar Switzerland Index, which includes Nestle, Roche, and Novartis, is the most global, with the US representing an estimated 30% of its revenues. Amazingly, the Morningstar Netherlands Index sources more revenue from Taiwan (an estimated 13%) than from the Netherlands (10%).

It's Not Just A Commodity Boom

Economic sectors do not seem to be strong drivers of change from last year. For example, some resources-heavy markets became more global, including Australia, Brazil, Chile, and the United Arab Emirates; but others, like Canada, Peru, Saudi Arabia, Norway, South Africa, and Qatar did not. The market for resources is obviously global, so producers might be expected to increase international revenues in an era of high prices and soaring demand.

Similarly, no clear trend was discernible within technology-heavy markets. The US, Korea, and Germany (all of which have significant tech representation) globalised. Taiwan, the Netherlands, Israel, and India, did not.

Canada sources roughly half of revenues from outside its markets. It is a resources-heavy market dominated by a few large banks, and its economy and population are similar to Australia. But whereas Canada sources an estimated 30% of revenue from the US, China is the biggest external market for Australia at 13%. Only Taiwan (18%) and Hong Kong (17%) depend more on Chinese revenues.

Revenue Sources Blur The Lines

The fact that equity markets are globalising certainly runs counter to the narrative that supply chains are onshoring and countries are pursuing self-sufficiency. But the stock market is not the economy. Revenue sources for public companies represent just a piece of the mosaic. There are many other ways to measure economic globalisation, the most common being trade as a percentage of gross domestic product.

For investors, globalised revenue sources blur the lines between the domestic and international portions of a portfolio. While it’s true that global exposure can often come through domestic companies, it’s also true that leading players in an investor’s home market may be based offshore. As ever, a global portfolio offers the broadest opportunity set.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/347BSP2KJNBCLKVD7DGXSFLDLU.jpg)