"My Government’s priority is to grow and strengthen the economy," Prince Charles intoned on May 10, deputising for his mother during the Queen’s speech.

Stripped away from the occasion's pageantry, those words seem rather obvious. As voters tend to blame politicians when things go wrong, governments need the UK economy to grow because it keeps them in power.

Growth and recession matter to investors too, not least because, without a regular job or income, the task of saving for the future is considerably harder. But the link between economic output and stock market performance is not as clearcut as you might think.

Recessions are rightly feared because they bring job losses, house repossessions and bankruptcies, all of which bring misery to individuals, and deter companies from investing and hiring. While high inflation grabbed attention, the Bank of England’s recession warning at the start of the month became the real story, and the pound sold off immediately.

The Bank now forecasts a contraction of 0.25% in 2023 rather than the 1.25% growth it predicted just three months ago. This warning tops a large list of anxieties facing the world, including war in Ukraine, soaring prices, rising interest rates, commodity shortages.

But what is an investor to make of these forecasts? Does it mean you invest less in the UK, shift your allocation to better growing countries? Or just drown out the noise and focus on your own portfolio and a longer-term timeframe?

Two Quarters, Big Problems

Let’s start with the basics: recessions are usually defined as two quarters of negative economic growth. We last had one in 2020 during the pandemic, and our charts in this story show what an outlier this was in our history. Before that we had one that lasted just over a year, between 2008-2009 during the financial crisis. Isolated pockets of contraction occurred between 2010 and 2012 (when George Osborne was notably booed at the Paralympic games), but the pain was not sustained enough to constitute the "double dip" many feared.

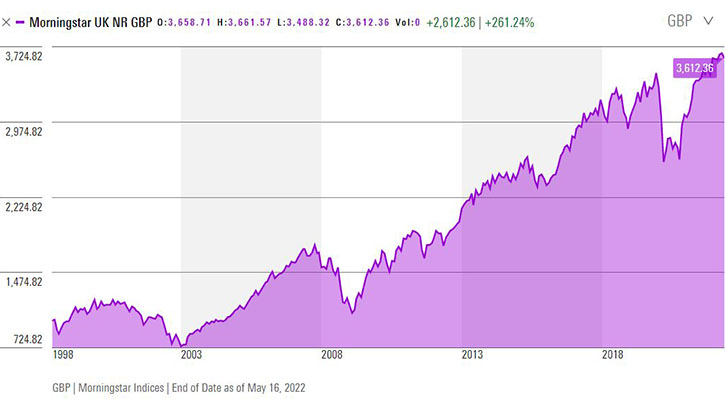

Readers with longer memories will recall the one before that, in 1990-1991, which lasted for a similar duration. Looking at the Morningstar UK index from 1994 to 2022 it’s clear where the major economic crises occurred, and even the minor ones like the end of dotcom boom in the early part of the century. But the upwards shape of the chart is hard to ignore and in hindsight there were plenty of buying opportunities.

Markets Move On

Before you cancel your investments into your UK funds, then, let’s look at some contrarian arguments amid the deluge of awful headlines:

1) "The stock market is not the economy and vice versa" is a common phrase seen on social media, usually when some unfavourable data is published: equity markets are forward looking and factor in any variables, including interest rates, currencies, economic data, dividends.

"By the time government number crunchers have declared a recession, the markets will be pricing in the upturn," says AJ Bell director Russ Mould. "It may be right to say stocks don’t get crushed in recessions. But only because they have been crushed already on the way in. Stocks will then move higher before the economic data improved and shows we are out of a recession."

2) Emerging market zealots have learned that hard way that high growth rates don't translate into strong investment returns. The UK economy is unlikely to grow at 5% a year but has other attributes that are prized by investors.

3) Many consumers are heading into this recession within a bigger than usual savings buffer because of numerous lockdowns and government support schemes. Steven Bell, chief economist at BMO GAM, puts the figure at 12% of disposable income, though he does acknowledge the “huge financial cushion” is very unevenly distributed.

4) Modern markets and large companies are very internationally focused too, so are less sensitive to movements in the UK domestic economy. Larger firms tend to be able to diversify across different territories and shift capital accordingly. A lot of the UK's problems are global in nature (war, pandemic, inflation), so all countries are facing the same issues.

5) UK stocks have been unloved since the financial crisis and eclipsed by the glamour of the US tech boom. While there are signs that the tables are turning, UK stocks can hardly be described as being in bubble territory – so may have less far to fall when times get tough.

"The UK market remains a reliable alternative to highly-valued, crowded trades," says Richard Colwell, head of UK equities at Columbia Threadneedle. He adds that this valuation disconnect makes the UK an attractive place for private equity and foreign investors. "The opportunities for UK M&A persist, and inbound activity remains at record highs."

6) The thing driving the strong gains in global stocks in the last decade has been low interest rates, and that has supported other asset classes like housing and crypto. Both the Federal Reserve and Bank of England seemed committed to the interest rate hiking process in their early May meetings. Could they ease off if economic conditions worsen? Bond markets are suggesting this may be the case – the UK 10-year gilt is currently 1.8%. A lot depends on whether inflation starts to fall this year.

But if UK interest rates peak at 2%, would that be a complete disaster? That rate would be historically very low, allowing homeowners and businesses to continue to borrow at reasonable levels. Financial markets, anxious that the punch bowl was taken away too soon, may see this as a sign of "business as usual" and find another reason to rise. A mild – and short – recession, could help support that theory.

Too NICE for Innovation?

The final argument brings us back home to the UK, which was our editorial focus last week. The 1997-2007 era was described as the “NICE” decade because it featured "non inflationary constant expansion". In retrospect, it may be hard to imagine a 10-year period like that again, and especially given the impact of Brexit, Covid-19 and war in Europe.

That said, there’s an argument that calm conditions are not conducive to innovation, and that the greatest breakthroughs come when entrepreneurs are up against it. Economist Joseph Schumpeter described this as the "recuperative power of capitalism". If that seems wishful thinking to you, Morningstar Investment Management’s Dan Kemp may have some more pragmatic advice: try to build a portfolio that can weather all economic climates.